Click Here to Read the Full Version

Markets enter the week facing the same unresolved equation that has characterised the past two months: a Gulf conflict barely eight weeks old, a Federal Reserve in leadership transition, and an equity market eyeing the certainty that the macro backdrop does not yet support. The temptation to discount the problems, to assume the ceasefire holds, energy prices normalise, and central banks resume gradualist easing, is powerful but, at this stage, premature. History suggests that in times such as these patience and scepticism are required in equal measure.

Three major rate decisions are due within a fortnight: The ECB meets 30 April, the FOMC on 1 May, and the Bank of England on 9 May. In normal times, this is a routine exercise, but then these are not normal times.

The ECB held rates steady in February, citing domestic resilience and inflation converging toward its 2% target. That assessment is now almost stale. Europe’s energy dependence on the Middle East, structurally greater than America’s, means the Hormuz price shock transmits more quickly and more sharply into European consumer prices. Christine Lagarde, the ECB president, meets the press after the meeting, she will face a difficult question: how is a hold defensible when the inflation outlook has visibly deteriorated? Expect “data-dependent” to carry more weight than the data itself.

The FOMC faces the same dilemma with an added complication: a Chairman who is on his way out. Consumer prices rose 0.9% in March, pushing annual headline inflation to 3.3%. Core inflation, at 2.6%, remains above the FOMC’s target but is slowing, and here lies the trap the markets have set for themselves. The critical distinction is not simply whether prices are rising. It is whether goods and services remain accessible at any price. The Hormuz closure, which has restricted approximately one-fifth of global oil trade, is a supply shock, not a demand-driven price event. Rate cuts do not reopen shipping lanes, restore refinery throughput, or repair the insurance markets that are currently pricing existential risk into every tanker in the region. A complete inflation picture will take four to six months to emerge as supply chain pass-through works its way into the data. The FOMC, with the 1970s firmly in mind, will not be rushed.

The Bank of England is arguably the most constrained of the three: European-scale energy exposure, a weaker currency buffer, and four rate cuts already delivered in 2025. It now faces the prospect of holding, or reversing, precisely when the domestic economy needs relief most. That contradiction will define the May meeting.

The path to confirmation as the Fed Chairman for Kevin Warsh, Trump’s nominee to replace Jerome Powell, cleared a material obstacle on Friday. The DOJ dropped its criminal probe against Powell, the sole condition Senator Thom Tillis had placed on releasing his hold on Warsh’s nomination. The White House is confident that confirmation will be completed before Powell’s term expires in May.

The 21 April hearing delivered two market-relevant headlines, on Fed’s independence and framework. On the institution’s independence, Warsh stated unequivocally that no commitment on rates had been sought or given by the White House. On framework, Warsh called explicitly for a “regime change in the conduct of policy”, a clear signal that the Fed’s inflation mandate will be reset, in both substance and communication. A fuller assessment of what Warsh is likely to introduce will be published later this week; clients should treat this as the preview.

The US equity market is up close to 13% from its end-March low, with gains concentrated almost entirely in two sectors: Technology and Energy. That narrow leadership is itself a signal. Higher inflation will erode household spending power; slower consumption growth, layered onto the prospect of structurally higher long-term rates, will weigh on the broader market. A sector-focused posture is warranted, and the case for each is set out below.

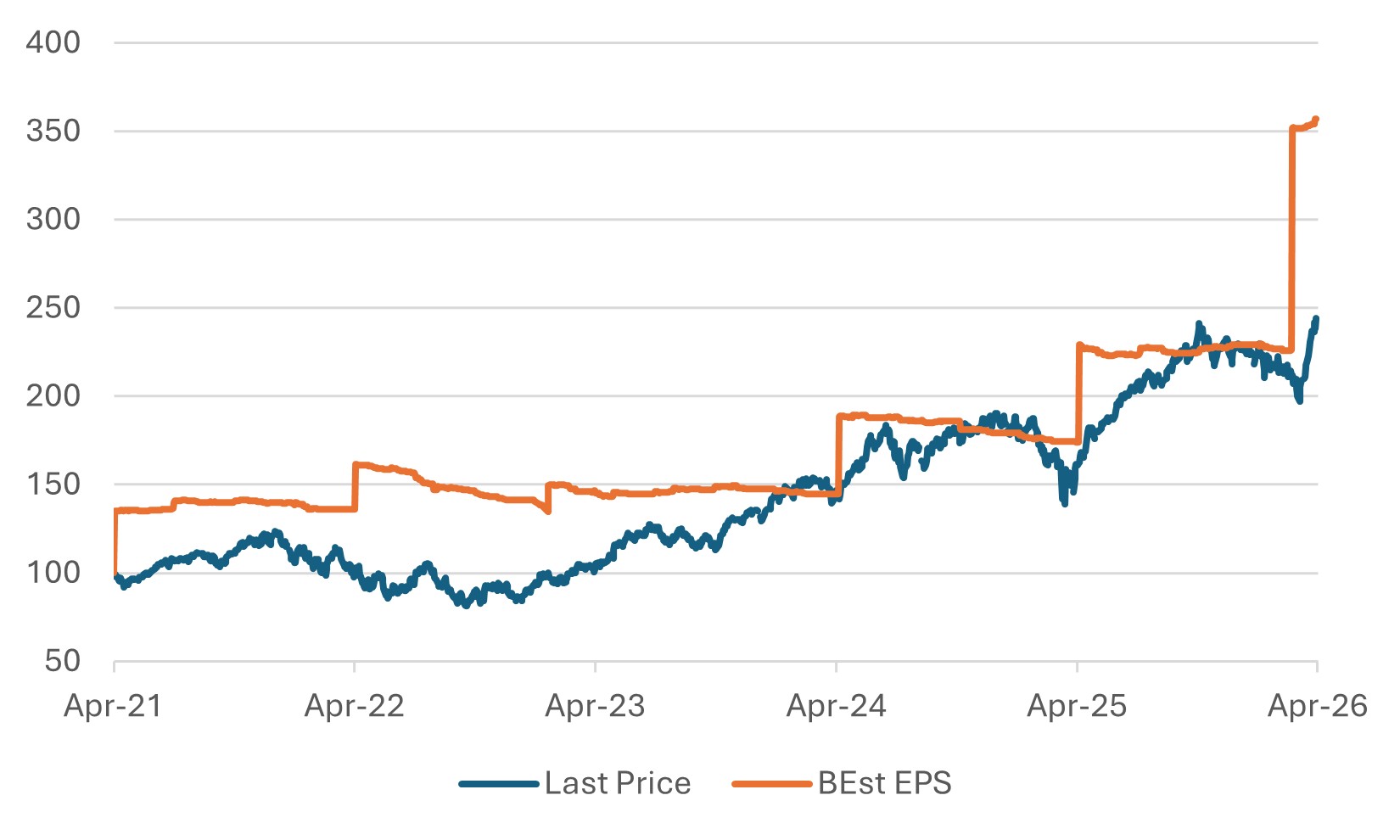

The S&P 500 Information Technology index presents an unusual picture: Street earnings expectations have run significantly ahead of where the index itself trades. In normal circumstances, this gap attracts re-rating. Today, however, it reflects a market pricing geopolitical and macro uncertainty well beyond what deteriorating fundamentals alone justify.

The caveat is real. Consensus estimates are partly built on AI productivity optimism, and the headcount reductions announced by Meta and Microsoft this past month introduce a question: are these measures efficiency plays, or the opening signal of capex restraint? If the latter, the multiple compresses further. The more probable reading is that the earnings trajectory is sound and the index is trading at a genuine discount to intrinsic value. For long-horizon clients, the entry point is compelling, conditional on the macro fog lifting on a rational timeline.

Chart 1: S&P500 Info Tech Sector Index Earnings Well Ahead of Price Index

Rebased to -5Y=100

Source: Bloomberg

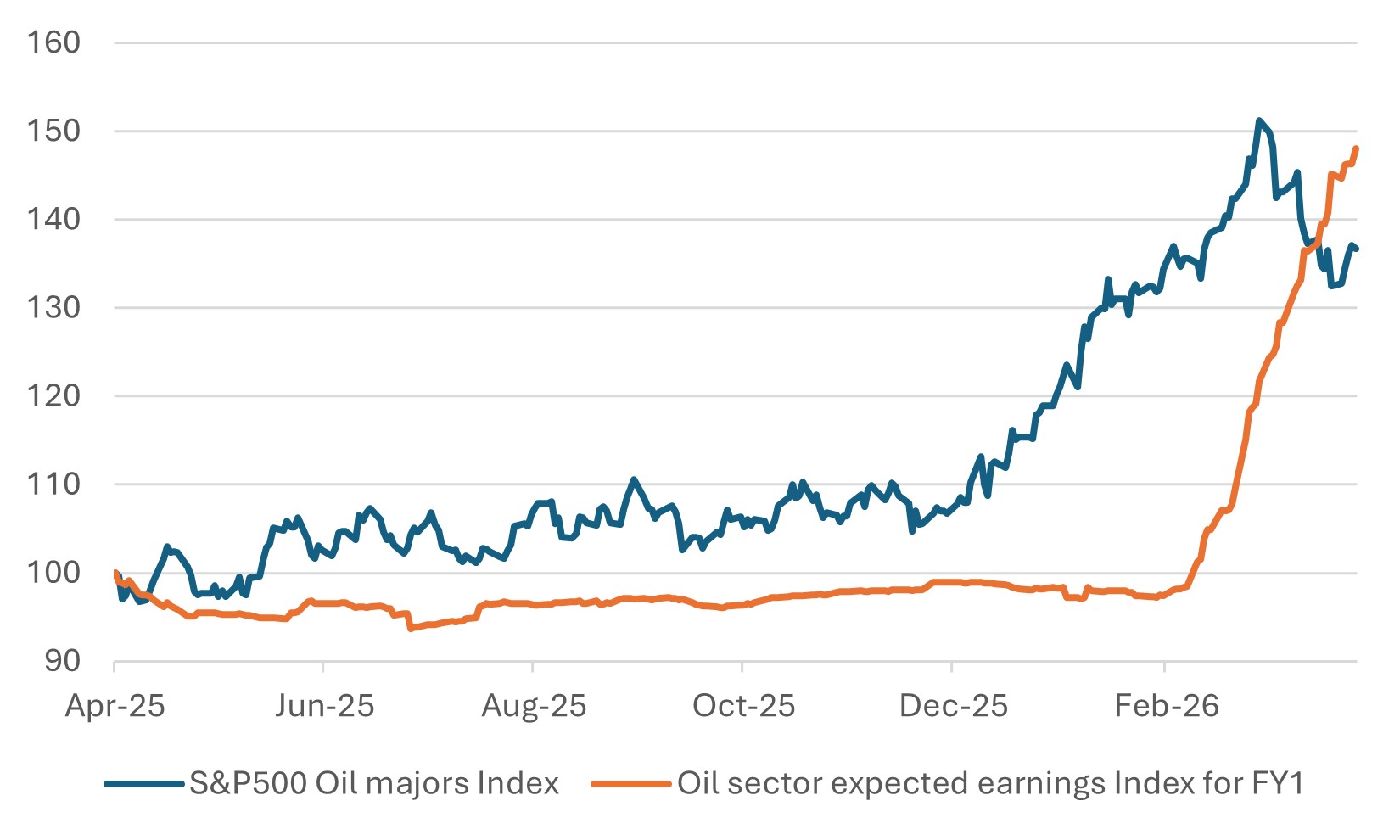

The Energy sector presents a more troubling story. Share prices have kept pace with upward earnings revisions, the S&P Oil majors index looks fairly valued relative to current forecasts. The problem is those forecasts almost certainly assume a swift, contained resolution to the Hormuz disruption.

Brent has risen more than 40% since the conflict began, last trading above $105 per barrel. Strait traffic remains well below pre-war levels despite the ceasefire. If disruption persists or resumes, energy earnings will materially exceed revised forecasts and the sector will re-rate sharply higher. If peace holds and throughput is fully restored, current prices are a ceiling, not a floor. That binary makes energy one of the most consequential sectoral positions available, but only for those who can form a credible view on a geopolitical timeline, which, at this stage, very few can.

Chart 2: US Oil Sector Sees Profit-taking but Consensus Earnings Forecasts Push Higher

Source: Bloomberg

Near-term disruption to price notwithstanding, the hope for eventual normalisation is not irrational, it is the desired long-run positioning in most environments. What makes it prone to error is the timing. Eight weeks in itself is not a resolution. The data that will define this cycle, Q2 CPI readings, shipping insurance trends, tanker utilisation through alternative routes, supply chain pass-through into core goods, does not yet exist. Central banks know this. Investors who have already priced in rate cuts should ask themselves whether they are discounting a resolution that is months, not weeks, away. Patience is not pessimism. In this market, it is the only defensible analytical position.

Gary Dugan – Investment Committee Member

Bill O’Neill – Non-Executive Director & Investor Committee Chairman

27th April 2026

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person’s sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB