Click Here to Read the Full Version

Investment conclusion: At the time of writing, market commentary increasingly reflects the view that a US-Iran peace deal is more likely than not. The initial market response to such a development is widely expected to involve a rotation away from recent crisis beneficiaries, energy, materials and technology, toward sectors and regions that underperformed during the disruption, including consumer discretionary, real estate, Europe, India and selected Gulf companies. The second phase of the rally will be less straightforward because the inflationary consequences of the disruption caused by the war will fade only gradually.

Financial markets increasingly need to consider a scenario in which the United States and Iran finally reach an agreement, sanctions on Iranian oil are eased, and the Strait of Hormuz reopens. At the time of writing, a final agreement has not yet been reached, and the terms and timing of the deal remain uncertain. Iranian and American statements nevertheless suggest that the negotiations have progressed far enough for markets to begin anticipating the investment consequences.

The immediate response to the agreement is likely to be instinctive: buy what has fallen and sell at least some of what has gone up. Markets rarely wait politely for every sign. They discount the future, sometimes with all the delicacy of a rugby scrum.

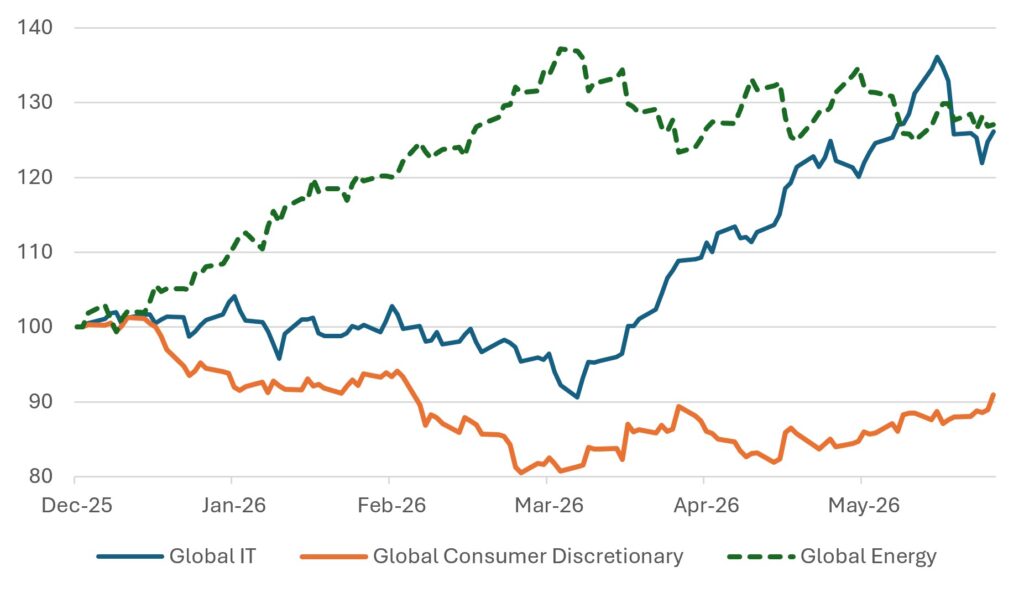

The performance data already tells a striking story. Year to date, global energy equities have surged approximately 27%, information technology 19%, and materials nearly 13%. By contrast, global consumer discretionary is down almost 4%, India is down more than 11%, and Dubai and Abu Dhabi remain modestly lower.

Chart 1: Sharp Divergence of Sector Performances Since Start of the Year

Rebased to Dec 31st 2025=100

Source: Bloomberg

Energy and materials have benefited directly from scarcity, supply disruptions, and a higher geopolitical risk premium. Technology has not been a Middle East trade in the same sense. However, weak global growth and uncertainty saw an inordinate amount of capital seek refuge in the relatively small group of companies still offering visible secular growth. This dynamic overlaps with, but is not entirely explained by, the ongoing AI investment cycle. Commentators have noted that a diplomatic settlement could lead to profit-taking in technology, even if the sector’s long-term fundamentals remain intact.

In previous rotations of this kind, capital has tended to flow toward consumer discretionary, travel, selected industrials and real estate. Large consumer names are among those discussed as potential beneficiaries of improved confidence and lower energy and distribution costs. The important point is not simply that the market rises, but that leadership broadens.

Europe is widely cited as among the regions most likely to benefit. For some time now, the region has remained unusually exposed to imported energy prices and the consequences of disrupted trade. A reduction in the oil and gas risk premium would improve the growth outlook and reduce the immediate pressure on the European Central Bank to deliver another rate increase.

The ECB would not be able to declare victory, however. The delayed ripple effects of inflation already generated by higher energy, freight, and supply-chain costs will continue to pass through the economy for some time. Nevertheless, the worst-case scenario would likely be behind us, creating room for a rebound in European equities, particularly consumer, real estate, and domestically sensitive companies.

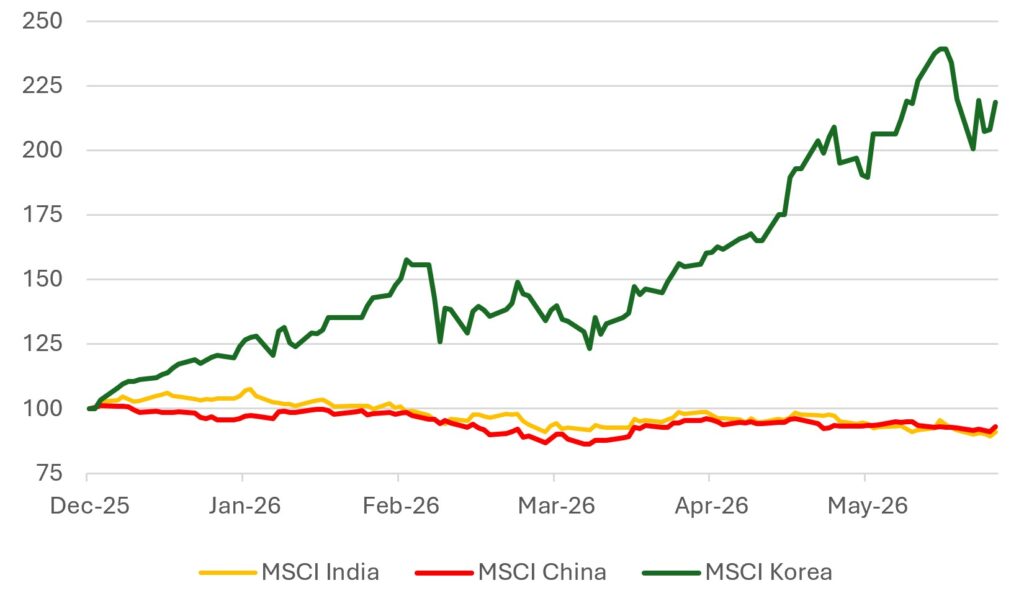

Asia should also benefit, but the effects will differ sharply by country. India stands out. The Sensex, the primary barometer of India’s economic health, is down roughly 11% this year while global equities are up around 5%. Higher imported energy costs, pressure on the rupee, and attempts to preserve currency stability have weighed heavily on investor sentiment.

India’s structural growth story has not disappeared. It has been obscured by an exceptionally unwanted combination of expensive energy, a weak currency, and reduced international risk appetite. An improving energy supply scenario, a lower oil risk premium, and reduced pressure on the rupee would support both the external balance and domestic confidence. Valuations still matter, but India now has far greater scope to respond positively to good news than markets already near their highs.

China could also benefit from lower energy uncertainty and improved regional trade. The likely response may be less explosive than in India, but a more stable global growth outlook would help industrial activity, consumer confidence, and international capital flows.

Chart 2: Sharp Divergence of Asian Equity Performances Since Start of the Year

Rebased to Dec 31st 2025=100

Source: Bloomberg

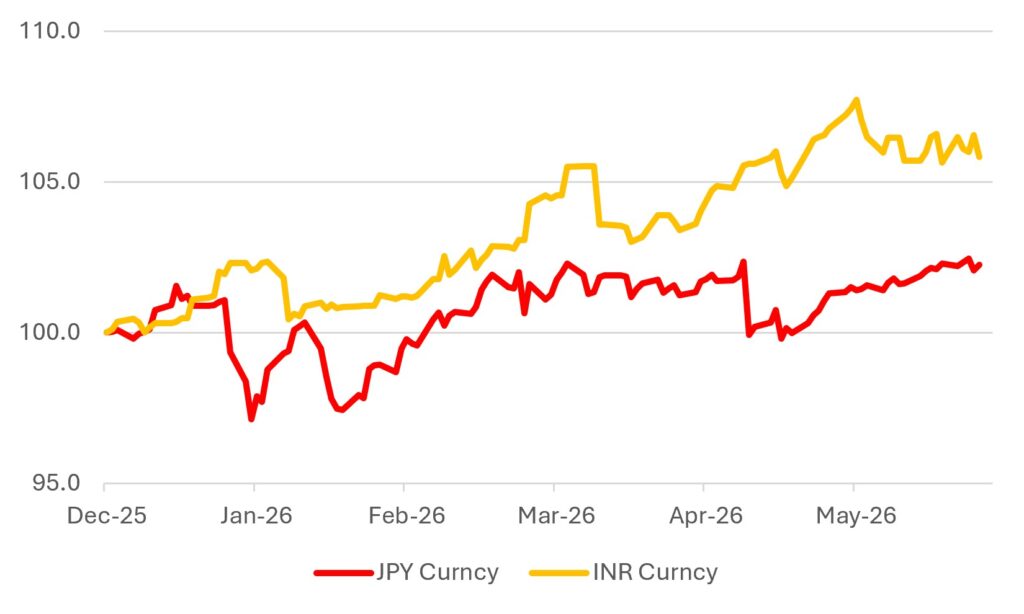

A resolution to the Middle East crisis carries meaningful currency implications, though the effects will not be uniform. The dollar is likely to soften against currencies that bore the greatest burden during the crisis, most notably the Japanese yen and the Indian rupee.

The yen has long served as a crisis hedge and safe-haven destination. As the geopolitical and energy-related risk premium unwinds, some of the dollar strength that accumulated during peak uncertainty should reverse. The Bank of Japan’s cautious policy normalisation provides a complementary tailwind: a less alarming global backdrop makes further yen appreciation more, not less, likely.

The rupee’s case is more direct. Elevated energy costs squeezed India’s current account; a sustained fall in oil prices would meaningfully ease that pressure. Combined with the improved investor sentiment described above, the rupee could be among the clearest beneficiaries within the emerging markets currency complex. For dollar-based investors, this adds a currency return to what is already a compelling equity catch-up trade.

Chart 3: JPY and INR versus the USD pressured

Rebased to Dec 31st 2025=100

Source: Bloomberg

The dollar, though, is unlikely to weaken universally. Against commodity-linked currencies such as the Canadian dollar or Norwegian krone, where the energy relationship runs in reverse, the picture is not very clear. The more interesting trade is selective: long yen and rupee versus the dollar, reflecting the unwinding of the most acute crisis distortions.

Gulf markets should rebound, although major indices in the region did not fall dramatically during the crisis. Dubai and Abu Dhabi are only modestly lower for the year, while Saudi Arabia has been comparatively resilient. Index performance, however, conceals significant dispersion among individual companies.

Several property, aviation, tourism, and consumer businesses still reflect assumptions that travel and capital flows will remain impaired, that expatriates will be slow to return, or that fiscal pressures would take long to ease. A deal would challenge those assumptions. The most attractive opportunities may therefore be found below the index level – in companies whose prices still imply a much longer period of regional disruption.

The oil market is where the transition from relief to reality becomes most complicated. At the height of the crisis, a substantial share of Gulf production was stranded or rerouted through alternative channels, and export losses varied. Reopening the Strait would release stranded Gulf production, while sanctions relief could allow Iran to rebuild exports from depressed levels.

The physical recovery will not be instantaneous. Ports, pipelines, export terminals, and tankers must be inspected and restarted. Insurers will need to regain confidence, shipping schedules must be rebuilt, and refineries will have to adjust their crude purchasing programmes. Even after a political agreement, logistics will remain a constraint.

Nevertheless, the direction of travel is powerful. Gulf producers have a strong financial incentive to restore exports quickly after losing revenue. Iran would add a second supply effect by competing more openly for market share. A poorly coordinated recovery could eventually produce a substantial surplus, especially with non-OPEC production still growing.

Oil may therefore experience two phases: an initial fall as the extreme geopolitical overhang is removed, followed by a second adjustment as physical exports recover. OPEC and its partners would then have their work cut out as they persuade cash-hungry producers to exercise restraint. History suggests that discipline is easiest to proclaim when nobody urgently needs the money.

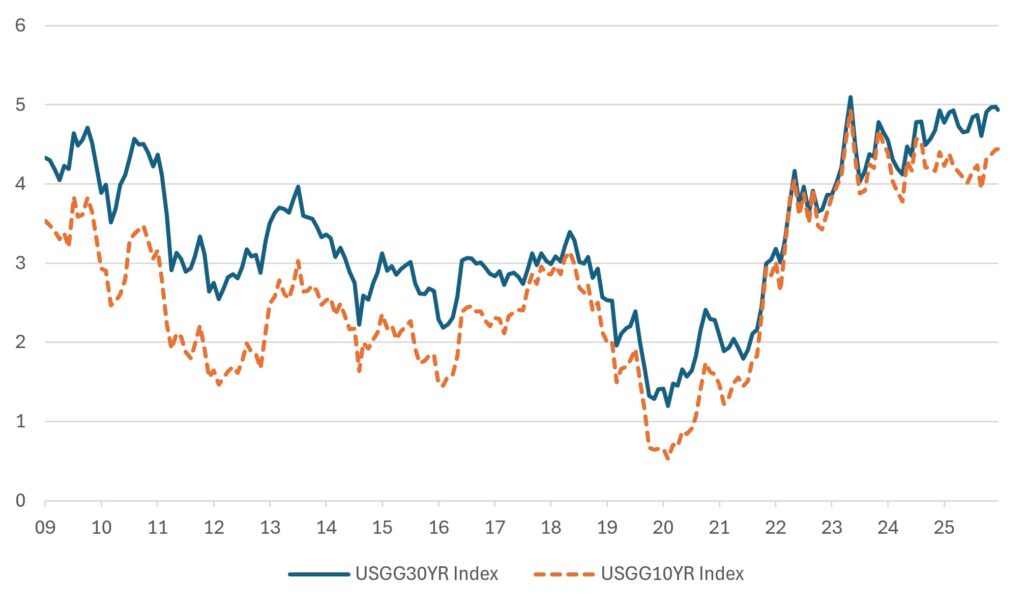

Government bond yields should initially decline as the risk of a prolonged energy shock recedes. A fall of perhaps 10-15 basis points in the US ten-year Treasury yield would be a reasonable first response. We would be cautious about extrapolating that move.

Chart 4: US 10 and 30-year bond yields remain close to recent Highs

Source: Bloomberg

The inflationary pulse already created by energy, freight, and supply-chain disruption will not disappear simply because an agreement is signed. Businesses reduce prices more slowly than they raise them, while depleted inventories and disrupted logistics take time to rebuild.

There is also a counterintuitive risk. Resolution of the crisis could release pent-up household and corporate spending. Consumers may respond as they did after the pandemic: relieved that the danger has passed, they travel, spend, and celebrate. Economists call it pent-up demand; ordinary people call it going to the party. That burst of activity could improve growth while – hold your breath – prolonging inflation.

The Federal Reserve meets on 16-17 June, offering the first major opportunity for a central bank to reassess risks against the changing global dynamics. The Fed and ECB may breathe a sigh of relief that their worst nightmares are unlikely to materialise, but both will remain on inflation watch. The immediate case for further tightening may weaken; the medium-term case for caution does not.

Our central expectation is for broader market leadership rather than another indiscriminate rise in global equities. The first beneficiaries could include consumer discretionary, travel-related companies, real estate, selected European domestic sectors, India, and individual Gulf companies still priced for prolonged disruption.

Energy and materials are likely to surrender some of their geopolitical premium. Technology may experience profit-taking and relative underperformance as investors recycle gains into cheaper cyclical assets. None of that weakens the structural technology story; it simply recognises that even excellent companies can become over-owned when investors have too few alternatives.

A scenario of selective dollar weakness may benefit the yen and rupee: long yen and rupee positions offer both a macro logic and a valuation argument that does not depend on the most optimistic deal scenarios playing out.

Gold deserves a separate word. The instinctive reaction may be that a peace agreement removes the case for holding it. That conclusion may be premature. Central banks, particularly in emerging markets and across the Gulf, have been accumulating gold not primarily as a crisis hedge but as a structural response to dollar dependency and the demonstrated willingness of Washington to weaponise financial sanctions. A single agreement, however significant, does not undermine that motivation. In fact, if anything, the Middle East episode has reinforced it.

There is also a wider policy uncertainty that gold reflects and that a Gulf deal does not resolve. The same administration that deployed economic coercion in the Middle East remains in office, with an appetite for using tariffs, sanctions, and financial pressure as instruments of bargain. Markets may celebrate the immediate resolution while quietly acknowledging that the next confrontation, wherever it materialises, is a question of when, not whether. Gold is the asset that prices that question. Central bank demand is unlikely to fade; if anything, the lesson of the past year accelerates the case for diversification away from dollar-denominated reserves.

A peace agreement would be welcome for reasons extending far beyond markets. Investors should not, however, confuse the removal of what could have been a significant disaster with the arrival of a perfect economic environment. Lower oil prices would be disinflationary, while renewed spending and stronger growth would be inflationary. The first trade is comparatively obvious. The more important question is what happens after the relief party and who is still holding gold when the next bill arrives.

Table 1: Selected Year-to-Date Performance

| Sector/Market | YTD Performance |

| Global energy | +27.0% |

| Global information technology | +19.0% |

| Global materials | +12.7% |

| Global equities | ~+5.0% |

| Global consumer discretionary | -3.7% |

| India | -11.3% |

| Dubai | -1.5% |

| Abu Dhabi | -1.9% |

Note: Market performance is based on Falco’s dataset and is rounded. Information and diplomatic developments are current at the time of writing (14 June 2026).

Source: Bloomberg, MSCI

Gary Dugan – Investment Committee Member

Bill O’Neill – Non-Executive Director & Investor Committee Chairman

15th June 2026

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell a security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person’s sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth is Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB