Click Here to Read the Full Version

Markets still looked too relaxed….. at least until this morning.

Friday’s sell-off in US equities may prove to be the first small crack in what has otherwise been a remarkably composed response to a deteriorating global backdrop. Riding on last year’s strong rally, equities remain close to highs. Bond yields have advanced, but not yet to levels that fully reflect renewed inflation worries. Markets are still pricing a contained, temporary shock. That may ultimately prove too generous.

Chart 1: US equities and Bonds extend their sell-off

Source: Bloomberg

A more uncomfortable admission would be that we may only be in the early stages of a broader macro repricing. An energy shock of an uncertain duration, weakening consumer and business confidence, a Federal Reserve unwilling to ease quickly, and a geopolitical situation offering little sign of resolution is not a benign mix.

Hard economic data still look respectable. Global economic growth is tracking close to 2.8% annualised, and PMIs are consistent with expansion. Yet, leading indicators are softening. Business expectations and consumer confidence are slipping, while inflation pressures are beginning to rebuild. These are early warning signs that the market is choosing to ignore.

Energy remains the fulcrum at this juncture. A sustained 10% rise in oil prices typically boosts global inflation by 40 basis points and trims growth by up to 0.2%. While that can be managed once, it is not manageable on a sustained basis. Current projections point to global CPI drifting back towards 3.5%, with higher energy costs already feeding into monthly inflation prints.

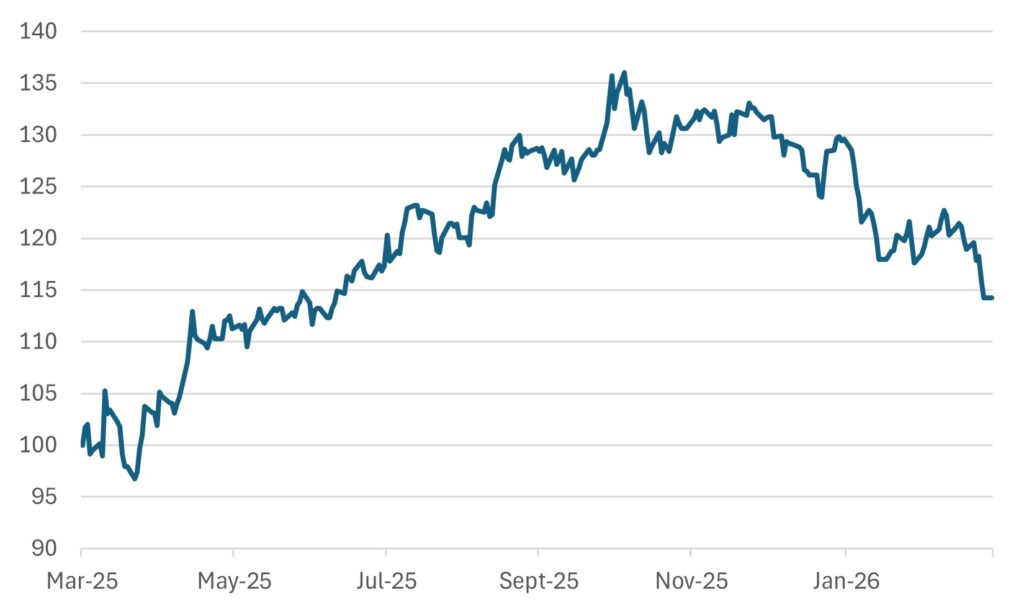

Chart 2: Brent Oil Breaks to New Highs ($bbl)

Source: Bloomberg

Bond markets have yet to fully absorb this. Real yields remain modest relative to inflation risk. It would not be surprising to see another 20–50 bps added to, say, US 10-year yields if markets begin to accept that inflation is proving sticky again. The Federal Reserve is likely to hold rates steady at around 3.75%, reflecting, on its part, caution rather than comfort. That leaves markets without the expectation of an imminent policy support to help keep the surging dollar in check.

Market positioning reinforces the sense that investors have not yet fully adjusted to the changed reality.

Equity inflows remain broadly supportive, particularly into US large-cap and technology-heavy strategies. Passive flows continue to dominate, with ETFs absorbing the bulk of allocations. There has been some rotation into energy and commodities, but not on a scale consistent with the increased likelihood of a prolonged supply shock. However, one standout feature has been the heavy selling in Asian equities, as investors bet that Asian economies, which rely heavily on imported energy, will suffer significant downside to growth.

In fixed income, flows have cautiously returned to investment-grade credit, encouraged by higher yields. Yet, spreads remain relatively tight, suggesting that investors are still not demanding significant compensation for rising macro uncertainty. Global high yield spreads have widened 70 bps in just the past few weeks.

More broadly, volatility positioning remains subdued, and systematic strategies, overall, remain long risk assets. Cash allocations are not elevated. In sum, this points to a market that has not yet positioned for a regime shift.

Flows tend to move late. When they turn, they tend to turn quickly.

The technology sector is beginning to confront a different type of risk. The issue is no longer simply whether valuations are stretched; it is whether the physical inputs required to sustain the AI and semiconductor build-out can be delivered reliably and at reasonable costs. Helium shortages, linked to disruptions in Middle Eastern supply, are already affecting semiconductor production. Rare earths and specialised materials are becoming more politicised as China’s tighter export controls and longer lead times affect supplies to global markets. What is even more concerning is that key chip manufacturing hubs such as Taiwan and South Korea remain heavily dependent on imported energy. Recent data already show upward pressure on technology input costs, including a 1.1% month-on-month rise in US non-fuel import prices, driven by technology-related components.

Chart 3: MAG 7 relative price performance to SP500 ex MAG 7

rebased to March 25=100

Source: Bloomberg

Amidst all the chaos, China appears relatively better placed, at least in the near term. Higher energy inventories, a more diversified supply base, and policy flexibility provide a buffer. Growth expectations remain around 4.7%, with inflation pressures likely to be felt more in producer prices than at the consumer level. However, vulnerabilities are more visible elsewhere. Energy rationing has begun in parts of India, while Vietnam and the Philippines have moved into emergency footing. Growth is likely to slow materially in the near term, with the familiar sequence of currency pressure, rising inflation, and tighter financial conditions beginning to bite.

There is a tendency to underestimate the scale of the current geopolitical risk.

Iran is not Iraq. It is not Vietnam.

Iran has a population of roughly 90 million and a landmass of approximately 1.6 million square kilometres. It is a large, complex, and geographically diverse country.

In Iraq, the United States’ fight was not against the entire population. The insurgency was largely concentrated in Sunni regions, representing perhaps 5–10 million people at the core of resistance. Even then, with around 170,000 troops at peak deployment, the conflict extended over roughly eight years.

Vietnam offers another perspective. The United States was primarily engaged against North Vietnam, with a population of roughly 18–20 million. Despite deploying more than 500,000 troops and sustaining a prolonged military effort, it did not achieve a decisive outcome.

Iran is materially larger than both in population and scale. It is also geographically more complex. Mountain ranges such as the Zagros and Alborz create natural defensive barriers across much of the country. In comparison, Afghanistan, for all its reputation, has a much simpler terrain. Iran combines mountainous defences with urban density, infrastructure, and industrial depth.

The conclusion is not political; it is structural. Iran cannot be subdued quickly or without incurring significant costs. Any escalation risks becoming prolonged, resource-intensive, and regionally destabilising.

Markets are not pricing that reality. Markets may begin to reassess conflict-related risk premia if credible signs of negotiation emerge.

The coming fortnight carries more weight than usual. Markets will be looking for confirmation or contradiction of the emerging narrative with another Trump deadline marked for 7 April. In the meantime:

Overlaying all of this is the political calendar, with the approach to early April and key US policy milestones adding another layer of uncertainty.

The combination of softer growth signals and firmer inflation prints would be particularly challenging for markets.

Portfolio positioning may increasingly be influenced by a shift in the balance of risks.

Some market participants are reassessing equity exposure levels, with increased attention on energy sectors and a relative shift from growth to value and income-oriented strategies. China and Latin America are being rumored by some investors as potential sources of diversification, given their differing sensitivities to current geopolitical developments. . We see 10-year yields surging up to 50 bps in the near term; hence, shorter-duration positioning has gained traction among some investors in response to rising yield expectations, but credit markets may face increasing pressure if macroeconomic conditions deteriorate further. Global high yield has moved out to a 350-bp spread. Historical spread ranges suggest that further widening remains possible under more stressed conditions. Still, we would not really be at the extremes of risk-off. Commodities have historically acted as a hedge in environments characterised by supply constraints and rising inflation. It was interesting to see precious metals firm up towards the end of last week.

From a technical perspective, the recent sell-off in S&P 500 has been quite rare. As Bill Sarubbi of Cycles Research points out, “the market has now fallen for five consecutive weeks. This has occurred 16 times in 50 years. The following time periods were not strong. In the first week, the market was up four times. After four weeks, the S&P was up six of 16 times. The bearish tinge began to wear off after 12 weeks, up in 10 of 16 years”.

Absolute return strategies have recently attracted increased attention in the context of market volatility. Experience from recent periods of dislocation suggests that macro and trend-following approaches can provide meaningful diversification when both equities and bonds struggle. In 2022, macro hedge funds delivered positive returns, and managed futures strategies performed particularly strongly, highlighting their historical role in diversification during periods when both equities and bonds face challenges.

The message is not that recession has arrived. The message is that markets are still underpricing the probability of a shift in regime.

Growth remains intact, for now. Confidence is weakening. Inflation risks are rebuilding. Supply chains are tightening.

And markets continue to behave as though the shock will pass. History suggests that when conditions look like this, the adjustment is usually still ahead, not behind.

Gary Dugan – Investment Committee Member

Bill O’Neill – Non-Executive Director & Investor Committee Chairman

30th March 2026

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person’s sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB