By Falco

19 May 2025

• The US and China agree to come back from the brink, but nothing is for certain

• In some quarters, the US 10-year is thought to offer tremendous value, but others would disagree

• The dollar continues to struggle to rebound

• US equities rally back to where they started the year, but corporate profit forecasts are under downward pressure

• US healthcare appears to have over-discounted the bad news

With a lot of reading behind us and post-participation in several forums over recent weeks, what stands out is the sheer diversity of views in the market today. While we have our own views, which we are quite steadfast about, we always want to understand the other side of the argument. What’s been striking lately is the passion with which those varying arguments are made. Some investors are convinced that we are staring at a once-in-a-cycle buying opportunity in the US Treasury market; others are lifting their S&P 500 targets, encouraged by the strong rebound post-April lows. Meanwhile, economists remain split in their views—some warning of persistent inflation risks, others pointing to enough disinflation to give the Fed room to cut rates.

Whichever side of the fence you’re on — bullish or bearish, it’s hard to avoid the fact that we’re still on a sticky wicket. It’s been just over six weeks since the “tariff shock” overwhelmed global markets. While there’s talk of a more moderate tariff regime in the works, it’s too early to assess the longer-term impact of what could be a profound shift in global trade and economic policy. In the meantime, we’re seeing a familiar cycle of sentiment that has guided the markets for some time now: markets rise, optimism follows; they fall, and gloom takes over. Right now, sentiment seems driven more by price action than hard data.

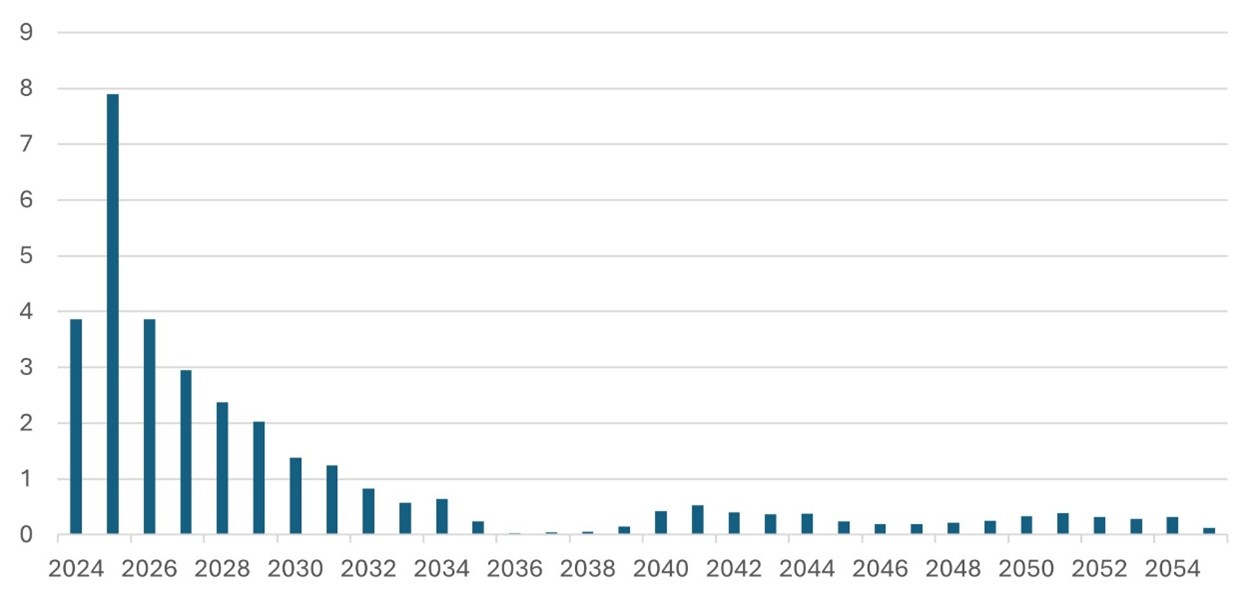

Let’s refocus on the US Treasury market, where the 10-year yield has traded in a volatile 4.2%–4.5% range. Yields spiked more than 100bps post the April tariff announcement, highlighting how vulnerable bonds are to policy surprises. But beyond short-term noise, what is even more concerning is the medium-term backdrop, which remains troubling. A towering wall of issuances looms—Treasury refinancing needs in 2025 will be more than double those of 2024 (Chart 1).

Chart 1: US Government Debt Instruments Maturing by Value ($ trillion) Source: Bloomberg

Source: Bloomberg

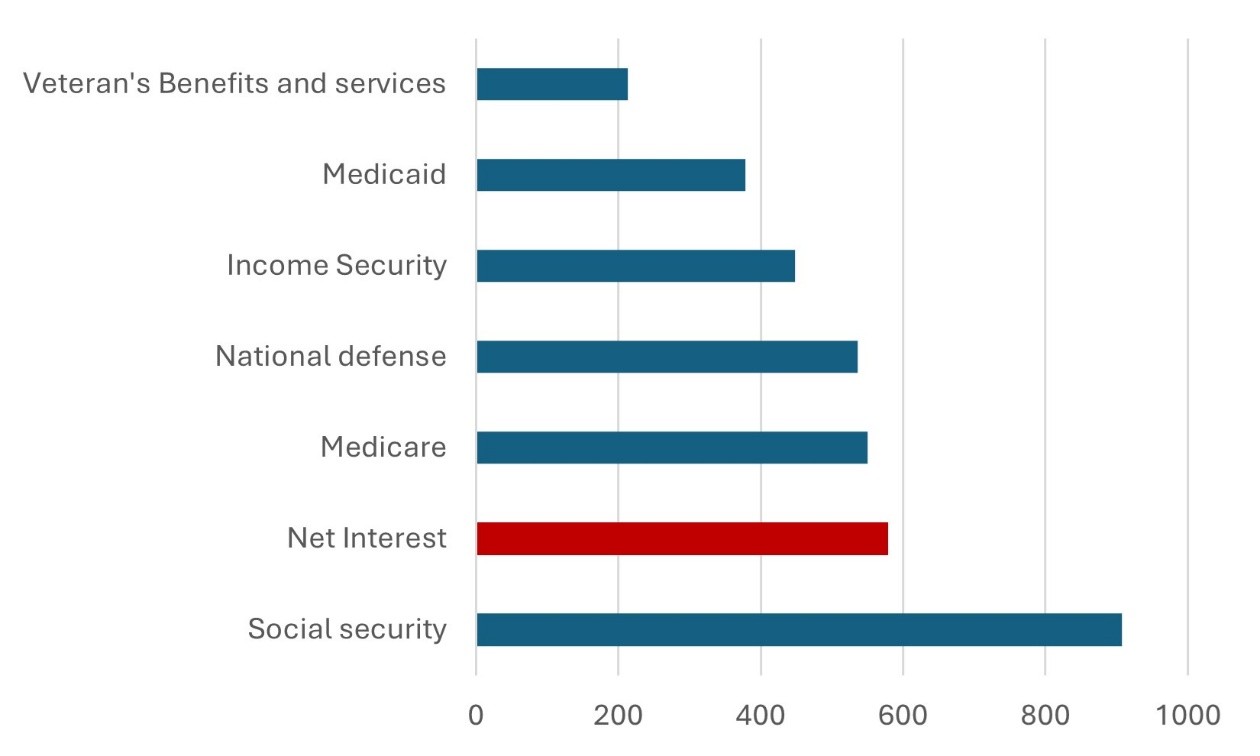

With an average coupon of just 3.267% on existing debt, and even the lowest point on the current curve yielding 3.90%, refinancing will be costly. Meanwhile, net interest payments have become the second-largest line item in the federal budget after Social Security (Chart 2).

Chart 2: Net Interest Now the Second Largest Federal Outlay by Value - FY25 ($ billion) Source: Bloomberg

Source: Bloomberg

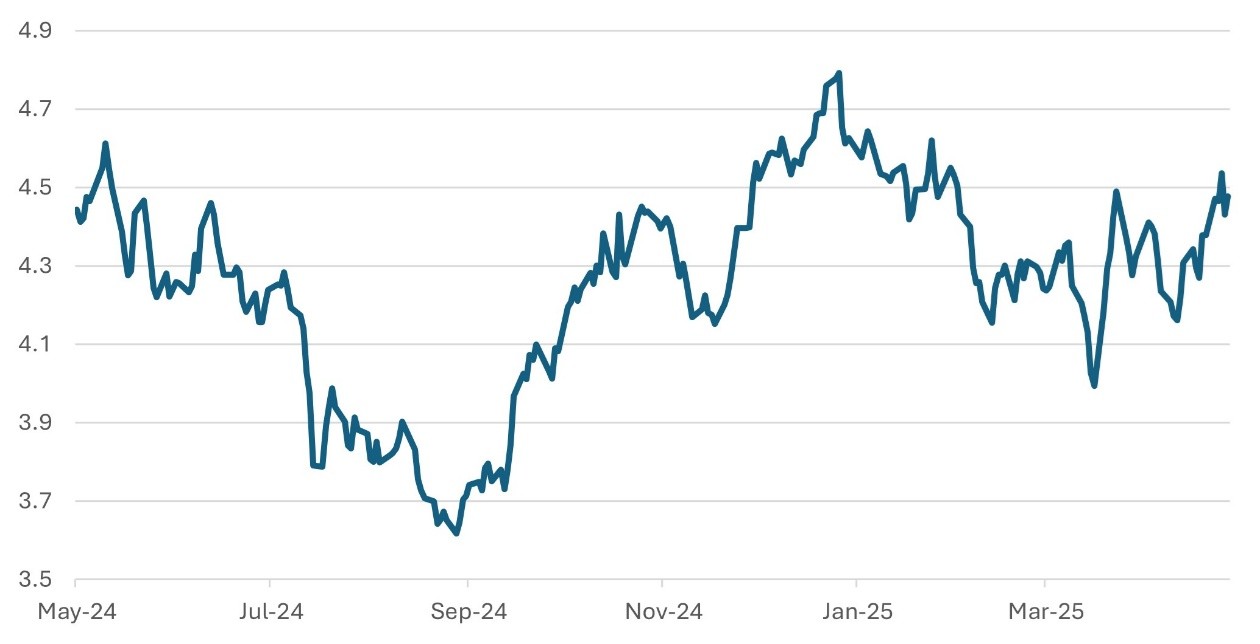

Against this backdrop, it should be no surprise that Moody’s finally pulled the trigger, downgrading US sovereign debt to Aa1 from Aaa—the last of the major credit rating agencies to do so. Moody’s cited the relentless rise in debt and interest costs, which now far exceed levels seen in similarly rated sovereigns. Although the dollar’s reserve status may limit immediate funding disruptions, the symbolic blow is clear: the US is edging into fiscal territory typically reserved for structurally weaker peers.

The downgrade also comes as Congress debates yet another sweeping tax-and-spending package. Some market participants warn of a revival in “bond vigilante” behaviour—investors demanding higher yields for the apparent fiscal indiscipline. For many, Moody’s move is less a final verdict and more a warning shot—this could be the beginning of a broader, more sustained repricing of US fiscal risk.

Chart 3: US 10-year Bond Yield Pushes Back Up to Around 4.50% Source: Bloomberg

Source: Bloomberg

The concerns about US debt sustainability will continue to limit the dollar’s recovery from the sharp correction seen year-to-date. We continue to hear of global institutions diversifying away from the dollar. For instance, the latest data shows ongoing dollar debt selling by the Chinese central bank. We think that the Swiss franc and Singapore dollar will continue to maintain their strength against the dollar.

Chart 4: US Dollar Spot Index Struggles to Make Headway Source: Bloomberg

Source: Bloomberg

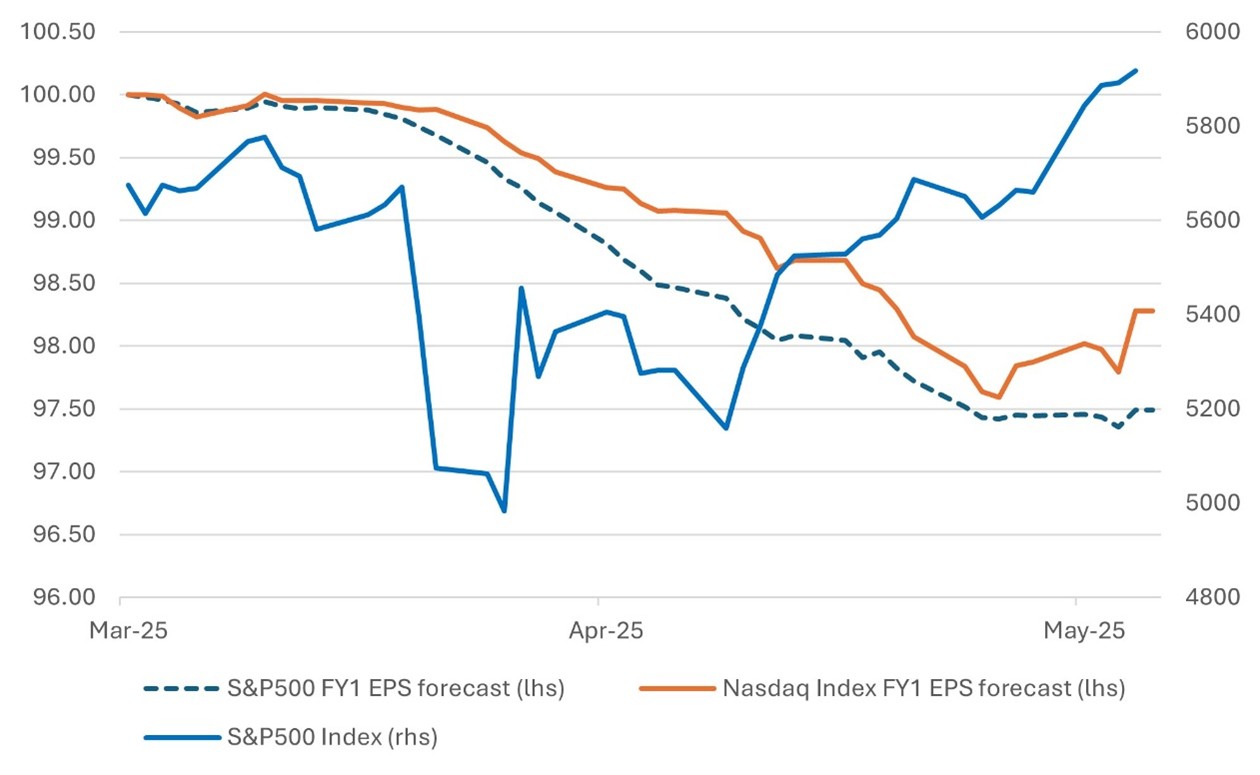

The bilateral agreement between the US and China to substantially reduce slated tariffs, at least for the next 90 days, helped the S&P500 to complete its rebound from its lows to end the week slightly positive year-to-date. The rally is particularly striking given that analysts have been revising earnings forecasts downward. That said, the most recent revisions have edged modestly higher, perhaps reflecting relief that still, the proposed tariff hikes—ranging from 10% to 30%—remain on the table and could significantly undermine corporate profitability if enacted. Our review of the S&P 500 found few instances where share prices have underperformed changes in earnings outlooks, suggesting markets remain remarkably resilient—or complacent.

As Chart 5 shows, tech has seen the most meaningful upgrades to earnings expectations in recent weeks, helping the tech-heavy NASDAQ register stronger performance versus the broader S&P500. Those on the bullish side of the fence argue that these upward revisions support a case for further gains in the index. Bears, however, warn that this could be a brief pause before another round of downgrades sets in. We remain cautious: US equities appear fully valued, and we continue to see better opportunities elsewhere in global markets.

Chart 5: US Equity Indices See Earnings Fall, but Index Rises Source: Bloomberg

Source: Bloomberg

What is Ailing Healthcare?

In more stable times, healthcare stocks might offer a degree of defensiveness to a US equity portfolio—but that hasn’t been the case recently. President Trump’s renewed threats to impose sweeping controls on drug prices has rattled investors. Although his proposals remain vague, Trump has pledged to “break the pharmaceutical cartel” and suggested using executive powers to mandate lower prices on key medications such as insulin and cancer treatments.

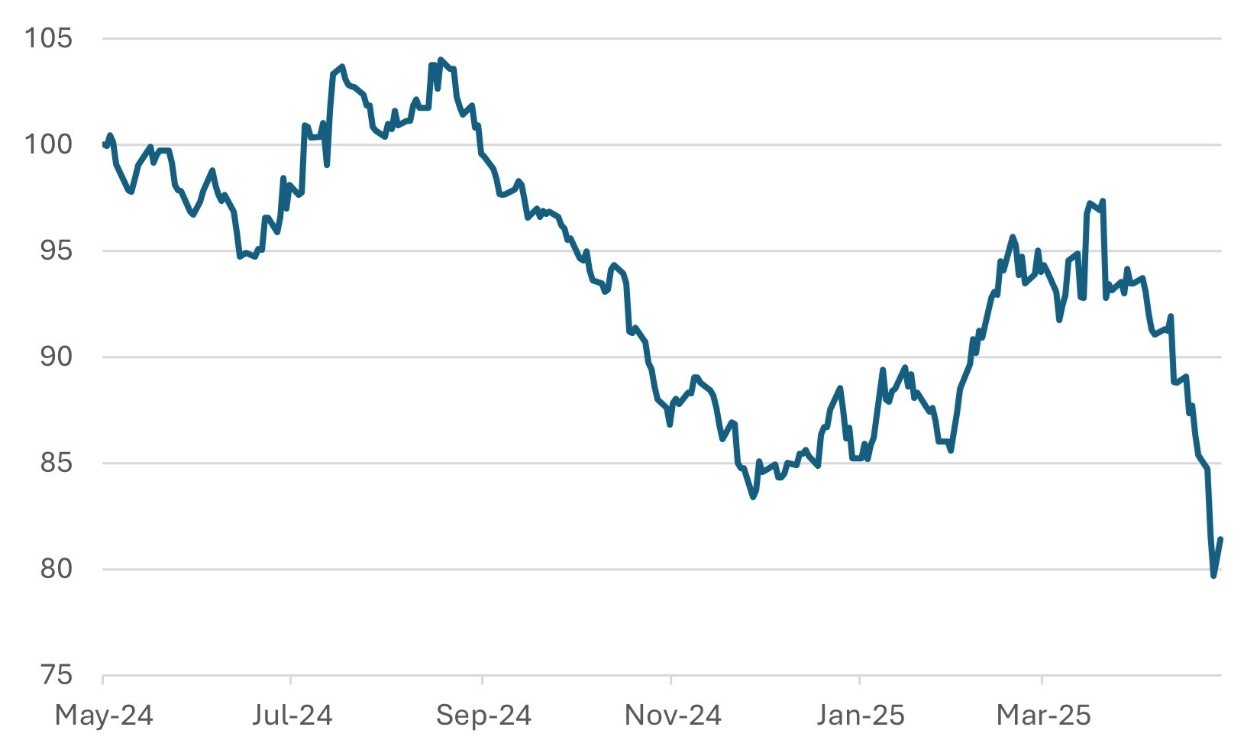

Healthcare has also lagged the broader market over the past week as regulatory risks are reassessed. That said, some analysts see the pullback as overdone. Historically, the sector has recovered well after political pressure fades, and this time, it stands out as one of the few where share prices have underperformed relative to changes in earnings forecasts. If no concrete policy emerges, the current weakness could present a tactical buying opportunity. Still, the episode serves as a clear reminder that healthcare remains acutely sensitive to policy noise, from drug pricing to broader budget reform debates.

Chart 6: US Healthcare Sector – Discounting all the Bad News? Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

19th May 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB