By Falco

23 Jun 2025

The US attack on Iran’s nuclear facilities adds another dimension to the already volatile situation in the Middle East. While global markets will carefully analyse developments in the oil market to gauge the impact of the unfolding situation, we, like President Trump, are hoping that peace will eventually prevail.

Through Sunday, cryptocurrencies were the only significant asset class trading. Bitcoin fell 3.2% within hours of the announcement of the US military action. Stablecoin, namely USDT, traded higher as crypto traders sought shelter from the volatility. In early Asian trading, the dollar and gold have seen a rise in value. We remain more convinced of the upside in the gold price than a sharp rise in the value of the dollar.

In our view, a spike in the oil price is the immediate transmission mechanism between what has happened in Iran in the last 24 hours and the global economy. Recent US inflation had surprised to the downside, but an element of that improvement came from the marked drop in oil prices since the beginning of April. However, oil prices now trade 27% above the May low of $60.2 per barrel.

Asset prices, in our view, are not discounting the persistence of higher oil prices. At this stage, it remains to be seen how the Iranian government or its proxies will react. Any action on their part that drives concerns that oil prices could persist or go beyond current levels (Brent $77/barrel) will likely lead to higher inflation and consequently higher bond yields. JPMorgan estimates that if the 15% increase in the Brent crude price sustains, it could boost global inflation by two percentage points annualised in the second half of 2025.

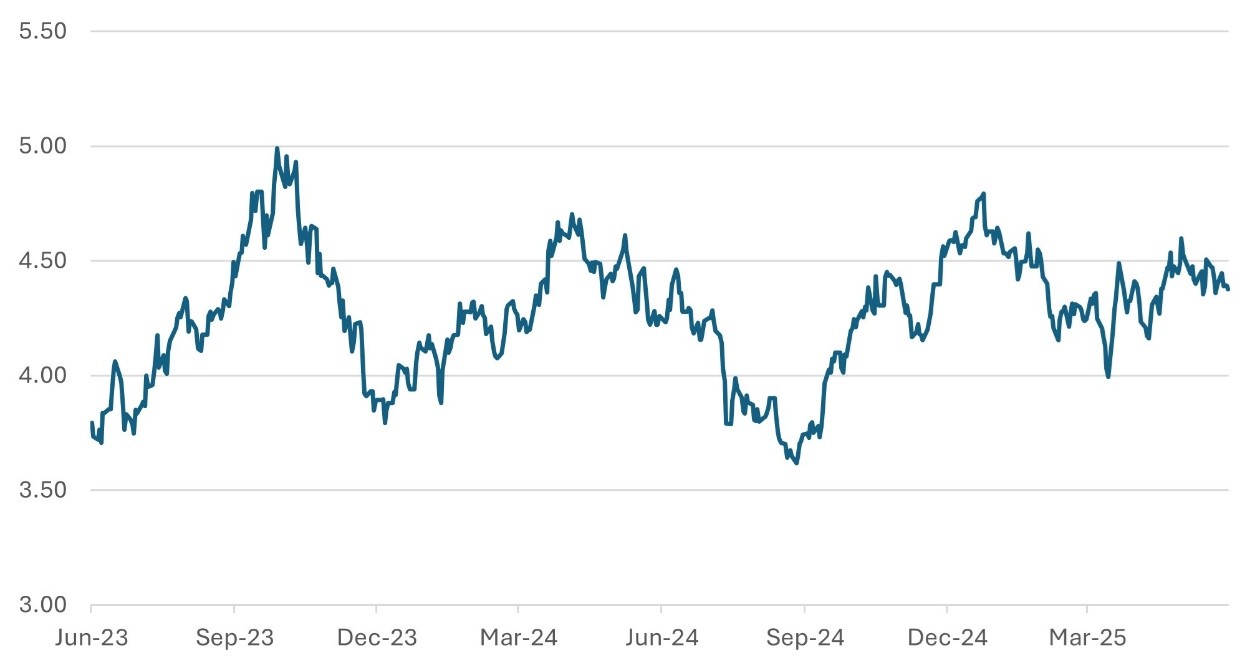

As a measure of that market’s complacency about the outlook for inflation, the US two-year breakeven, which is the implied level of inflation priced into the two-year US inflation-linked bonds had been slipping back in recent weeks (Chart 1). We expect to see a sharp reversal of inflation expectations, which may lead to possible gains for short-dated indexed linked bonds.

Chart 1: US Two-year Inflation Linked Bond Break-even Inflation Complacency (%)

Source: Bloomberg

We will leave it to the geopolitical experts to gauge the possible consequences of the US military strike on the nuclear facilities on the prevailing situation in the Middle East. However, it is clear that investor risk-taking will be reined in. Volatility in bond and equity markets has been relatively subdued of late and should reverse but there are reasons to believe that the initial reactions could be tentative and modest, barring any real attempts that Iran takes to block shipping access through the Straits of Hormuz.

Equities are not starting this phase of the Iran conflict in overextended territory. Major equity markets only trade around 4% above their respective 200-day moving averages and 3% above their 50-day moving averages. Asia ex Japan, which is marginally more extended, is geographically furthest from the problems.

Table 1: Equity Market Technicals Do Not Give Reason to be Worried About Any Significant Downside

Percentage deviations from moving averages

| Developed Markets | vs. 50D | vs.200D |

| S&P500 | 4.0% | 2.6% |

| DJ Industrial | 1.8% | -0.7% |

| Nikkei | 4.5% | 1.3% |

| EUROSTOXX | -0.6% | 2.3% |

| FTSE 100 | 2.3% | 4.1% |

| SMI | -1.2% | -2.4% |

| Asia ex Japan | 4.5% | 7.1% |

| Nasdaq | 6.1% | 4.6% |

| Global | 3.1% | 3.7% |

Source: Bloomberg

In the bond markets, unless oil prices spike sharply, we see little reason for a marked deviation of yields from their current levels. The immediate take on the latest developments in the Middle East is that they could subdue growth and investors’ risk-taking appetite. Hence, absent a large rise in oil prices, we expect US bond yields to remain around current levels.

Chart 2: US 10-year Bond Yield Range-Bound Source: Bloomberg

Source: Bloomberg

FOMC: Split and split again

In other news, the Fed decision to leave rates unchanged last week was not a surprise, but subsequent comments by FOMC member Chris Waller were. The meeting brought to four differences between the FOMC members, with one group believing that they would not cut rates while the other being of the view that two rate cuts could indeed come by year-end. Chairman Powell was at pains to explain to the market that the committee remains concerned about the impact of the tariff increases on headline inflation.

It only took a matter of days though before Waller broke ranks with the FOMC and suggested that a rate cut might be warranted at the end of July. In an interview on CNBC’s Squawk Box on Friday, he indicated that recent inflation trends now appear “pretty good” and expressed confidence in the Fed’s ability to look through any tariff-related price spikes. He remarked:

“Any tariff inflation … I do not think is going to be that big and we should just look through it in terms of setting policy. The data the last few months has been showing that trend inflation is looking pretty good … We could do this as early as July.”

As we approach the 3 July deadline for agreements to be in place, markets appear increasingly convinced that we may witness yet another TACO moment—"Trump Again Chickens Out"—with the president opting to extend the deadline rather than escalate tensions further. While the optics of hardline trade rhetoric remain politically useful, the actual imposition of tariffs remains a risk that the market is discounting, perhaps prematurely.

Asia ex-Japan cools

In the meantime, the varying regional impacts of the tariff threat are becoming more evident. Across Asia ex-Japan, there are signs of cooling momentum. The earlier flurry of front-loaded exports—driven by attempts to pre-empt potential tariffs—has largely run its course. The resulting air pocket in shipments is starting to weigh on near-term growth data, particularly for export-sensitive economies such as South Korea, Taiwan, and Vietnam.

Chinese growth is robust but active policy support is likely to wane

China, on the other hand, has faced a more immediate and sustained hit to its external trade flows. With US-bound exports already under pressure, the government has leaned more heavily on domestic demand to boost growth. Encouragingly, recent data suggests that the stimulus efforts are gaining some traction. Both retail sales and industrial production figures for May exceeded expectations, pointing to modest but welcome stabilisation in the economy.

Nevertheless, the authorities appear content with the current trajectory and are unlikely to unveil further large-scale support measures. The upcoming July Politburo meeting is expected to reaffirm this cautious stance. On the monetary side, the PBOC may offer only a token 10-bp rate cut—more a gesture of intent than a stimulus lever. Policymakers remain acutely aware of the risks of over-easing, particularly of the dangers of reinforcing deflationary expectations among households.

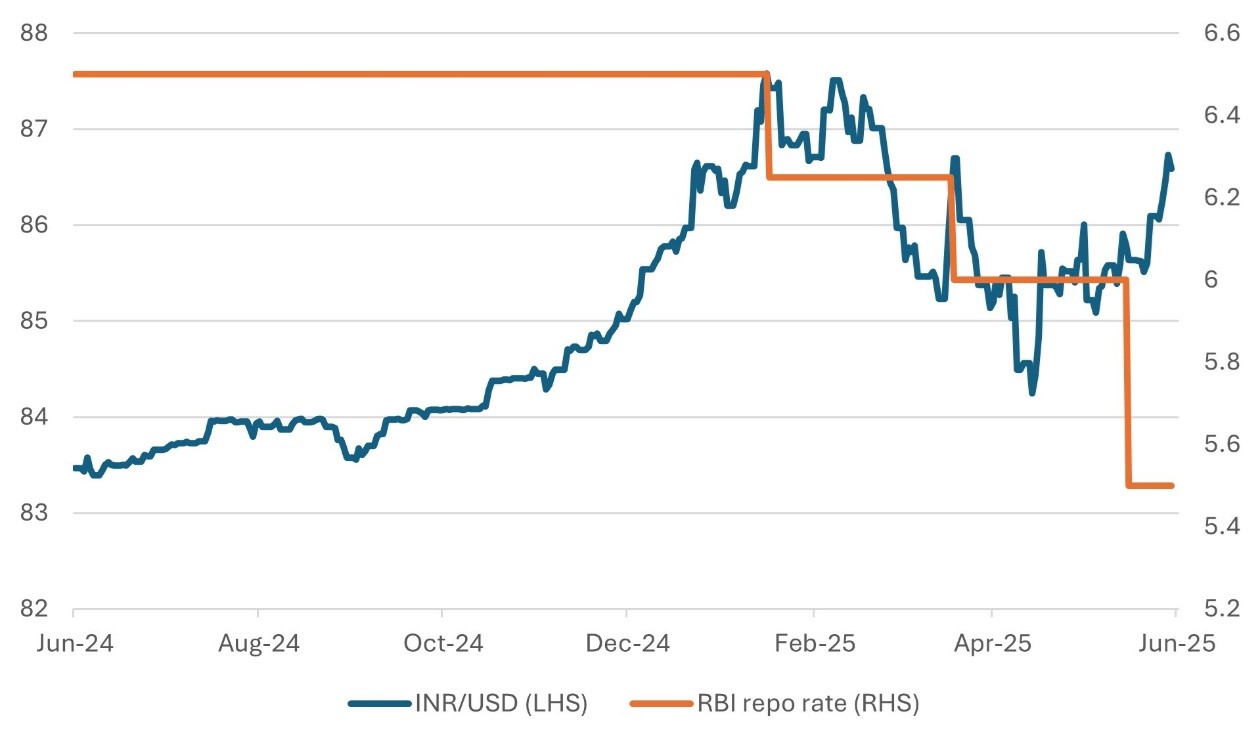

India and Indonesia’s currency weakness limits further central bank easing

Elsewhere in the region, policymakers are facing a dilemma. On the one hand, there is the desire to support domestic demand amid external uncertainty; on the other, the threat of capital outflows limits the scope for rate cuts. India and Indonesia, for example, have adopted a more cautious tone despite the recent softness in inflation, preferring currency stability and capital market resilience over aggressive easing.

Chart 3: Rupee Weakness Likely to Hold Back RBI from Easing Still Further Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

23rd June 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB