By Falco

24 Mar 2025

• Buy-the-dip helps US equities edge higher, as other markets are quiet.

• US equities however, are hampered by challenging technicals and weak earnings revisions.

• Chinese equities slide as India improves.

• The Fed is on hold, maybe until the end of the year.

We observed a subtle shift in market dynamics last week, with some rotation away from recent high-flying markets and investors exhibiting cautious optimism. The S&P 500 edged up 0.5% on the week, but India’s 30-share benchmark Sensex and the broader Nifty were outliers in terms of gains, each surging 4.2% and outperforming many of their strongly performing counterparts in Europe and China.

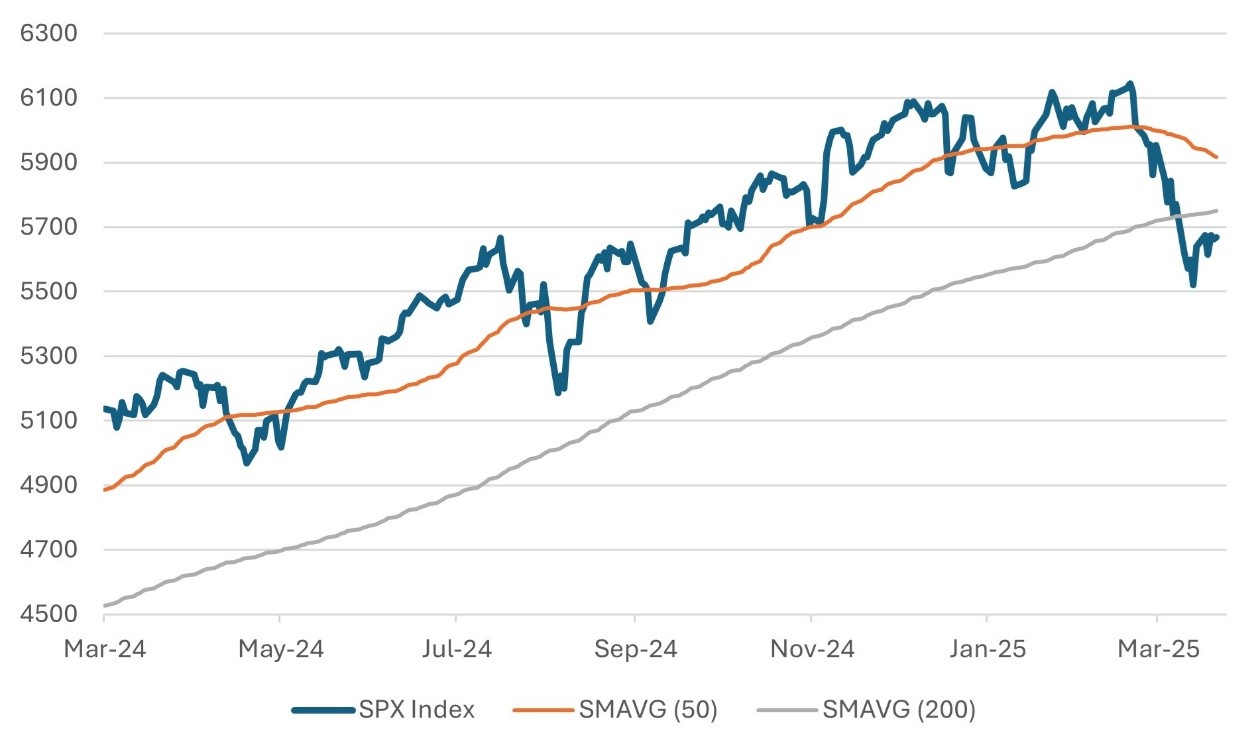

Meanwhile, in the US, the “buy-the-dip” mentality appears to be alive and well, with Bank of America reporting the third-largest monthly inflow into equities—measured as a percentage of assets under management by its private clients—since March 2012. However, despite this renewed enthusiasm, technical indicators suggest investors should remain cautious. The S&P 500 index, for instance, is still trading below its 200-day moving average, a key long-term trend signal. Additionally, the 50-day moving average continues to trend downward, indicating that short- to medium-term momentum remains soft.

In short, while inflows and investor sentiment have improved, the technical setup has yet to confirm that a more durable recovery is under way. A sustained breakout above these moving averages would help build the case for a stronger upside, but until then the bulls should tread with caution.

At this juncture, we advise investors to keep an eye on technical resistance levels and sector rotation. Momentum is improving, but a broader trend reversal is still not apparent.

Chart 1: S&P 500 Rebounds But Technicals Still Challenging Source: Bloomberg

Source: Bloomberg

Notwithstanding the small recovery that we witnessed last week, market commentators argue that investors remaining so risk-averse after a relatively minor correction is a rarity in itself. It is therefore not surprising that the weekly American Association of Individual Investors sentiment survey shows 79% of the participants remain bearish or neutral on stocks.

The headwinds to the market are still very real. For example, Q1 2025 earnings estimates for S&P 500 companies, which start reporting results for the quarter in April, have declined from $226/share in March of last year to just $219/share and the decline continues unabated.

While investors continue to wonder if the US economy is heading into a recession, unfortunately the answer is still far from clear. Some economic indicators have indeed weakened, but the overall data remains mixed—not yet conclusively weak enough to call a recession.

What is also more concerning is the US housing starts data for February, which showed new US residential construction remained 5.2% below already-depressed levels from a year ago. Even more striking was the seasonally adjusted sales of existing homes, which fell to their lowest level since February 2009. Simply put, elevated interest rates and stubbornly high inflation continue to erode purchasing power and consumer confidence.

There are also emerging signs that the economy may be losing momentum more broadly. The Conference Board’s Leading Economic Index (LEI)—specifically the six-month rate of change, which has historically been a reliable recession predictor—had been showing signs of improvement. However, the latest data suggests that this positive trend is starting to falter.

While the labour market remains relatively resilient and consumer spending hasn't collapsed, investor caution is warranted. The combination of high interest rates, weakening housing activity, and shifting consumer sentiment continues to raise the risk of a more pronounced slowdown in the months ahead.

Fed Policy – Don’t be Complacent About What Could Happen

Last week’s Fed meeting was interpreted by the market as relatively benign, but we caution investors against complacency. Four FOMC members signalled no rate cuts for the remainder of the year, and both the tone of the statement and the dot plot reflected a "wait-and-see" approach on part of the Fed. There remains a clear concern that inflation could prove more persistent than anticipated.

Countdown to 2 April: Tariff Tensions in Focus

We are approaching the pivotal date of 2 April 2025, when the United States is scheduled to implement a new round of reciprocal tariffs. In what could reflect a shift in tone, President Trump on Friday indicated that there may be some flexibility in the rollout of these broad-based tariffs.

The quality of dialogue around trade policy does appear to have improved in recent weeks, particularly since the late-February appointment of Jamieson Greer as the US Trade Representative. Greer, who now leads the Office of the USTR, has brought a greater degree of consistency to the administration’s trade messaging. As the president’s chief advisor, negotiator, and spokesperson on trade, Greer’s involvement has introduced a more measured and structured approach to what has been a volatile area of policy.

Meanwhile, many of the US’s key trading partners are responding with calculated restraint. China, for example, has signalled its preparedness to weather potential economic disruptions. Premier Li Qiang reiterated the country’s commitment to globalisation and multilateral cooperation. The European Union has also chosen a more diplomatic path, delaying its planned retaliatory tariffs—which were initially slated to begin on 1 April and 13 April—until mid-April. This postponement allows more time for negotiations and for a possible recalibration of the list of US products targeted by countermeasures.

Investor Takeaway: The tone on trade may be softening, but policy risks remain elevated. April could be another volatile month for global markets depending on how negotiations evolve.

China Back to India

Both the Hang Seng and CSI 300 indices were weaker last week after the Chinese government’s announcements on a boost to household confidence and spending failed to meet market expectations. The "special action plan" unveiled by Chinese policymakers lacked substantial new details and was perceived as limited in its immediate economic impact. The plan includes measures such as trade-ins for consumer goods, wage increases, child-care subsidies, and strengthening safety nets. Analysts viewed the plan as more focused on improving sentiment rather than providing significant immediate economic stimulus.

The weakness in China’s equity market seems to have added some zip to the recovery of Indian equities. The 50-share Nifty and the benchmark Sensex each recorded their largest weekly gains in four years, rising 4.2% on the week. The disappointment in China probably added as a near-term catalyst for some movement as active EM managers repositioned their bets into equities in India, where the Sensex had fallen 15% from September last year. India’s case was also helped by some better economic data released on 12 March, with inflation surprising to the downside and industrial production to the upside. The subsequent disappointing news from China at the start of last week further reinforced the recovery. Also, and crucially, month to-date foreign institutions have turned net buyers in March, reversing the billions of dollars of selling in the previous six months.

Chart 2: India’s Sensex Index relative to the Hang Seng index Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

24th March 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB