Click Here to Read the Full Version

Last week, the geopolitical spotlight shifted decisively towards Asia, where President Trump’s political travails have proved to be challenging. Tariffs and counter tariffs notwithstanding, momentum has now arguably tilted eastward, with China now standing toe-to-toe with the United States in economic and strategic heft, while Japan, under its new prime minister, projects a self-assurance unseen in decades.

In her early dealings with Washington, Sanae Takaichi has struck a tone of quiet resolve – cooperative yet unapologetically independent, signalling that Japan is no longer ready to play the second fiddle. The 15% surge in Tokyo’s equity market over the past month reflects both a domestic revival of confidence and an emerging conviction overseas that Asia’s major economies are now engaging America on their own terms. For investors, the message is that capital must now think and act in terms of multipolar resilience, not US exceptionalism. Asia’s markets are no longer the satellites, they are the new poles of confidence.

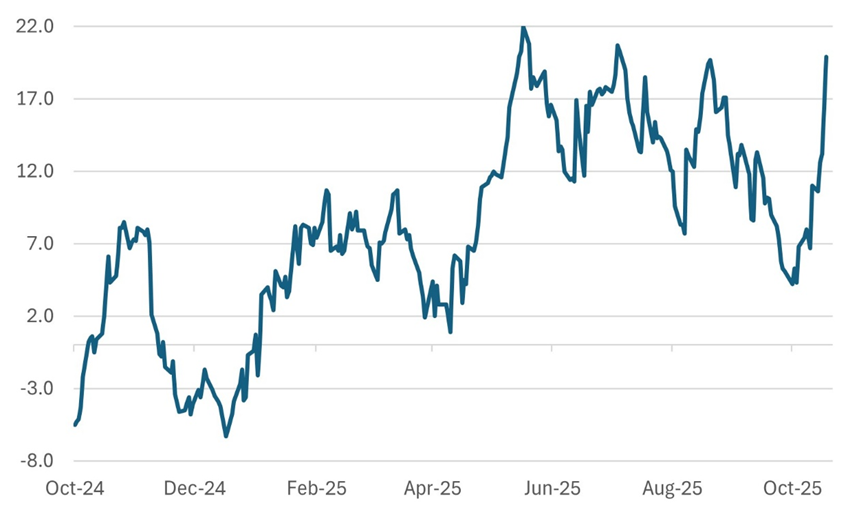

There is a shift underway. We are witnessing greater upside to global growth, despite inflation continuing to surprise somewhat negatively and the likelihood of a pause on rate cuts. If we had to guess, we would expect more inflation. The most recent data points for global economic growth have been positive. The Global Economic Surprise Index has increased dramatically in recent weeks, almost rising vertically since the middle of October.

Chart 1: Near Vertical Rise in the Global Economic Surprise Index

Index

Source: Bloomberg

Global inflation may not show signs of a marked acceleration because, in any case, it has mostly been a problem for the US rather than the rest of the world, but it has nevertheless become entrenched at higher levels. While investors may have been initially excited that the latest US inflation data was a tenth below expectations, it is still stuck at around 3.0% and not in the 2.0%-2.5% range that we believe the Fed would be more comfortable with.

The Fed surprised the market with its hawkishness, and has had to reassess the odds of a rate cut when it meets next in late December. In a week, the odds of a 25-bp rate cut have decreased to 68% from 98%The US yield curve has largely seen a parallel shift higher over the past month.

Chart 2: Parallel Shift in US Yield Curve (%)

Source: Bloomberg

China and the US: The Optics of Power

The Busan summit between Xi Jinping and Donald Trump was more about posturing than policy. Both leaders arrived at the summit with their own domestic compulsions, yet it was Xi who appeared to dictate the rhythm. His call for “mutual respect” was not merely a diplomatic courtesy, but a signal that Beijing now views itself as a peer power. The image of Trump travelling to Asia to meet Xi captured the shift: the geopolitical centre of gravity is no longer anchored in Washington.

China approached the meeting from a position of quiet strength. Rare-earths and battery materials provide China with a significant strategic leverage that the US cannot easily replicate. For the next several years, Beijing effectively controls the upstream machinery of the global energy transition. The US remains dominant in software and semiconductors, but interdependence has become mutual. As American economist Stephen Roach aptly notes, the two nations are locked in a “codependent” relationship, one that becomes unstable whenever either side tries to rewrite the rules. This summit was a brief attempt to steady that imbalance.

Beijing appears to have the upper hand at the moment. Trump sought a political win by pausing tariff escalation; Xi sought time to innovate and consolidate. Both achieved something, but China gained more of what it values most: time. Export restrictions on Nvidia’s advanced AI chips have not stopped progress; they have triggered a state-backed innovation drive reminiscent of Japan’s post-war industrial strategy. Authorities in Beijing appear convinced that indigenous technology is, in their words, “a matter of life and death.” That determination which Roach also heard in recent conversations with Chinese officials explains why consumption remains secondary to technological self-sufficiency in China’s next Five-Year Plan.

Markets have read the truce as temporary relief rather than resolution. Nevertheless, Asian equities rallied on what they perceived as reduced tail risk, but the deeper decoupling continues. Supply chains are being rebuilt around control rather than cost efficiency; volatility will remain embedded. The key investment implication is clear: the intersection of state strategy and private ingenuity is where the next decade’s alpha will emerge.

The broader symbolism endures. Xi left Busan with the optics of equality or perhaps quiet superiority in a relationship once defined by American dominance. If this was, as Roach observed, “a deal between equals,” the more profound truth may be that equality itself marks China’s greatest victory.

Japan’s Remarkable Comeback

The Japanese equity markets near 15% return in October has certainly put Asian equity markets back on the map. The Japanese economy is consistently showing inflation, some growth, and confidence and resilience unseen in recent decades. As we remarked in last week’s GCIO Weekly, Sanae Takaichi’s leadership marks the beginning of a new era — the symbolism of Japan’s first female leader is not lost on the markets. In Asia, it is not only China that can lay claim to global stature; Japan is quietly reasserting itself as an economic and diplomatic equal on the world stage.

Chart 3: Japan’s Remarkable Equity Market Performance in October

Source: Bloomberg

From Busan to Tokyo, the message from Asia was consistent: parity, not deference. Donald Trump’s meeting with the Japanese PM marked a pragmatic reset in US–Japan relations, built on trade, investment, and security cooperation. Washington agreed to scale back its threatened tariffs on Japanese goods to 15% from 25%, in exchange for a Japanese commitment to channel roughly US $550 billion into US industry through loans, equity stakes, and joint projects. Tokyo also pledged to open its market further to American agricultural and defence exports. For both leaders, the deal represents a political victory: Trump can portray it as evidence of “fair trade,” while Takaichi deserves credit for avoiding a damaging tariff war and strengthening Japan’s status as Washington’s most dependable ally in Asia.

Beyond trade, the summit’s most strategic outcome was a new framework for cooperation between Japan and the US on critical minerals and rare earths — a clear bid to reduce reliance on China’s near-monopoly in these supply chains. The accord commits the two powers to joint stockpiling, financing of new extraction projects, and collaboration on next-generation nuclear technology, including small modular reactors. In doing so, it aligns Japan’s re-industrialisation agenda with America’s wider effort to “friend-shore” key resources among trusted partners.

For markets, the tone was one of quiet bullishness. Japanese exporters — notably automakers, machinery producers, and defence manufacturers — benefited immediately from the removal of tariff risk. The deal also supports longer-term investment narratives: a rise in defence spending towards 2% of GDP, a renaissance in nuclear and energy-security infrastructure, and a broad re-rating of industrial and technology stocks linked to resilient supply chains. The yen firmed modestly as trade uncertainty receded, while Japanese government bond yields eased, reflecting relief that the Bank of Japan faced no new pressure from Washington to tighten policy.

Strategically, the Tokyo meeting re-establishes Japan as the cornerstone of America’s Asian alliance network and, in parallel, heightens the region’s competitive edge against China. For investors, one geopolitical tail-risk has diminished — a US–Japan trade rupture — but another lingers: the gradual bifurcation of the global economy into US- and China-aligned blocs. In summary, the summit has given markets a short-term boost and Japan a renewed sense of purpose. Yet the real measure of success will be whether the promised US $550 billion in investment and the rare-earth partnerships evolve into tangible action rather than merely remaining diplomatic theatre.

Gary Dugan – Investment Committee Member

Bill O’Neill – Non-Executive Director & Investor Committee Chairman

4th November 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person’s sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB