Click Here to Read the Full Version

US economic data continues to look solid on the surface, yet retrospective revisions and internal distortions are steadily eroding confidence. Investors are being asked to price assets off numbers that may not withstand scrutiny six months from now. The issue is no longer simply whether growth is slowing, but whether we can fully trust the data defining it. Asia, on the other hand, is a picture of confidence, executing policy with clarity and scale. Markets are beginning to recognise the divergence and where more compelling value may lie.

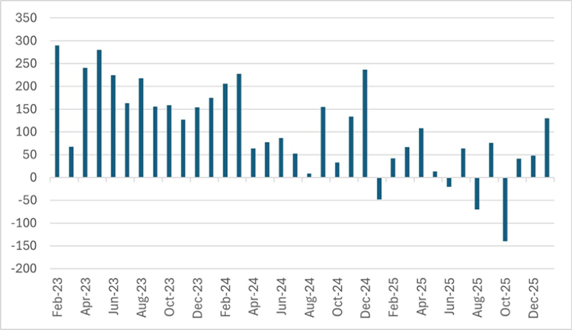

Now, some context. The January US employment report showed nonfarm payroll growth of 130,000, against expectations of 75,000, and an unemployment rate that edged down to 4.3% from 4.4%. Ordinarily, that would reinforce the soft-landing narrative. However, the Bureau of Labor Statistics simultaneously revealed that overall job growth in 2025 totaled just 181,000 positions rather than the 584,000 previously reported. A downward revision of more than 400,000 jobs outside recessionary conditions is not statistical noise – it is a structural credibility issue. If last year’s strength was overstated, the apparent ‘stability’ that we see today deserves a more cautious interpretation.

Chart 1: US employment growth month-to-month

‘000

Source: Bloomberg

Inflation is Cooling, But not Uniformly

Headline CPI slowed to 2.4% year over year in January from 2.7% in December, with a 0.2% monthly increase that undershot consensus. Treasury markets responded predictably, with the 10-year yield falling toward 4.05% and the 2-year settling near 3.5%. Rate markets now price roughly two quarter-point cuts in 2026, with June viewed as the earliest plausible starting point.

That optimism may prove premature. Core inflation accelerated to 0.3% month over month in January from 0.2% in December. Services inflation remains sticky, and airfares surged 6.5% in a single month. Producer price indices continue to signal tariff passthrough that has not yet appeared in consumer data. If those pressures emerge in the second quarter, the disinflation narrative could break down quickly. Meanwhile, the Federal Reserve is being pushed by political pressure, leadership transition uncertainty, and imperfect data. Markets are pricing a degree of policy confidence that may not be fully justified.

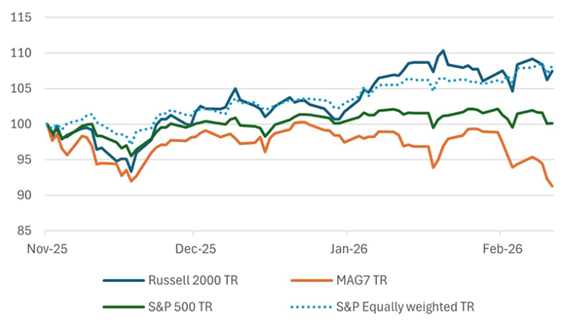

Ongoing Equity Market Rotation by Sector and Country

The S&P 500 closed the week at 6,836 and the Dow Jones Industrial Average crossed the 50,000 milestone briefly last Thursday. Earnings have delivered a fifth consecutive quarter of double-digit growth and market breadth has improved meaningfully. On the surface, the bull market remains intact. As Bill Sarubbi of Cycles Research noted late last week, even on a weaker day, there were 370 new highs versus 134 new lows, with weakness concentrated in technology.

Beneath the headline indices, equity leadership is clearly rotating. The equal-weight S&P has outperformed the capitalisation-weighted index by more than 300 basis points year to date. During this period, the Russell 2000 has advanced more than 8% compared with roughly 2% for the headline S&P. Only one of the mega-cap technology leaders is making new highs alongside the broader market. That is not random dispersion – it is rotation away from prior concentration.

Chart 2: MAG 7, Russell 2000, and Equally Weighted S&P500 Indices Since the Start of 2026

1st Jan 2026 =100

Source: Bloomberg

This shift matters. A market dependent on a handful of technology names is inherently fragile, whereas a market broadening into small- and mid-caps is structurally healthier. Moreover, the rotation also signals that the era of indiscriminate mega-cap dominance is fading. A continued concentration in crowded technology trades assumes that the previous market regime will reassert itself. History suggests otherwise.

AI: Enhancement Versus Displacement

Amid all the hullabaloo, the market’s reassessment of artificial intelligence is accelerating. Last week, brokerage businesses such as Charles Schwab came under pressure as markets questioned whether AI-driven portfolio construction could weigh on traditional brokerage and asset management economics. If portfolio design and allocation become increasingly automated, fee structures across parts of the industry will face structural pressure.

Conversely, logistics and supply chain operators are demonstrating how AI can help expand margins without wholesale labour destruction. They have shown how route optimisation, inventory automation, and integrated procurement systems enhance productivity while preserving human capital. The dispersion between sectors being enhanced and those being displaced may widen over the next 12 months, increasing differentiation across industries.

Japan: Strong Leadership with a Mandate for Growth

Japan delivered the week’s most strategically significant development. Prime Minister Sanae Takaichi’s ruling Liberal Democratic Party secured a two-thirds supermajority, winning 316 of the 465 lower house seats. This is not incremental political strength – it is governing authority with room to execute.

Takaichi’s proposed two-year suspension of the sales tax on food would inject approximately five trillion yen into the economy. Fiscal expansion layered onto gradual monetary normalisation has the potential to alter earnings trajectories, particularly for exporters and defense-adjacent sectors. The Nikkei responded decisively. The yen remains weak. This dynamic highlights the potential impact of currency movements on international equity returns, particularly where earnings acceleration coincides with FX volatility.

Japan now offers something increasingly scarce in developed markets: political clarity aligned with pro-growth policy. Persistent underweight positioning in Japan may reflect historical allocation patterns rather than current fundamentals. Current conditions appear supportive.

Chart 3: Topix Index Relative to MSCI World ex Japan

Source: Bloomberg

China: A Structural Redeployment of Household Savings

China’s story is not stimulus-driven speculation. It is structural reallocation. Approximately 50 trillion yuan in time deposits mature this year after multiple rounds of deposit rate cuts pushed yields toward 1%. Capital is unlikely to remain idle at those low levels of interest rates.

Estimates suggest that between two and four trillion yuan could migrate into wealth management products, insurance vehicles, and equities this year. Retail brokerage account openings have already surged and technology-oriented indices are posting double-digit gains. This is rational asset migration responding to compressed deposit yields.

From a benchmark construction perspective, inclusion factors and weighting methodologies remain relevant considerations. In the MSCI ACWI framework, China’s weight is constrained by partial inclusion of A-shares and other structural factors. China typically accounts for roughly 3% to 5% of the index depending on methodology. If A-shares were included at full inclusion factors and treated comparably to developed markets, China’s weight could plausibly jump to 8% to 12%. That context provides perspective on how China’s representation within global indices could evolve under different inclusion methodologies.

Chart 4: China’s household sectors Savings options Low Interest rates or a Rising Equity Market

Source: Bloomberg

China met its 5% GDP growth target in 2025 despite export headwinds from the United States, as stronger trade with ASEAN and Belt and Road partners offset those headwinds. The deposit maturity wave creates a durable domestic liquidity tailwind. This is not about short-term stimulus headlines – it is about household balance sheet behaviour potentially shifting to risk assets at scale. That being said household confidence remains low and it will be a leap of faith, or excitement about equity market gains, that motivates households to spend or save in riskier assets.

Europe: Stability Without Momentum

The European Central Bank held rates at 2.0% as inflation eased toward the bank’s target. Growth projections remain modest. Europe offers valuation support and macro stability, but it lacks catalytic force. Absent a geopolitical resolution that unlocks reconstruction spending and stronger investment cycles, the region’s outlook may remain steady but lacking strong catalysts.

Fixed Income and FX: Asymmetric Risks

The bond market rally reflects confidence in sustained disinflation, but that confidence remains fragile. Sub-4% yields on the 10-year Treasury offer limited compensation for fiscal expansion and potential tariff passthrough. Duration exposure may be sensitive to upside inflation surprises. In foreign exchange, modest dollar softness and yen strength reflect shifting rate expectations and Japan’s political clarity.

The Strategic Divide is Widening

The core takeaway from the week is structural rather than tactical. The United States is navigating statistical opacity and political crosscurrents. Europe is managing stability but there is hardly any dynamism. Asia, particularly Japan and China, is deploying decisive policies and catalysing capital movement.

These evolving dynamics are likely to influence asset allocation discussions. Japanese equities currently exhibit characteristics associated with fiscal clarity and earnings leverage. China’s deposit maturity cycle represents a notable domestic liquidity dynamic. US equity markets continue to be influenced by concentration dynamics within mega-cap names. As AI reshapes sector economics, technology sector outcomes are likely to depend increasingly on monetisation discipline and earnings visibility.

Markets often favour alignment with emerging momentum while reassessing assets tied to fading narratives.

Gary Dugan – Investment Committee Member

Bill O’Neill – Non-Executive Director & Investor Committee Chairman

16th February 2026

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person’s sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB