Click Here to Read the Full Version

Markets are no longer driven solely by size, but by how swiftly they strike a balance. Last week reinforced the narrative that leadership is broadening, not weakening, as capital rotates away from US concentration risk toward diversification by geography, sector, and currency. Persistent dollar weakness, combined with improving growth narratives across parts of Asia and emerging markets, is attracting incremental global capital flows. Investors appear increasingly willing to diversify both geographic and currency exposure, particularly as valuation and policy differentials widen. Nevertheless, positioning remains cautious rather than complacent. Recent profit-taking in gold should be seen less as an exit strategy and more as a portfolio maintenance requirement, with the underlying commitment to hedging geopolitical risk and currency uncertainty remaining firmly in place.

The week marked a notable shift in how investors are approaching technology: less breadth, more judgment. The market response to Claude-maker Anthropic’s latest model release has reinforced a shift already underway in technology investing. Broad “own the full AI stack” positioning is giving way to greater selectivity. Software, data and IT services stocks sold off sharply as investors reassessed pricing power and reinvestment needs. The concern is not demand destruction, it is margin pressure and rising capital intensity.

By contrast, the rebound in NVIDIA shares highlights where confidence remains strongest. The stock rose about 8% in a single session during the week and finished roughly 10% above recent lows. The move followed renewed emphasis from the company on the scale and durability of AI infrastructure spending already committed by hyperscalers and large enterprises. That distinction matters. Monetisation of the application layer is becoming more competitive. Investment at the infrastructure layer remains visible and substantial.

Chart 1: NVIDIA vs MSCI USA Software and Services Sector

Relative performance rebased to –1 Year =100

Source: Bloomberg

The implication, is it’s not the end of the tech cycle. Rather, a phase of higher dispersion and volatility where balance sheets matter more; pricing power matters more; capital discipline matters more. Exposure to technology is becoming more discerning, not more defensive.

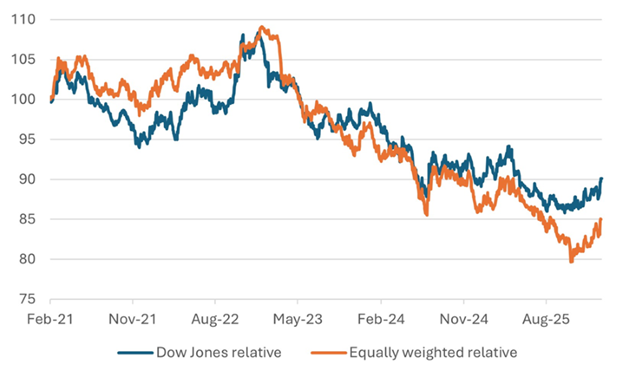

The recent rotation out of technology and into the broader market is not a warning sign; in fact, it is the mechanism by which this equity cycle extends. The tech-sector volatility that we witnessed last week merely accelerated a shift that has been building for months, now clearly visible in the sustained outperformance of the equally weighted S&P 500 relative to its market cap-weighted counterpart. As we noted earlier, markets are no longer driven solely by size. Market leadership is broadening away from a handful of mega-cap technology stocks toward cyclical and domestically oriented sectors, including industrials, financials, consumer discretionary ex-mega cap and selective value plays.

Crucially, all this is not sentiment-driven. Macro data are validating the move. History suggests that periods of extreme index concentration rarely end in immediate market declines; more often, they resolve through higher dispersion, where returns are earned through strategic allocation, balance-sheet strength, and pricing power rather than passive beta. The current rotation fits that template far more convincingly than any classic risk-off narrative.

Chart 2: Dow Jones and Equally Weighted Indices Recover Versus S&P 500

rebased to February 2021 =100

Source: Bloomberg

Recent data releases point to a meaningful revival in US consumer spending, underpinned by resilient labour income, easing inflation pressures and still-healthy household balance sheets. In that context, the case for broader equity exposure strengthens, as earnings momentum becomes less concentrated and more sensitive to domestic demand rather than global tech investment cycles. The equal-weight outperformance therefore reflects not just rotation, but growing confidence in the durability of US economic activity.

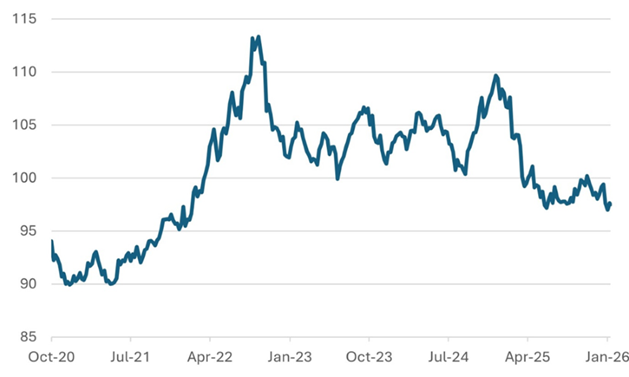

The rotation is equally evident in the sustained outperformance of other prominent markets, with Japan emerging as a clear beneficiary. Following this weekend’s decisive election victory for Prime Minister Sanae Takaichi and the ruling Liberal Democratic Party, the market appears positioned for further gains. The verdict delivered a governing supermajority, removing a meaningful layer of political uncertainty and strengthening the mandate for policy execution. Markets have welcomed the signal of continuity, particularly around structural reform and corporate governance. Japanese equities have responded accordingly, led by domestically oriented and cyclical sectors, as investors price in stable governance, targeted fiscal support and continued pressure on companies to improve returns on capital.

Japanese bond and currency markets, however, are telling a more sceptical story. Persistent pressure on the yen and long-dated government bonds reflects unease over fiscal discipline and debt sustainability. That divergence matters. Equity investors are voting on reform momentum and earnings leverage; bond markets are voting on balance-sheet credibility. For now, equities are winning the argument, but not with a blank cheque. Japanese risk assets remain supported, while currency exposure and duration risk demand active, rather than passive management.

Chart 3: MSCI Japan’s Outperformance Over the US

MSCI Japan relative to MSCI USA net TR $ (rebased to -5years =100)

Source: Bloomberg

Fixed Income, FX & Commodities

In fixed income markets, the US dollar experienced a four-year low before retracing on news flow regarding key policy nominations, underscoring how sensitive FX markets remain to monetary policy and Fed leadership expectations. Safe-haven assets such as precious metals experienced significant moves, with metals that had previously benefited from term premium shocks seeing notable loss reversals. This suggests a complex interplay between yield curve dynamics and risk sentiment.

Chart 4: US Spot Index Rebounds Modestly from a Four-year Low

Source: Bloomberg

Commodity markets were mixed. Energy prices were influenced by broader risk sentiment and demand expectations, while gold’s advance reinforced its safe-haven appeal amid thematic equity stress. Industrial metals and agricultural commodities were relatively steady with no new major drivers reported during the week.

Gold: An Insurance Policy You Can’t Give Up On?

The recent recovery in the gold price has been telling and somewhat predictable. Investor demand for the yellow metal continues to reflect a desire to hedge persistent geopolitical risks and renewed softness in the US dollar, rather than using the yellow metal as a simple inflation trade. Gold has regained significant ground after its recent pullback, supported by steady central bank buying and stabilising ETF flows. Recent profit-taking appears driven less by conviction and more by discomfort with volatility. History suggests that is rarely a reason to abandon insurance.

Silver, by contrast, has behaved far less predictably. While it shares some of gold’s macro drivers, higher volatility and greater industrial exposure have worked against the metal in recent weeks. Sharp price swings triggered higher margin requirements in futures markets, forcing some investors to reduce exposure and amplifying short-term pressure. The divergence reinforces a familiar pattern in periods of stress: gold functions as a balance-sheet hedge; silver behaves more like a hybrid risk asset. Treating the two as interchangeable is a mistake that markets repeatedly punish.

The broader message from precious metals is not panic, but persistence. Investors continue to pay – and position – for protection against geopolitical uncertainty, currency weakness, and policy error. Those trimming exposure on short-term price action may find they have saved on premiums just as the insurance becomes most valuable.

This week’s macro focus is on US inflation and employment data, which will influence expectations on the timing of any further policy easing. The market will scrutinise the delayed January non-farm payrolls data, due out this week, for any signs of cooling in labour demand and, crucially, any loss of wage momentum, after recent data pointed to resilience rather than overheating. Later this week, the January CPI release will show whether the disinflation trend is resuming following recent stickier data points, particularly in services. For markets, the balance matters more than any single number. Evidence of moderating inflation alongside still-healthy employment would reinforce the case for a soft-landing scenario and support risk assets. A renewed upside surprise on either front could push rate-cut expectations further out and keep volatility elevated across rates, FX, and equities.

The key takeaway is not a call for indiscriminate risk reduction, but an observation about how market participants are responding to current conditions. Broader equity exposure, selective positioning in technology, attention to currency dynamics, and the continued use of hedges reflect a market that appears to be rotating rather than experiencing structural stress.

Gary Dugan – Investment Committee Member

Bill O’Neill – Non-Executive Director & Investor Committee Chairman

9th February 2026

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person’s sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB