By Falco

07 Jul 2025

After the last few weeks of euphoria, which saw asset markets notching up handsome gains, investors were faced with a bit of a wake-up call last week. A stronger-than-expected labour market report, in particular, dampened hopes of an early Fed rate cut. A Big, Beautiful Fiscal package only complicates the future.

The US jobs report for June surprised markets and forced markets to readjust expectations for future interest rates.

The US economy added 147,000 new jobs last month—significantly more than the 110,000 expected. At the same time, the unemployment rate fell to 4.1%, while most economists were expecting it to rise to 4.3%. The markets now see almost no chance of a Fed rate cut in July and a lower chance of one—if at all—in September.

Beneath the strong headline employment numbers, the report revealed structural softness, however. Nearly half of the job gains were attributed to the public sector, particularly education and state-level hiring. Job creation in the private sector was subdued at 74,000. Compounding this was a drop in the labour force participation rate, including a notable fall witnessed in the participation of foreign-born workers. This marks the continuation of a trend that has seen tightening labour supply, even as wage growth slows. The labour market is, maybe, ICEing over!

A Big Beautiful Bill: challenge to the Labour Market; Negligible Impact on the next 12 months’ Growth

At first glance, Trump’s Big Beautiful Bill might look like providing a boost to the US economy, but we worry that it will hurt the long-term potential growth, with limited near-term impact on growth. We believe it will only add to the country’s indebtedness.

A large part of the bill focuses on tougher border controls and cuts to immigration. For example, funding for immigration enforcement has jumped significantly, with $46.4 billion going toward the US-Mexico border. This is expected to slow the number of migrants entering the country. Some estimates suggest that the current trend is that of net migration away from the US!

Why does this matter? The US already faces an ageing population and a shrinking workforce. If fewer people are coming into the US to work, it could lead to labour shortages. That would push wages higher and make it harder for the Fed to bring down inflation. So, while the June jobs report was strong, these immigration changes could make it harder to grow the economy in the long run and could even create a mix of weak growth and stubborn inflation.

The more immediate impact of the bill is not universally seen as a material positive for the economy. Indeed, there are many headwinds on the horizon that may offset the extra spending. JPMorgan estimates that the bill in isolation adds about 0.4% to the primary deficit in fiscal year 2025 and 0.8% next year. However, once we combine tariff revenue, the total fiscal thrust is negligible.

Bonds and selective equities see downside

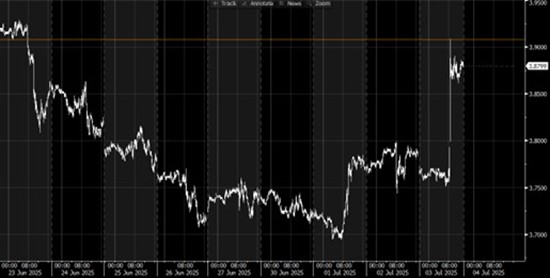

Market reaction to the US labour data was swift. Bond markets sold off sharply, with two-year yields surging 12 basis points (Chart 1). Gains in the equity market were more nuanced: interest rate-sensitive sectors such as real estate and utilities declined, while broader indices held firm on the back of perceived economic resilience.

Chart 1: US 2-year Yield Reverses Course Days After Discounting Early Fed Easing

Source: Bloomberg

The mood in the global markets has changed. The upswing in equities post the April lows was driven by expectations of early rate cuts in the US. Then came the US labour market report that threw those calculations somewhat off gear. Looking retrospectively, it is evident that the euphoria was a bit contrived. Market analysts were hailing the 25% rise in US equities from the April lows as a remarkable feat. In reality, however, the advance was just an “ordinary” 5% versus the start of the year. We now hear more about the increasing sense that the US equity market has run too fast, given that we are likely moving into a phase when US growth will wane, and inflation rises.

Second half slowdown… slowly becoming apparent

Turning to global economic dynamics, we see a synchronised yet uneven deceleration in growth unfolding. Forecasts peg global GDP growth in the second half of 2025 at a subpar 1.4% annualised rate. US growth is projected at 0.8%, Western Europe at 0.7%, China at 2.8%, and other EMs around 1.9%. This coordinated slowdown is attributed to waning business sentiment, trade tensions, and fiscal restraint.

Interestingly, the anticipated drag from earlier front-loading of goods imports—ahead of the July tariff deadline—has not fully materialised. June's all-industry global PMI rose by 0.5 points, indicating ongoing strength, especially in manufacturing and tech. Resilient industrial production in May and solid Asian exports support this view. The resilience appears driven by ongoing activity ahead of expected tariff escalations, and possibly stronger-than-expected tech demand.

We retain our positive view of Europe, although we’d prefer to buy into any absolute price weakness.

Europe is quietly navigating this slowdown with relative poise. Germany’s decision to relax debt-brake rules has allowed for increased infrastructure and defence spending. Industry surveys across the Eurozone support a view of stabilisation rather than deterioration. The region is benefiting from fiscal tailwinds and a measured monetary stance, contrasting sharply with US uncertainty.

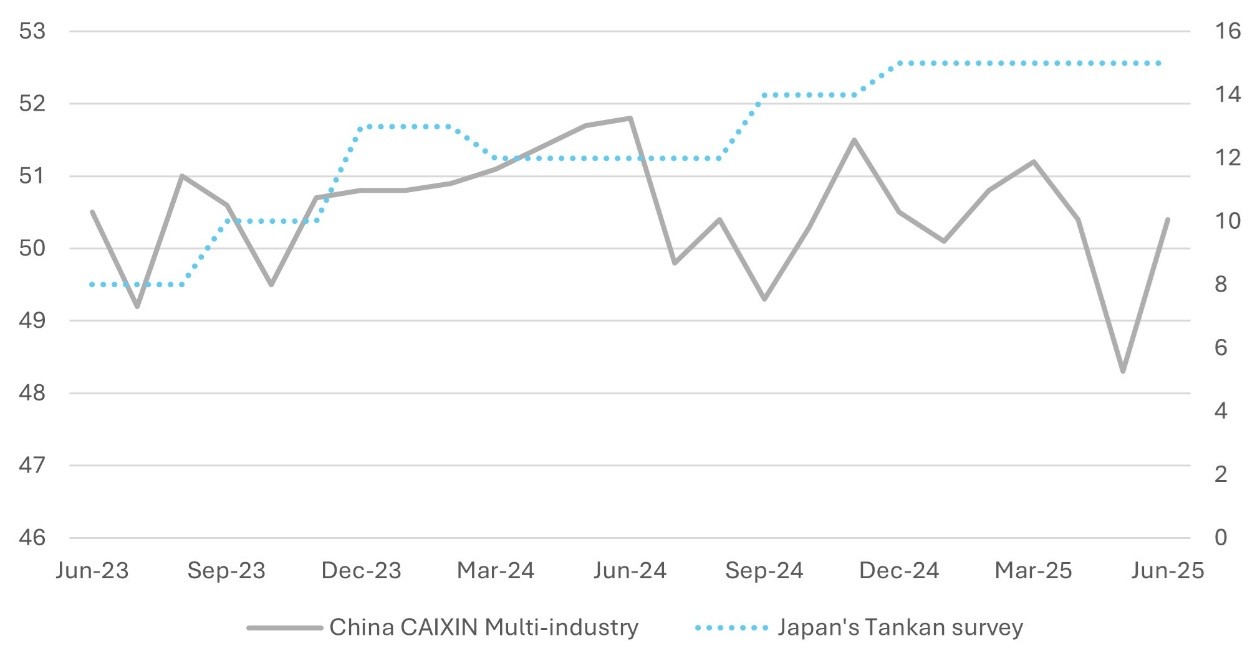

In Asia, the tone is also resilient. China's exports have outperformed expectations, despite a sharp decline in the US exports, which have been offset by gains from other markets, helped by strong tech demand and limited payback from earlier surges. The Caixin China General Manufacturing PMI jumped 2.1 points in June, fully offsetting May’s decline. The Bank of Japan, meanwhile, is seeing data that challenges its previous caution. The June Tankan survey showed no negative sentiment from tariff threats. With inflation pressures persisting and growth robust, the BoJ may be poised to upgrade its outlook and prepare for a potential October rate hike.

Chart 2: Improved Caixin and Tankan Surveys of Chinese and Japanese Industrial Confidence  Source: Bloomberg

Source: Bloomberg

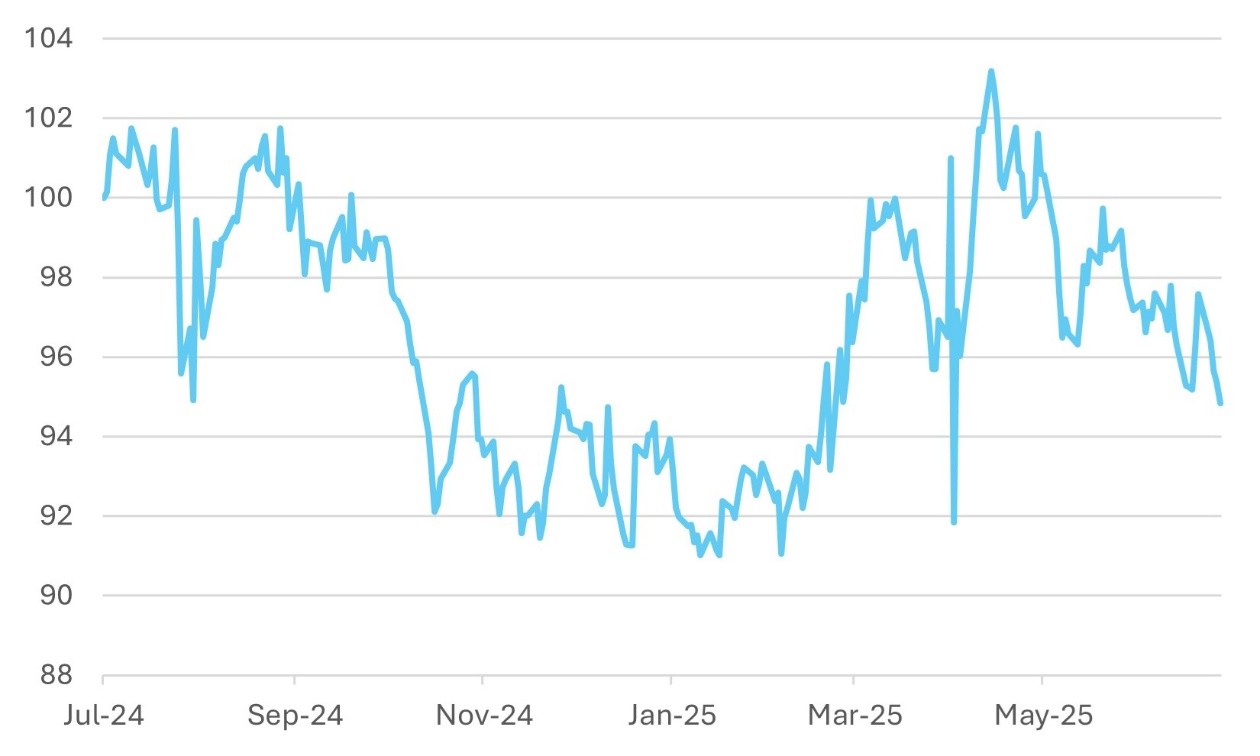

Meanwhile, Japan emerged as a standout in terms of equity opportunity, structural reforms, and investor inflows, underscoring the evident resilience of both Europe and Asia relative to the policy and fiscal noise in the US.

Japanese equities have gained renewed attention in global asset allocation circles. Several pivotal developments underscore this shift. In just a few months of FY2025, Japanese companies have announced more than ¥6.9 trillion ($47.75 billion) in share buybacks, with April alone seeing buybacks worth ¥3.8 trillion. At this pace, total annual buybacks could reach a record ¥22 trillion. Surging M&A activity has accompanied this extraordinary capital return. Year-to-date, domestic and cross-border dealmaking in Japan has reached $232 billion, reflecting a structural shift toward shareholder-aligned strategies and the shedding of non-core assets.

Equally significant is the resurgent foreign investor portfolio interest. Net foreign equity inflows during Q2 2025 alone exceeded ¥6.8 trillion, marking the strongest quarterly inflow in more than two years. What makes this more compelling is the alignment of this capital flow with corporate earnings momentum. Profit forecasts for FY2025 have been steadily upgraded. Net income for Topix-listed companies is now projected to rise by 11% year-on-year to approximately ¥46 trillion. This confluence of capital return, earnings growth, and reform places Japan at the centre of a new strategic allocation narrative.

As a slight caveat, ongoing tariff negotiations with the US could still cause some trouble for the Japanese market, but any further marked weakness would provide an opportunity to accumulate.

Chart 3: Relative Performance of Japanese Equities Offers Opportunity Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

7th July 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB