By Falco

02 Jun 2025

• S&P500 has its best May in 35 years

• But... US assets remain at risk from future high core inflation and a constrained central bank.

• ECB and Asian central banks are likely to cut rates to support their respective economies

• We see further outperformance of ex US markets

• AI - a driver of global growth

The S&P 500 recorded its best May in 35 years, surging 6.2% during the month and notching up its best monthly gain since November 2023. Not surprisingly, the financial press has been euphoric. Yet, beneath the surface of this equity euphoria, the broader economic outlook for the US remains anything but reassuring. It’s striking that in the same month that the equity markets staged a decent rally, the yield on the 10-year US Treasury bonds rose 24 basis points to 4.40%—a signal that fixed income investors are still wary.

US Inflation: Good News Likely Behind Us…Now the Reality

While some calm has returned to the tariff narrative (it could be temporary, so don’t hold your breath yet), and headline inflation has eased, investors would do well to brace for more difficult data ahead. Last week’s PCE inflation report may well have marked the peak of the good news—and the start of something more troubling. The PCE Price Index for April 2025 came in cooler than expected, with headline inflation rising 2.1% year over year—below the 2.2% market forecast—and core PCE inflation (excluding food and energy) softening to 2.5%, the lowest since March 2021. Lower oil prices have temporarily eased inflationary pressures, but that relief is unlikely to last.

As the latest tariffs begin to filter through, US inflation is expected to accelerate sharply. JP Morgan now projects US core inflation to reach an annualised 6.0% in upcoming releases. On the contrary, core inflation in the Eurozone is seen heading toward just 2.0%.

The Federal Reserve continues to signal that it has little appetite to start talking about rate cuts. The latest Fed minutes released last week highlight a growing unease within the central bank over the persistence of inflation, which remains stubbornly above target despite headline figures easing recently. Policymakers acknowledged that newly implemented tariffs could further fuel price pressures, complicating the path toward price stability. At the same time, there have been growing concerns about the US dollar’s role as a global safe haven, with some officials noting the potential long-term risks to the dollar’s status if investor confidence begins to erode. The Fed remains cautious, balancing the need to tame inflation without undermining a labour market that may already be showing signs of strain.

Europe is a Picture of Calm

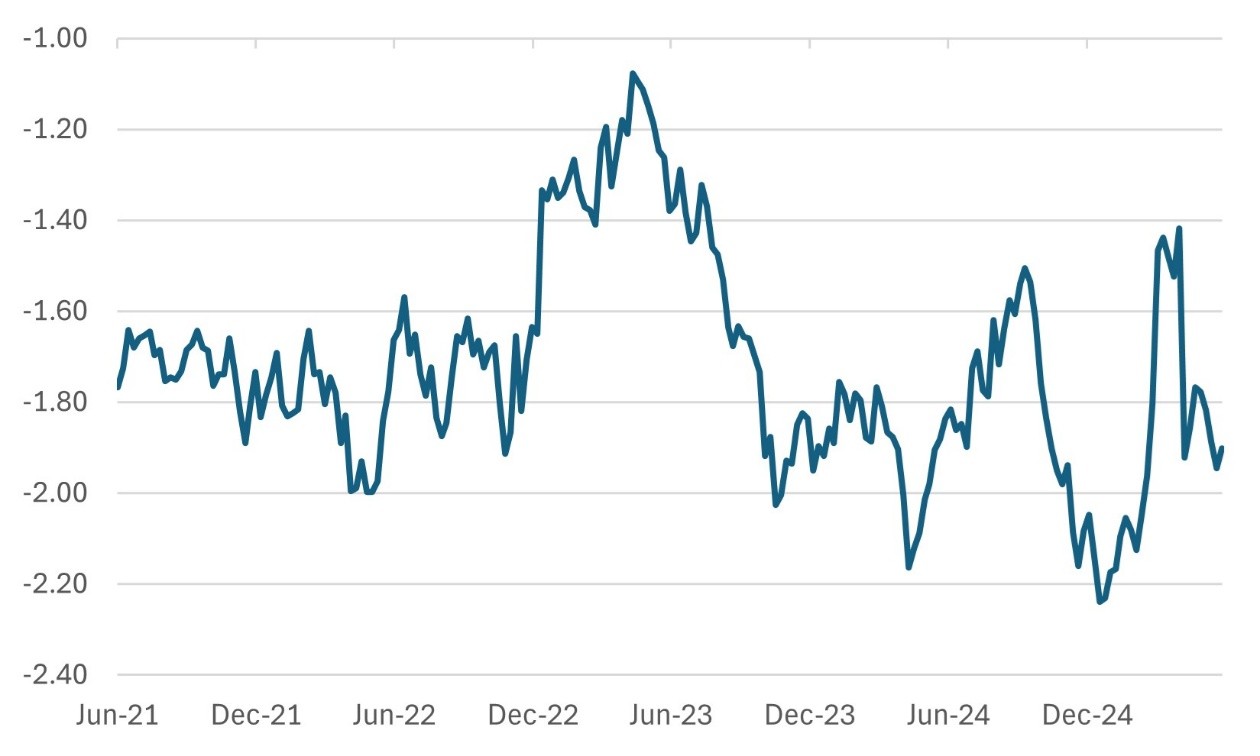

The ECB’s job is a great deal easier. We (and the market) expect a rate cut at the central bank’s next meeting, which should bring the policy rate down to 2.25%. Europe is also benefitting from lower long-term interest rates, with German 10-year bund rates trading close to two percentage points below their US equivalent.

Chart 1: Spread of 10-year German Bund and US 10-year Government Bond Yield (%) Source: Bloomberg

Source: Bloomberg

Asia to Continue to Ease Monetary Policy and Perform

Asia finds itself in a similar position as Europe with a comfortable opportunity to ease monetary policy in the coming months.

Let’s start with India. Although there is quite a debate in the market about whether the Indian central bank, the Reserve Bank of India (RBI), will cut rates this week, a rate cut looks the more likely outcome despite the better-than-expected first quarter GDP growth. The RBI, on its part, takes comfort from the fact that inflation has remained at a ‘reasonable’ 3%.

We suspect that the central bank will be keen to provide a further boost to consumer confidence ahead of a critical monsoon season. While industrial production data for April was marginally better than expected, it is still showing a marked slowdown. Quarter-on-quarter GDP growth has slowed to just 2.1% in April from 7% in January.

Other central banks in Asia that could be looking to cut rates:

• China (PBOC): Further cuts are expected (RRR, MLF rates) to combat weak demand and property sector stress.

• South Korea (BOK): High chance of a Q3/Q4 cut as inflation cools (2.7% in May) and growth slows.

• Thailand (BOT): Additional cuts possible after April’s surprise reduction, given sluggish growth (1.5% Q1 GDP).

• Indonesia (BI): Could cut in late 2025 if inflation remains tame and the Fed eases.

India, meanwhile, officially announced that it surged past Japan to become the world's fourth-largest economy on 25 May 2025. This declaration was made by B.V.R. Subrahmanyam, CEO of NITI Aayog, during a press briefing following the 10th Governing Council meeting of the policy think tank. India's nominal GDP has reached $4.19 trillion.

Non-US Assets May be the Answer

Given the current macroeconomic landscape—particularly the outlook for monetary policy—it still makes sense to maintain an overweight allocation to non-US assets within a global portfolio, across both bonds and equities.

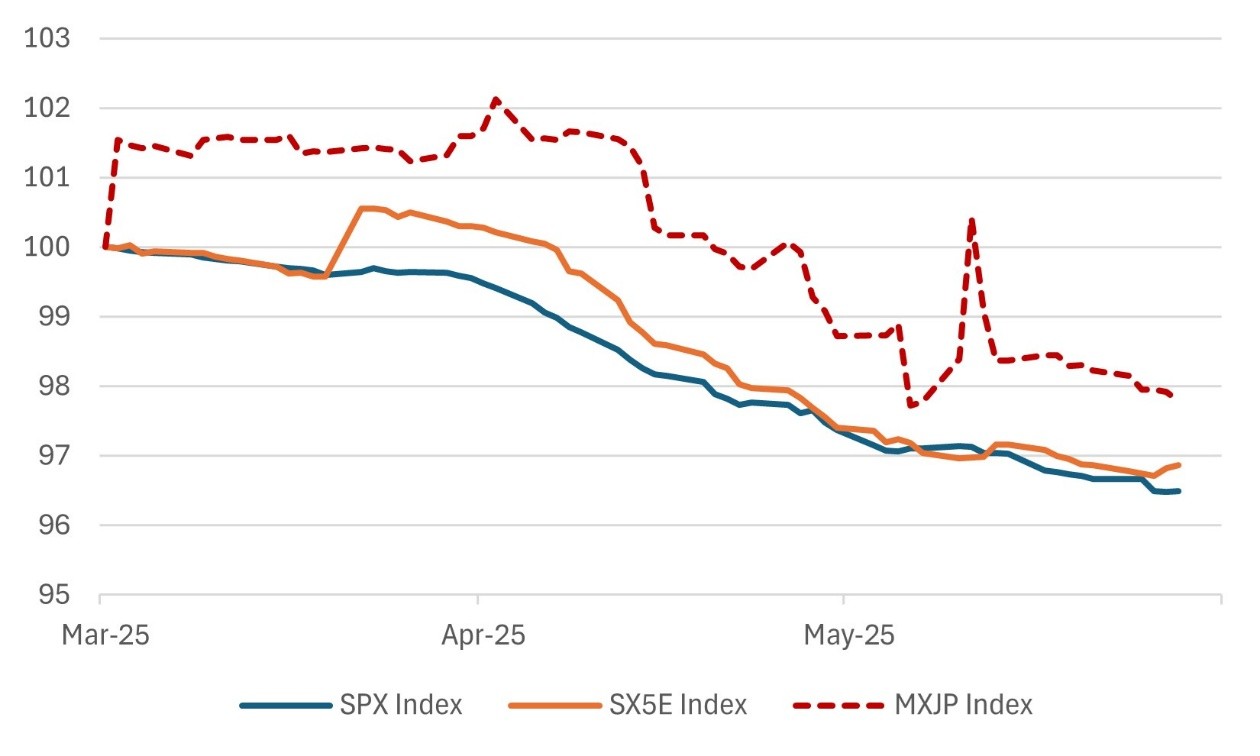

On a fundamental level, equity markets globally are grappling with downward revisions to earnings forecasts. The US, Japan, and the Eurozone have each seen comparable aggregate cuts. While we acknowledge that currency movements currently support US corporate earnings, we believe the dual headwinds of persistent tariffs and sticky high interest rates continue to pose meaningful challenges for the US equity market.

Chart 2: Consensus Earnings Forecasts are Falling for All Markets Source: Bloomberg

Source: Bloomberg

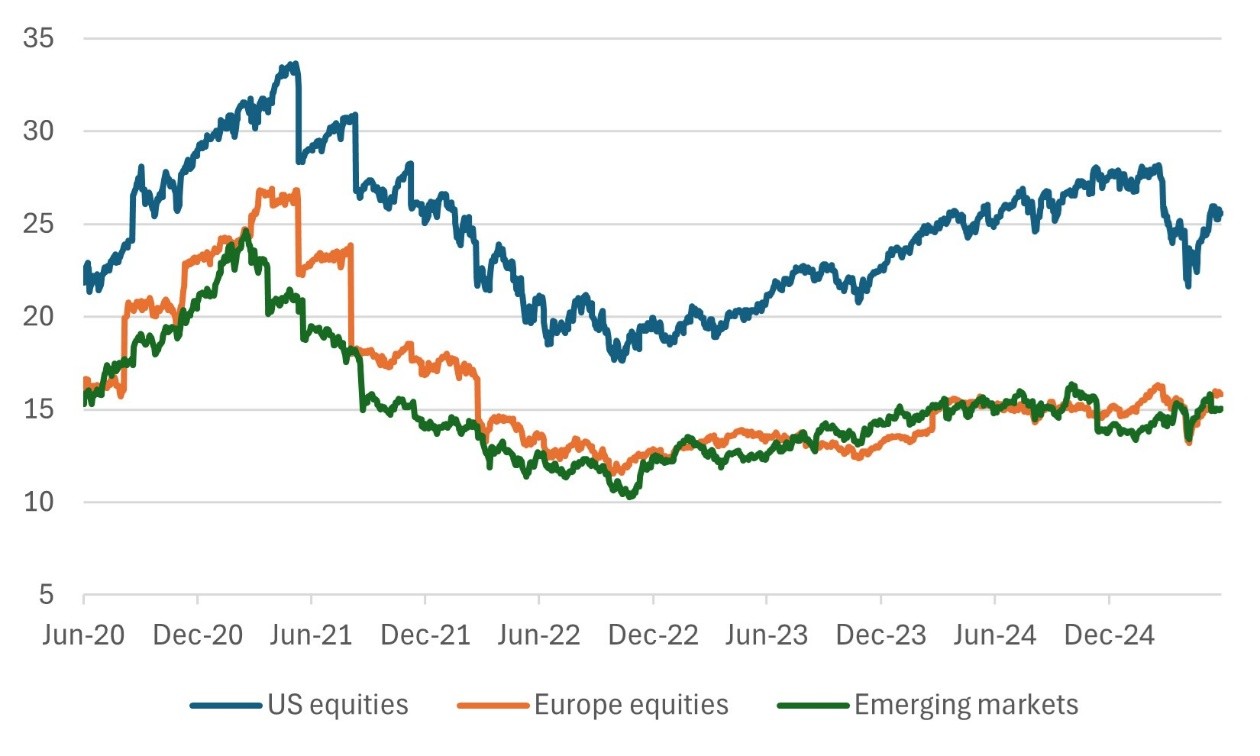

However, the most challenging issue for the US equity market is valuation. As Chart 3 shows, the US equity market is at a significant P/E premium to the rest of the world.

Chart 3: US P/E Multiple at a Still-high Premium to Europe and EM in Particular Source: Bloomberg

Source: Bloomberg

AI Driving Good Results from Nvidia and Global Economic Growth

Nvidia’s stronger-than-expected results last week—highlighted by a 69% year-over-year surge in revenue—reaffirm the scale of ongoing investment in artificial intelligence.

Beyond company performance, the broader macroeconomic implications of AI continue to attract attention. Recent research from PwC and the IMF highlights its transformative potential. PwC estimates that AI could boost global GDP by as much as 15% over the next decade, translating to roughly one additional percentage point of growth per year—on par with the economic gains of the Industrial Revolution. The IMF offers a more conservative view, projecting a 0.5% annual lift in global GDP between 2025 and 2030. While increased energy use—particularly from data centres—raises concerns about carbon emissions, both institutions suggest that the productivity and growth benefits of AI will outweigh the environmental cost.

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

2nd June 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB