Click Here to Read the Full Version

While US headline inflation came in below expectations, helping soothe sentiments, President Trump’s tariff interventions continue to carry an inflationary bias.

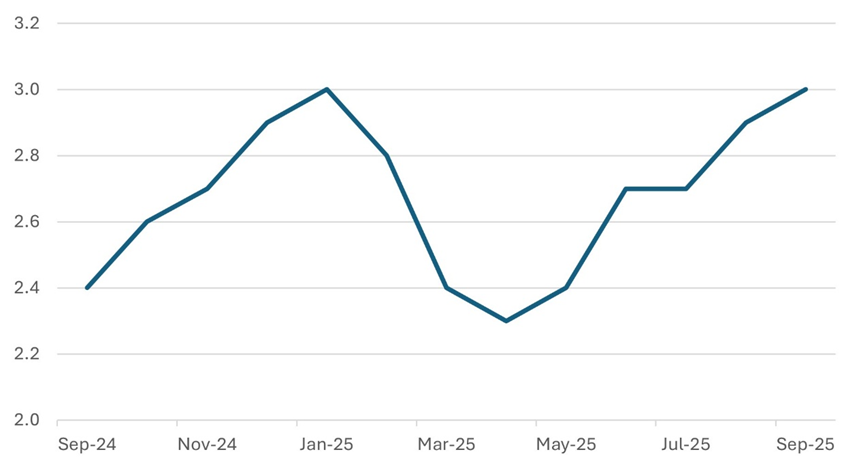

US inflation data for September was marginally softer than expected, with headline CPI rising 3.0% year-on-year and core inflation holding at 3.8%. Markets took comfort in this, viewing it as a sign that disinflation remains on track. However, any conclusion at this stage will be premature, as we’re still in the early phases of a structural adjustment to tariffs. For instance, the latest 10-percentage-point hike in US tariffs on Canadian imports announced without warning, inflates the cost base for US producers and consumers. These levies hit a range of goods, from industrial inputs to food, and are likely to leak into core CPI in the months ahead. The broader geopolitical backdrop hasn’t helped either and is contributing to inflationary pressures. In the past week alone, Washington has imposed new sanctions on Russia, targeting its energy exports. While the market impact of those sanctions has been muted so far, the ongoing trend of using trade and sanctions as geopolitical tools risks embedding higher input costs into global supply chains. The recent cooling in inflation could prove temporary if these pressures persist.

Chart 1: In Case You Missed It, US Inflation Went Up in September!

% change year-on-year

Source: Bloomberg

The Fed is almost certain to cut rates by 25 basis points this week. Markets have priced it in, and the softer CPI gives the Fed cover to move. Chairman Jerome Powell is likely to acknowledge the progress on inflation but keep a close eye on tariff risk and geopolitical instability. Forward indicators, slower credit growth, weaker consumption suggest the economy is cooling. The tone the Fed adopts at the press conference will matter more than the cut itself. The cut is coming, but the message will shape expectations from here.

The dollar weakened modestly last week, giving back some recent gains as markets leaned further into the Fed pivot narrative. The softer-than-expected inflation data reinforced expectations of a near-term cut, narrowing rate differentials and weighing on the greenback. The dollar’s move lower – orderly nonetheless – was most visible against the euro and the yen. While policy divergence in Japan and Europe had earlier supported the dollar, a firmer political backdrop in the former and signs of fiscal action in the latter also contributed to the greenback’s weakness. Safe-haven flows remain intact, and for now, the broader dollar trend remains range-bound.

Chart 2: US Dollar Spot Index Consolidates

Index

Source: Bloomberg

Beyond the near term, stagflation risks in the US are increasing. We think core PCE inflation to stay elevated at 3% into year-end, only easing to 2.5% by end-2026, still above the Fed’s long-term 2% target. At the same time, the consensus believes that GDP growth should slow to just 1.8% this year. The labour market, once a key source of strength of the economy, is now showing signs of stress. The Chicago Fed’s Labor Market Dashboard puts the hiring rate for unemployed workers at just 45.2%, the lowest since 2009. Nearly 950,000 layoffs have been announced so far this year, while new hiring announcements are down 58% year-on-year. Meanwhile, the federal government shed 100,000 jobs in early October due to a backlog of retirements and buyouts. With a weakening labour market and persistent inflation, rate cuts and balance sheet adjustments could risk reigniting price pressures without addressing the slowdown. For markets, that sets up a tug-of-war: front-end yields falling with the Fed, while the long end remains under pressure from Treasury supply and de-dollarisation.

Against this backdrop, Asia stands out.

Japan’s New Phase of Positive Consensus

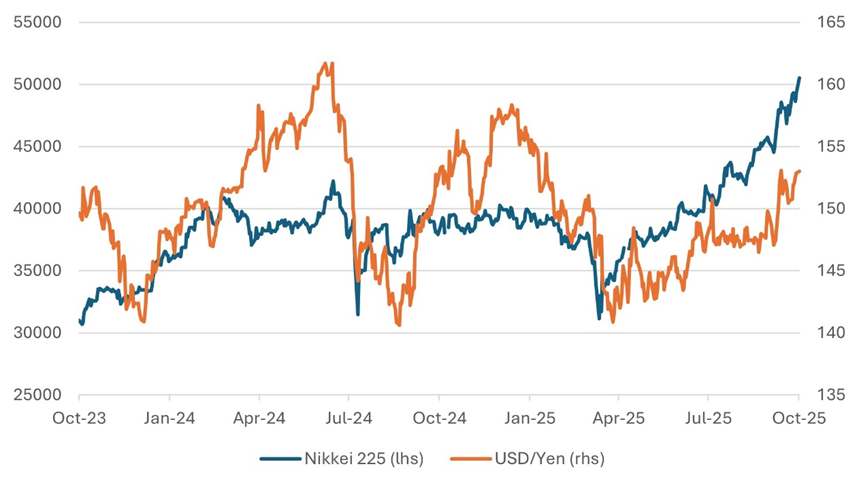

Further upside in Japanese equities and potentially the yen? The appointment of Sanae Takaichi as Japan’s first female prime minister marks a decisive shift in the country’s political fortunes. A known conservative and close ally of former prime minister Shinzo Abe, she has defied expectations by assembling a cross-faction cabinet that includes former rivals and members of the Japan Innovation Party. Many see that as a pragmatic and stabilising move. In fact, Takaichi’s leadership style is drawing comparisons to Margaret Thatcher, tough, ideological, but tactically inclusive. Her economic agenda focuses on “crisis-management investment” across semiconductors, AI, and defence, aimed at rebooting productivity and hardening Japan’s strategic position. The policy direction is clearer, the intent stronger. Japanese equities continue to benefit from this momentum. The yen, still soft on current fiscal and monetary settings, could strengthen if the policy mix delivers a sustainable productivity boost.

Chart 3: Japanese Equity Index and Yen – Room for Both to Perform Further

Source: Bloomberg

China’s Inner Strength

China’s recent plenum didn’t deliver anything outstanding, but it did send a more coherent and confident message: Beijing is placing fresh emphasis on strategic sectors such as AI, semis, and advanced manufacturing, while also signalling greater intent to support domestic demand and tackle local government debt. The real shift, though, is external. Senior US and Chinese trade negotiators have reportedly resolved several longstanding disputes, paving the way for President Trump and President Xi Jinping to finalise a deal when the two leaders meet on the sidelines of APEC this week. US Treasury Secretary Scott Bessent confirmed the proposed 100% tariff hike on Chinese imports is off the table, which removes a major overhang. China, in turn, is delaying its rare earth export restrictions by a year, a meaningful gesture aimed at de-escalation. With the policy environment turning more constructive and geopolitical risks easing, Chinese equities could look appealing. Positioning is light, valuations are cheap, and even modest policy follow-through could unlock further upside. Execution risk is real but the risk/reward is skewed.

Gary Dugan – Investment Committee Member

Bill O’Neill – Non-Executive Director & Investor Committee Chairman

27th October 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person’s sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB