By Falco

22 Apr 2025

• Economic surveys and data points will provide greater clarity on the state of the global economy.

• A new set of IMF forecasts will provide some guidance to the downside to growth and upside to inflation.

• Trump's attack on Fed chair Powell does not bode well for long-term bond yields - real yields may rise further.

• US retail investors buy the dip with leverage!

• Dollar index technicals do not look good.

Since the presidential inauguration in January, markets have largely been reactive to policy announcements and the varied responses triggered by continuous updates from the White House. Even as global markets remain on edge, we believe a string of economic data due out over the rest of this month will provide greater context on the actual impact of the tariff mayhem on global growth.

Activity data for the first quarter, on the surface, has been stronger than expected but there is a sting in the tail. Last week’s US retail sales and China’s GDP reports exceeded forecasts. However, much of this “positive” data reflects a pull-forward of purchases as both industrialists and consumers, anticipating higher prices because of the tariffs, resorted to “panic buying”. JP Morgan estimates suggest that US imports in Q1 may have grown by more than 20% on a quarter-on-quarter annualised basis. Meanwhile, China’s Q1 GDP growth was a robust 6.6% annualised. However, the consensus anticipates that the tariffs will reduce future growth to 3.5% from 4.5% in 2025, even assuming a significant fiscal stimulus to support the economy.

Sentiment surveys to provide the first scaling of the turmoil in the global economy

This week, several key economic surveys will offer significant insights into how consumers and corporations are assessing the future. On Tuesday, 22 April, S&P will release a series of confidence surveys across major economic zones, including the US, Europe, China, Japan, and Australia. On Wednesday, the release of the Fed Beige book which gives some anecdotal evidence of the mood on the US industry. Economists generally expect these surveys to indicate weakness compared with previous reports, but this remains a challenging prediction. Given the extraordinary circumstances of recent weeks, there is potential for confidence levels to fall well below expectations.

IMF Economic Forecasts: A Reality Check

Importantly, the International Monetary Fund (IMF) is set to release its updated World Economic Outlook on Tuesday. Market expectations are for a significant downgrade to global growth forecasts for 2025, primarily because of the impact of US tariffs. While a global recession is not yet projected, the IMF has warned that the trade tensions are expected to weaken global economic growth and increase inflation. When the data hits the headlines, I am not saying ignore it, but analysis shows that the IMF tends to overestimate GDP growth by around 50bps when the global economy is turning down.

In the US, the probability of a recession within the next year has risen to 45%, up from 25% in March, according to a recent Reuters poll. Inflation expectations have surged simultaneously, constraining the chances of interest rate cuts by the Federal Reserve. Most economists now predict just two rate cuts by year-end. Current consensus forecasts compiled by Bloomberg show a sharp drop in growth in Q1 compared with Q4 2024.

Table 1: Bloomberg Consensus G8 Aggregate GDP Forecasts Quarterly Annualised

| Q4 24A | Q1 25E | Q2 25E | Q3 25E | Q4 25E | Q1 26E | Q2 26E |

| 2.0% | 0.9% | 1.1% | 1.1% | 1.3% | 1.5% | 1.6% |

Source: Bloomberg

Bond Market: The Growing Tensions Between Trump and Fed Chair Powell

Tensions between President Trump and Federal Reserve Chairman Jerome Powell have intensified, with the President repeatedly criticising Powell's monetary policy. Powell’s term at the Fed ends next year, and concerns are growing that a politically motivated appointment could undermine the Fed’s independence. In fact, President Trump has even suggested that he may end Powell’s tenure sooner than expected. Powell meanwhile noted that “The inflationary effects [of tariffs] could also be more persistent…[and that] without price stability, we cannot achieve the long periods of strong labour market conditions that benefit all Americans.”

Ratcheting up the rhetoric, Trump posted on his social media app, Truth Social, that “Powell’s termination cannot come fast enough!” and argued he could fire Powell at will.

The ongoing conflict over US monetary policy raises significant risks of political interference, potentially setting back the US monetary framework by decades. The 1980s and 1990s marked a painful transition to a global monetary system that was universally non-political and focused on controlling inflation. While central banks have not always been without shortcomings, their credibility and perceived independence have been crucial in lowering risk premiums and fostering long-term market stability. Should that credibility be shattered or policymaking become politically compromised, there is a real risk of long-term borrowing costs shooting up significantly.

Chart 1: US Real 10-year Yield Headed Back to Levels of the 1990’s?

(%) Source: Bloomberg

Source: Bloomberg

Such a shift could erode market confidence and result in higher long-term borrowing rates, reminiscent of the 1990s when volatile inflation expectations drove up risk premiums. As we have recently forecast, we are particularly concerned that the 10-year US government bond yields could shoot up to 6%, reflecting inflation levels of 3-5% and higher real yields at the long end of the bond market.

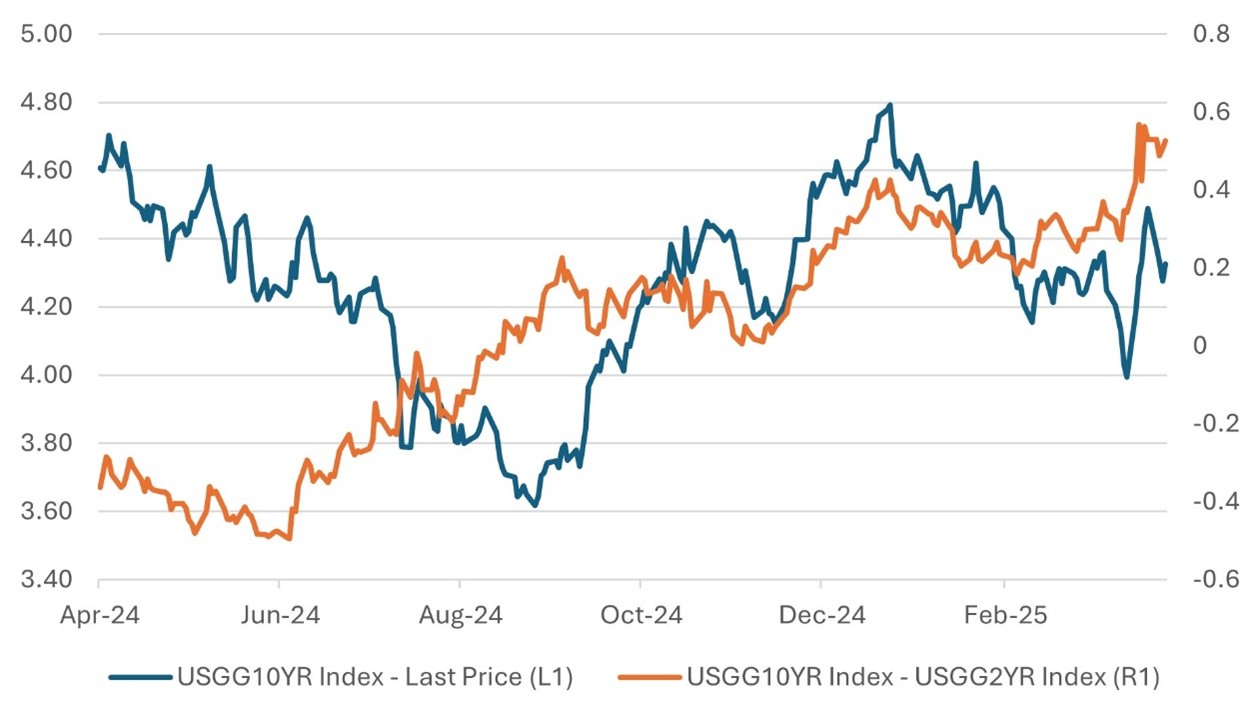

Chart 2: US Yield Curve Steepens Even as the US 10-year Yield Drops Back  Source: Bloomberg

Source: Bloomberg

Prepare for a Rocky Couple of Quarters with a Likely Worse Second Half of the Year

Most economists expect the full impact of tariffs to begin to significantly affect the global economy in the third quarter. However, the current consensus is that in the current quarter, global growth will slow from an annualised rate of around 2.5% in Q1 to just over 1.0%.

There is hope in the markets that the scope of the tariffs announced could be reduced. The 90-day tariff pause announced by President Trump on 9 April is still in effect, with the deadline set for 9 July. However, tariffs on Chinese goods have already started to take effect and will begin affecting trade. US-bound exports from China are expected to decrease by two-thirds, which could result in a 10% drop in overall Chinese exports.

Last week’s discussions between the US and Japan on tariffs failed to yield any substantial agreement, despite President Trump’s direct involvement. The two sides are scheduled to meet again before the end of the month.

Asset Markets at Sea

Never make the mistake of assuming that the current market direction offers any insight into where it is headed. The statement is particularly true of bear rallies. Last week we saw a profound, off-the-charts buy-on-the-dip mentality in the US equity market. Leveraged ETF trading surged to an all-time high. Some investors clearly want to play the casino.

A Further Fall in the Dollar Still Appears to be the More Likely Outcome

The US Dollar Spot Index sits close to the key support level. A precipitous 10% correction still looks like a real possibility, something that could spook the markets.

Chart 3: The Scariest Chart of the Lot – Dollar Spot Index at Key Support Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

22nd April 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB