By Falco

06 May 2025

• COVID provides a good template for discerning market reaction to trouble on the horizon

• A true market reaction will likely have to wait for hard economic data

• The fall in oil prices provides some good news

• The Fed is still some meetings from cutting rates

• We retain our preference for ex-US equity and bond markets

• Watch the US 10-year for inflation risk, and US HY for recession risk

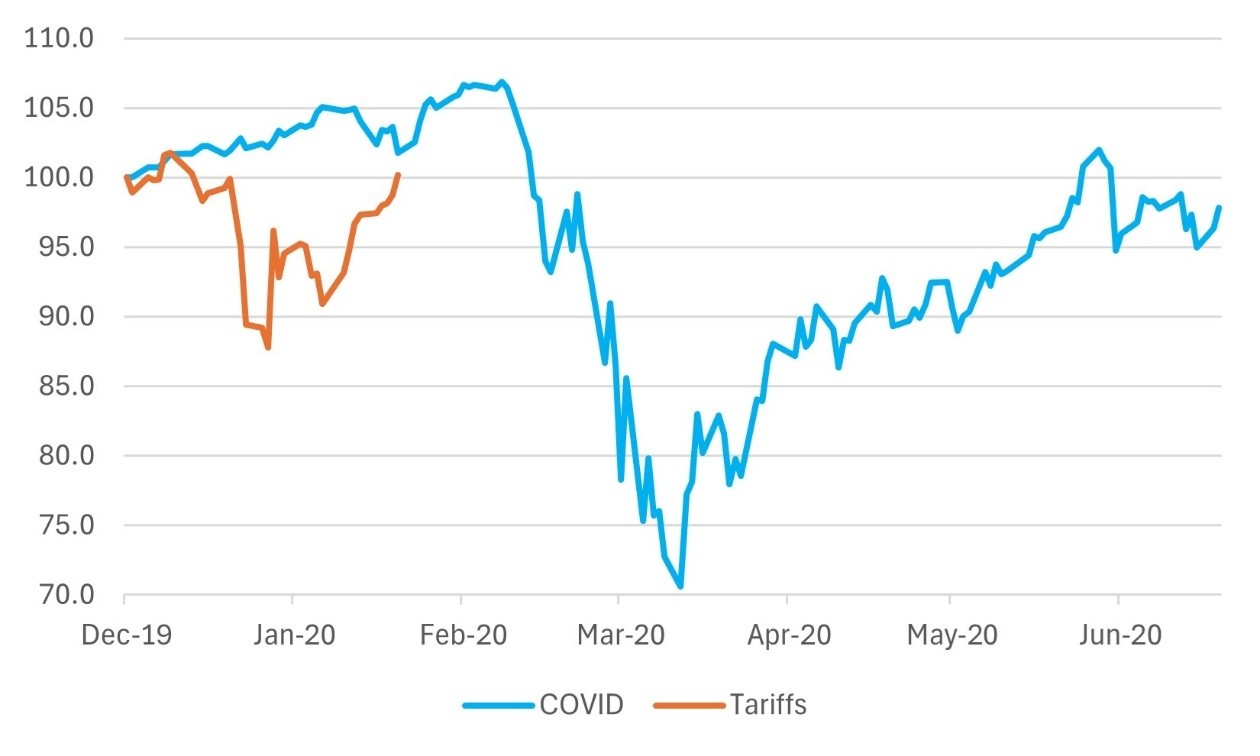

The equity market rally last week – despite little hard data on the impact of tariffs – is encouraging. However, in our view, it shows complacency since the market has chosen to overlook potential risks, focusing instead on solid growth and positive tech sector news. This reminds us of the overconfidence seen during the early days of the COVID crisis—when markets were quick to dismiss mounting uncertainties, only to face the harsh reality of a significant downturn later. Is history repeating itself?

To put things into perspective, we compared the performance of the S&P 500 from the moment we first heard about COVID on 9 December 2019. Despite the building uncertainty back then, the market continued to advance for almost three months until 20 February, before hard data began to reveal the true impact of the pandemic on the global economy. President Trump’s tariff announcement – seen in that context – could imply that markets may be facing turbulence in about six weeks from now.

Chart 1: Is the S&P 500 Showing the Same Complacency Seen During the Early Stages of 2019-20?

rebased to 100 Source: Bloomberg

Source: Bloomberg

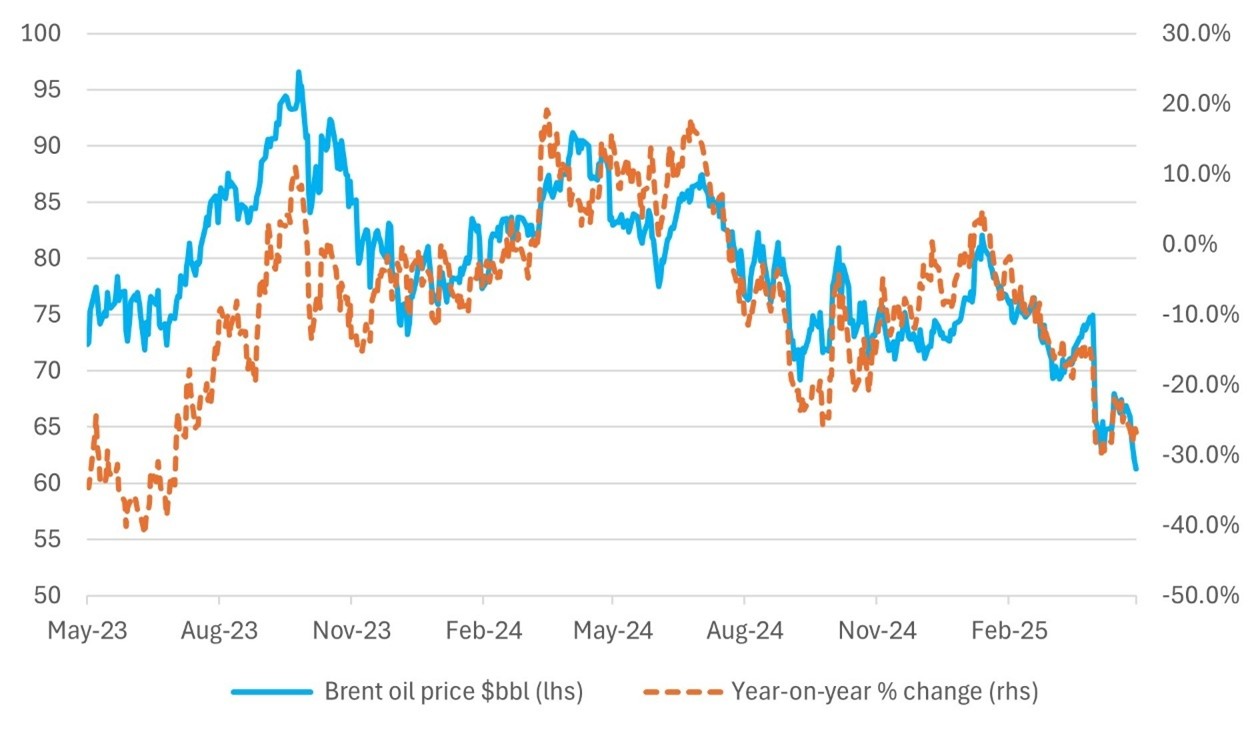

One positive dynamic in recent weeks has been the retreat in oil prices. Initially, this was attributed to concerns about global economic weakness, as the tariff threats continue to loom large. However, the retreat also reflects the market’s response to OPEC Plus’s decision to increase oil output despite the backdrop of weakening demand. OPEC Plus has made it clear that it is intent on unwinding the 2.2 million barrel per day (bpd) production cut implemented eighteen months ago. This unwind began in April, and from June, an additional 411,000 bpd will be added to the market. OPEC has scheduled a meeting for 1 June to determine whether to continue expanding production, potentially bringing output levels back to where they were a few years ago. Eight OPEC Plus members had agreed to the original 2.2 million bpd cut in November 2023.

Nevertheless, the decline in oil prices offers a timely boost to the global economy, acting as a valuable counterbalance to the anticipated sharp rise in prices from the tariff increases. JP Morgan estimates that if oil prices remain at current levels, it could reduce global inflation by approximately 1.5 percentage points. Some analysts also predict that Brent oil prices could drop as low as $50 per barrel, further contributing to the downward pressure on inflation.

Chart 2: Disinflation from the Fall in Oil Prices Source: Bloomberg

Source: Bloomberg

The calls from some quarters for the Fed to cut interest rates at this week’s meeting seem increasingly ill-timed, especially considering last week’s better-than-expected employment report and the current trend in oil prices. It’s always been difficult to understand how anyone expected a sharp decline in employment growth, even with the best efforts of Elon Musk and DOGE. The changes to tariffs, which were only proposed in early April, don't seem to have had enough time to significantly affect employment plans. Therefore, it’s hard to see why the Fed would be inclined to cut rates, especially when employment remains robust and falling oil prices could, to some extent, help mitigate the future impact of tariffs. Therefore, pre-emptive rate cuts still appear to be a few meetings away. Nevertheless, the market prices only a 30% chance of a Fed rate cut in June but fully prices a cut at the end of July.

There are, however, winds of trouble in the background of the US economy. Q1 US GDP growth was weaker than expected at a negative 0.7% quarter-on-quarter. In essence, GDP growth was weighed down by higher import volumes as companies pulled forward imports in an attempt to avoid at least some of the impact of the tariff increases by boosting near-term orders. The tariff increases could also significantly affect the vulnerable household sector, which has been battered by a loss of spending power. Below, we reproduce part of a Seeking Alpha article authored by Lance Roberts to add a bit more context. The highlighted data points are as follows:

We continue to believe MSCI World ex-US has significant potential to outperform the US for the remainder of the year. In Europe, the ECB is likely to cut rates in June, with an additional cut later in the year, taking policy rates down to just 1.5%. Even without the cushion of lower oil prices, inflation is unlikely to pose a challenge to the ECB's accommodative stance.

Chart 3: Relative Performance of the US Equity Market to MSCI World ex US (USD, net TR)

Rebased to May 2024=100 Source: Bloomberg

Source: Bloomberg

Anecdotally, we’re hearing that institutional managers are creating bespoke benchmarks to reduce their US exposure and increase long-term allocations to emerging markets and developed ex-US regions. The narrative that China is un-investable seems to be losing steam.

Asian equity markets have shown mixed performance year-to-date, but there’s a clear tilt toward stability. The weaker dollar is allowing Asian countries to ease monetary policy. In China, deflation is a bigger concern than inflation, which could help authorities launch more aggressive stimulus when needed. Meanwhile, the Bank of Japan is slowing the pace of its monetary tightening, even as age-related growth accelerates.

We remain bullish on European equities, where governments are already committed to fiscal easing, and the ECB is likely to cut rates sooner than the Fed. The market is pricing in a 1.5% ECB rate by the fourth quarter.

In the bond market, we’re keeping a close eye on the US 10-year yield as a gauge of inflation risk, and the US high-yield spread as a measure of recession risk. Last week, the 10-year yield rose by 10 basis points, signalling more inflation risk, while the high-yield spread narrowed, suggesting reduced recession risk. That said, macro factors still point to potential recession risk in the US, though bond experts argue that a substantial widening of the high-yield spread is required for confirmation.

Chart 4: US 10-year Yield Spikes Modestly but High Yield Spreads Remain Well Behaved Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

6th May 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB