Click Here to Read the Full Version

Exceptionalism Tested, Duration Mispriced, and the Search for Stability

The week just gone by may eventually come to be seen as one of those inflection points where several structural narratives converged at once. The immediate catalyst was legal, but the implications are macroeconomic, fiscal, and psychological.

US Exceptionalism Under Strain

The ruling by the Supreme Court of the United States against the administration’s broad use of emergency authority to impose tariffs bears significant consequences. The decision does more than just limit executive trade discretion. It reopens the question of US institutional consistency and fiscal sustainability.

The potential for large-scale repayments of up to $170 billion (about 0.6% of GDP) to companies that paid tariffs under the now invalidated authority introduces a new fiscal variable. Even if those repayments are staggered or legally contested, the prospect alone widens perceived deficit risk. That matters in a market already sensitive to Treasury supply. Markets will treat the possibility of repayments as an incremental addition to expected Treasury supply. In an environment where issuance is already heavy, even marginal shifts in supply expectations matter for duration pricing.

Compounding the legal shock was the policy reaction. Within hours of the ruling, the President announced a universal 10% tariff under alternative statutory authority, only to pivot to a 15% rate shortly thereafter. While the economic substance of those numbers is significant, the signalling effect of knee-jerk reactions is more important. Thankfully in recent hours there appears to have been a clarification that the US will honour the trade deals with individual currencies.

For decades, US exceptionalism was defined not only by economic scale and military dominance, but also by institutional predictability. Markets could price risk around policy because the framework governing those policies was stable. Cut to present and what unsettles investors now is not merely tariffs, but volatility in decision-making. Abrupt shifts, emotionally charged rhetoric toward trading partners, and rapid escalation alter investors’ perception of risk.

The end-of-week events feed a broader narrative already circulating in global capital markets: that the dollar’s unquestioned dominance may be in abeyance, and that US assets, long considered structurally safer than peers, may now require a higher risk premium. Whether that proves cyclical or structural remains to be seen, but the direction of travel in investor psychology is notable. The dollar’s performance in the opening days of the week may provide further insight into investor sentiment.

Chart 1: US Dollar Spot Index May Have further Downside Risk

Source: Bloomberg

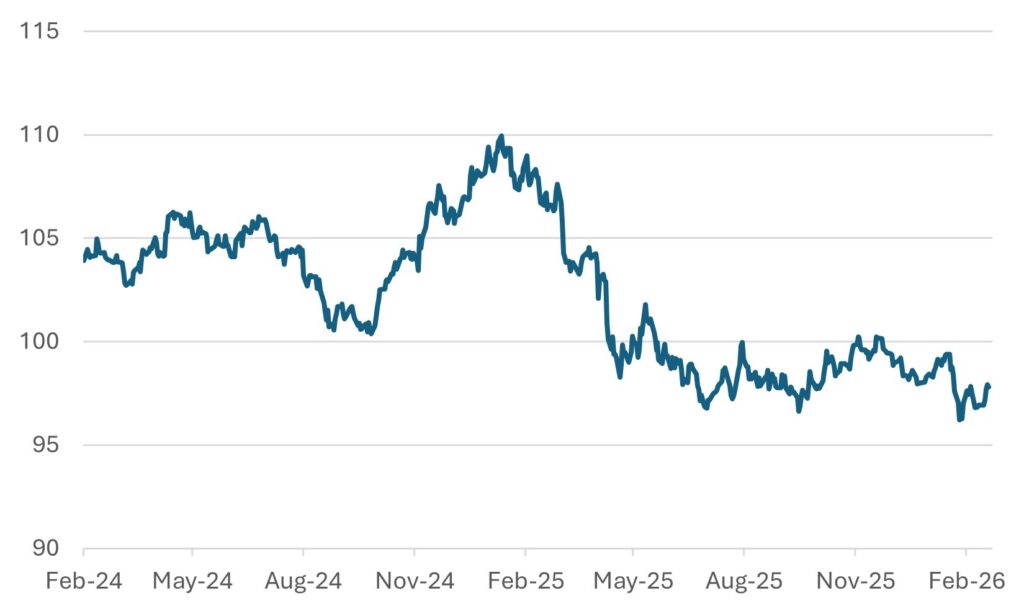

The 10-Year Yield and Structural Risk Premium

Against that backdrop, the US 10-year Treasury yield spent the week hovering close to 4.0%. On the surface, that level reflects moderating growth and inflation expectations. Beneath the surface, however, valuation levels may warrant closer examination in the current context. Structurally, however, the larger issue is not inflation arithmetic but term premium. If tariff repayments (at around 0.6% of GDP), expand the deficit and issuance rises, and if policy volatility increases uncertainty around fiscal discipline, investors will demand greater compensation for holding long-duration assets. Inflation expectations may adjust at the margin, but it is confidence in fiscal and institutional stability that ultimately determines the term premium.

Chart 2: US 10-Year Looks Mispriced

Source: Bloomberg

The latest minutes from the Federal Reserve underscored an understandable reluctance to cut rates prematurely. The minutes from the 28 January Federal Open Market Committee meeting show policymakers are wary of reigniting inflation, particularly given renewed tariff pressures. Markets that had leaned toward earlier easing were forced to recalibrate.

Structurally, however, the bigger issue may be term premium. If tariff repayments add to the deficit, issuance will rise. If fresh tariffs lift prices again, inflation expectations could reaccelerate. And if investor confidence in fiscal discipline weakens, long-duration bonds will warrant greater compensation.

For years, Treasuries benefited from a suppressed term premium due to central bank buying, regulatory demand, and the dollar’s reserve status. That bedrock is less certain today. Foreign official purchases have moderated in recent years. Retail ownership remains a single-digit share of the overall Treasury market, but it has grown meaningfully and steadily since 2021. The significance of growing retail participation in the Treasury market lies less in the headline percentage and more in the character of the marginal buyer, which is increasingly more yield-sensitive and flow-driven. Institutional anchors such as foreign central banks, pension funds, and insurers still dominate the stock of outstanding Treasuries, but incremental flows are increasingly influenced by retail behaviour. Retail capital is more yield sensitive and more responsive to volatility. In a market where supply is expanding and fiscal uncertainty is rising, the composition of demand matters as much as the quantity.

In that context, a 10-year yield of 4.0% may not fully reflect a backdrop of fiscal expansion, policy volatility, and geopolitical fragmentation. Any adjustment in long yields would likely influence domestic financial conditions and global asset allocation dynamics.

The recent episode at Blue Owl Capital Inc. is instructive in this regard. Redemption pressures in one of its retail-oriented private credit vehicles forced adjustments to withdrawal terms and asset sales, unsettling investors across the alternatives complex. The issue was not credit quality per se, but the dynamics governing liquidity and flow. When retail capital becomes a meaningful participant in asset classes traditionally dominated by long-duration institutional money, volatility increases at the margin. There are potential parallels for Treasury market dynamics. As the investor base shifts, even slightly, toward more flow-driven participants, the stability premium that once characterised duration markets diminishes.

China’s Momentum Question, but EM Still Looks Good

While institutional volatility in the US is shaping global risk premia, the next directional move in cyclicals will still depend heavily on China’s domestic momentum. The question is simple: where is the momentum?

Post-holiday data in China have yet to convincingly demonstrate a durable upswing in domestic demand. External demand now faces renewed tariff uncertainty. If Beijing signals conservative growth targets, global commodities and cyclical equities could soften. Conversely, forceful stimulus would buoy risk assets but at the cost of further leverage concerns.

China’s trajectory remains central to commodity currencies, export economies, and global manufacturing supply chains. In a week defined by US legal and fiscal drama, the quieter uncertainty around Chinese growth should not be overlooked.

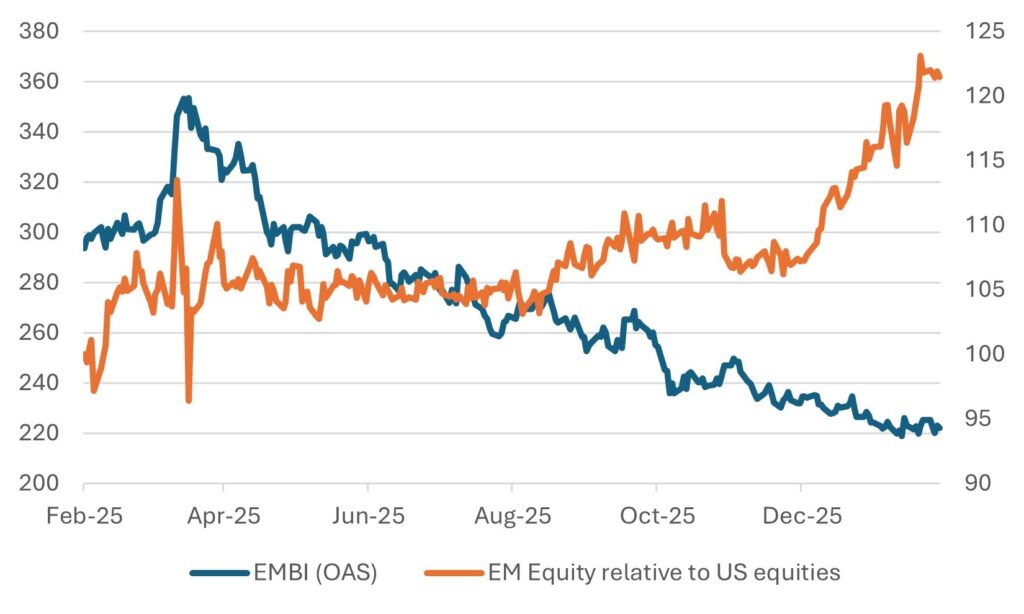

Emerging market assets may experience relative support amid heightened uncertainty in the US. Interest in EM debt and equities could increase as EM countries march ahead on monetary easing. Last week, the Philippines cut rates, and others will likely follow. This week the Bank of Korea and Bank of Thailand are expected to leave rates unchanged, but they will likely adopt a dovish stance. In Latin America, the story remains about growth where economists expect a re-acceleration in the coming quarters. JP Morgan expects an imminent re-acceleration in growth in both Mexico and Brazil. In relative terms, emerging markets could see relative performance shifts as perceptions of US risk premia evolve.

Chart 3: The recent rally in EM debt and EM equity may extend further

OAS (rhs), EM equity relative (rhs, rebased to -1Y=100)

Source: Bloomberg

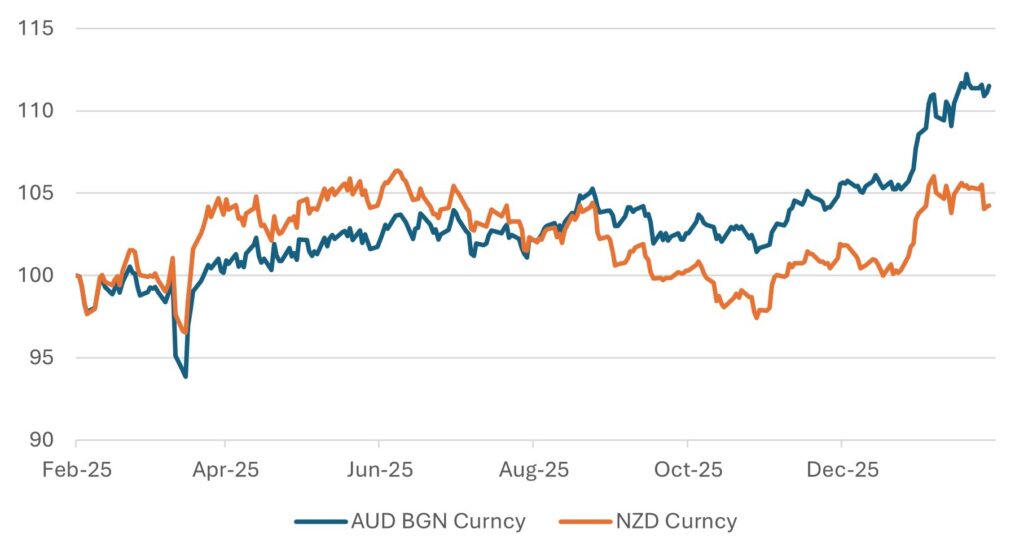

Australia and New Zealand as Relative Beneficiaries

As investors look for havens of consistency, Australasia has attracted increased attention in this context. In fact, The Guardian highlights a clear rise in American interest in relocating to New Zealand, particularly among high-net-worth individuals. Under New Zealand’s revamped investor “golden visa” scheme, wealthy Americans account for nearly 35% of applicants, roughly 617 out of 1,833 since the programme began, overtaking applicants from China and Hong Kong. Many cite political uncertainty in the United States and lifestyle considerations as key motivations. More broadly, around 28,000 US-born residents now live in New Zealand, a 29% increase over five years, indicating that the trend predates the current momentum but has gained visibility. While this does not amount to a mass exodus, it does point to a discernible uptick in relocation interest among Americans with capital and portable skills, reinforcing the narrative that stable, rules-based jurisdictions are becoming more attractive at the margin.

Against the US backdrop, Australia and New Zealand economies appear comparatively steady. The countries’ respective central banks have maintained disciplined fiscal stances, keeping policy rates elevated to ensure inflation credibility. Higher rates in this context are not punitive. They signal orthodoxy.

Fiscal positions in both Australia and New Zealand remain more contained relative to major developed peers. Their bond markets offer yield support without the same scale of deficit overhang. The Australian dollar and New Zealand dollar retain cyclical sensitivity, but they also benefit from positive real yield differentials.

Growth forecasts are moderate rather than spectacular, yet institutional credibility, diversified export bases, and demographic support, particularly in Australia, provide resilience. These economies may not be havens in the traditional sense, but in a world of rising policy noise, they offer stability. In this context, the Australian and New Zealand dollars may exhibit characteristics that differ from traditional high-beta risk currencies during periods of US policy turbulence.

Chart 4: Australia and New Zealand Dollars Recover and Progress Versus the USD

Source: Bloomberg

Gary Dugan – Investment Committee Member

Bill O’Neill – Non-Executive Director & Investor Committee Chairman

23rd February 2026

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person’s sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB