Click Here to Read the Full Version

For a brief moment late last week, it felt as though the global economy was ready to strike some sort of balance. Growth was solid and – albeit slowly – inflation was easing. Financial markets reflected a sense of stability characterised by an uneasy calm. US 10-year Treasury yields traded in a narrow 10-basis-point range around 4.20%, and global equity indices edged higher with some sector rotation.

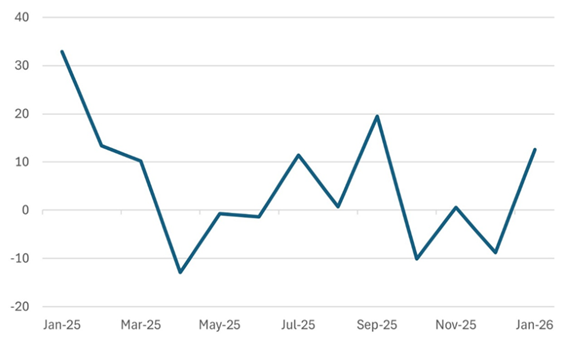

Healthy economic prints in the US supported the sense of stability, helping soften the slowdown narrative. Payroll growth appeared to have moderated without breaking; the unemployment rate eased to 4.4%. Most notably, US manufacturing sentiment surprised to the upside. Last week also saw the release of the Empire State Survey, which moved back into expansion at +7.7 from -3.7 for January, and the Philadelphia Fed Manufacturing Survey jumped to +12.6 from -8.8. New orders in both surveys improved. US Manufacturing appears to be stabilising rather than deteriorating, reinforcing the view that US nominal growth could remain near 4% to 4.5% rather than slipping sharply lower.

Chart 1: US Surveys Pointed to Strength in Manufacturing Sector

Index of balance of opinion

Source: Bloomberg

Against that backdrop, markets began pricing in a positive outlook. Inflation was drifting down, but the drift lower was not fast enough to push central banks to cut rates. Core US inflation remains sticky near 3%. Rate cuts are still expected in the US, but fewer and later. Nevertheless, equity markets took comfort in the economic resilience, while bond markets reflected balance in the economy rather than stress. For a brief window, it looked as though the global economy might show resilience and simply muddle through the first quarter.

Then the White House noise returned.

Trade rhetoric has resurfaced abruptly, aimed at European and NATO allies and placed back on the agenda as a political lever in the Greenland fiasco. Markets are now forced to pivot away from analysing economic data to assessing geopolitical uncertainty. The instances of the past year suggest that President Trump’s tariff threats should be treated sceptically but not entirely ignored. Even when diluted or delayed, they change corporate and central bank behaviour at the margin.

The economic impact of tariffs is asymmetric; for Europe, tariffs would be a growth problem. Export exposure to the US remains significant in autos, machinery, and capital goods, sectors that already face weak domestic demand. Most mainstream modelling suggests that a broad tariff shock could reduce euro area GDP by roughly 0.2 to 0.7 percentage points (pp) over the next 12 to 18 months. An economy growing at little more than 1% at best would find that impact material. It would not trigger an immediate crisis, but it would reinforce stagnation and further widen the growth gap with the United States.

For the United States, the impact would be inflationary. Tariffs function as a consumption tax. They raise prices without improving productivity or real incomes. The 2018 and 2019 tariff episodes show that between 70% and 100% of tariff costs were passed through to US import prices. Estimates suggest that a broad tariff programme could add around 0.1 to 0.3 pp to headline inflation over a year. While that may sound manageable, in a world where inflation is easing only grudgingly and the Federal Reserve is seeking confirmation that inflation has returned to a lower range, it matters.

The announcement of the tariff increases was made on Saturday, meaning markets had not yet had the opportunity to fully price or assess the implications. While precedent suggests that President Trump reserves the right to change his mind, such announcements tend to raise uncertainty, influence business sentiment, and alter risk premia at the margin. Legal challenges to the tariffs remain unresolved, with the Supreme Court still weighing the limits of executive authority over trade policy. Political resistance is also more visible than in previous cycles. Inflation has evidently become a far more sensitive issue for voters, and there is unease even within the Republican Party about policies that risk pushing prices higher. Corporate America, meanwhile, has little appetite for renewed supply chain disruption.

That explains the potential disconnect between rhetoric and pricing. Markets may eventually assume that the probability-weighted likely outcome is delay, dilution, or negotiation rather than immediate escalation. That judgement may prove correct, but it is not cost-free. Policy uncertainty itself carries some risks: Investment decisions are postponed, supply chains are hedged rather than optimised, and confidence becomes more fragile.

The deeper issue is not tariffs alone but the environment in which they sit. Policy has become louder, more personalised, and less predictable. Markets can live with bad news and withstand tight policy, but they struggle with sustained uncertainty. Events unfolding over the last week and into the weekend illustrated how quickly the narrative can shift from cautious optimism to renewed anxiety, even when the underlying data has not materially changed.

We are left in an uncomfortable middle ground. Beyond the headlines, the global economy is not faltering. US growth looks firmer than feared, manufacturing sentiment has stabilised, and financial conditions remain supportive. On the surface, however, the geopolitical noise is gaining momentum. The hope is that this proves to be another episode where rhetoric fades and pragmatism reasserts itself.

With Western ‘allies’ in a state of flux, global investor attention may be likely to continue to be on the opportunities in the east, which is a core theme of our 2026 Outlook. Japanese equities have reacted positively to the strong expectation that Sanae Takaichi, who became Japan’s first female prime minister last year, will imminently call a general election. The government’s current majority, with just 233 seats in the 465-seat lower house is razor thin, making parliamentary arithmetic fragile. Takaichi’s approval ratings have been relatively high, near 70% in some polls, reflecting personal popularity even as the LDP’s overall public support has been weaker. Some reports suggest she could dissolve the lower house around 23 January, setting up the February election as a test of her mandate and approach to economic and security policy.

Economically, the timing of the Japan election injects uncertainty into fiscal policy and budget implementation but is seen as a net positive. Japan faces structural pressures, including a weak yen, modest inflation, and demographic headwinds. Takaichi is reportedly considering campaign pledges such as suspending the 8% sales tax on food, which could cut government revenue by roughly 5 trillion yen (around $30 billion) annually if enacted.

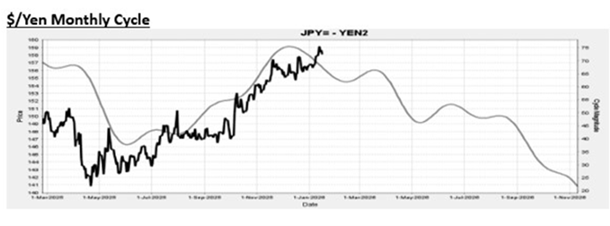

Technical analysis from Bill Sarubbi of Market Cycles suggests we are close to the peak of weakness in JPY versus the USD.

Chart 2: Technical Signal Suggests a Greater Risk of a JPY Rebound Versus the USD

Source: Bloomberg

Commodity markets consolidated over the past week. Oil prices drifted lower last week despite persistent geopolitical tension, with Brent trading back towards the low $80s per barrel. Industrial metals were mixed. Copper stabilised after recent weakness, holding around $3.7 per pound and reflecting the tension between soft global manufacturing data outside the US and structurally rising medium-term demand linked to electrification and data centre investment. Gold and silver remained firm near record highs, signalling that investors continue to hedge fiscal risk, geopolitical uncertainty, and longer-term currency debasement rather than near-term inflation shocks. Overall, commodity prices point to an environment of subdued cyclical momentum but a step-up in persistent strategic demand in a world with broken supply lines.

Gary Dugan – Investment Committee Member

Bill O’Neill – Non-Executive Director & Investor Committee Chairman

20th January 2026

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person’s sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB