By Falco

27 May 2025

• President Trump recharges the tariff challenge to the markets

• US bond market fundamentals remain worrying to investors

• Global growth has some positive drivers – policymakers helping in certain quarters

• Smaller markets in Latin America and Europe have achieved good returns and still may have some upside

Trade Tensions Return

President Trump’s proposed 50% tariffs on all imports from the EU announced in a seeming fit of pique about the alleged “tardy” pace of negotiations have reignited fears of a renewed trade war. The EU is expected to respond swiftly if the tariffs are indeed implemented. In late-breaking news on Sunday evening, President Trump has given the EU until July 9th rather than June 1st for an agreement to be reached.

Exporters in Asia are accelerating shipments to the US in anticipation of more tariffs. Taiwan’s earlier implied tariff peak of 32% eased somewhat because of the exemptions in semiconductors, yet recent strength in its export orders suggests Q2 GDP could surprise to the upside.

China, meanwhile, continues to reroute exports through regional partners to exploit lower effective tariffs—a strategy that may soon lose its edge if the US tightens tariff alignment across supply chains.

US equity markets responded poorly to Trump’s renewed tariff threats, suffering their worst week since early April. Mutual fund flows showed some selling pressure with investors pulling $9.4 billion from global equity funds.

Bond Markets on Edge

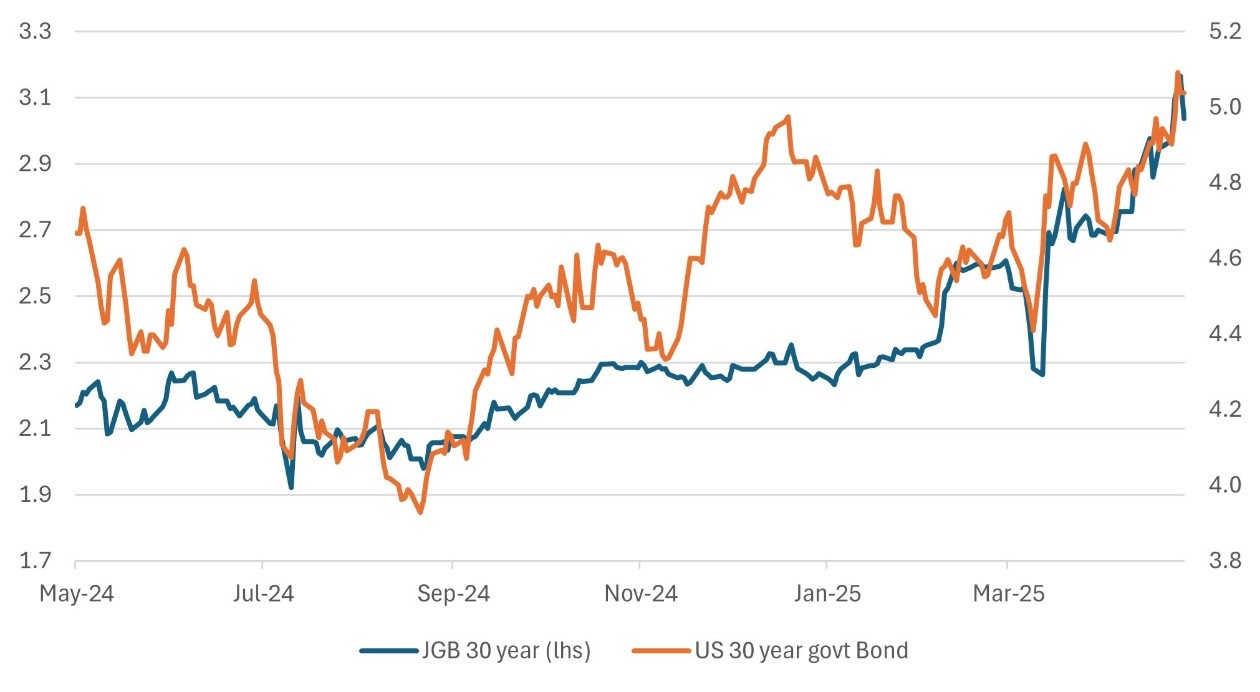

The US bond market, already strained by concerns over rising debt, took another hit last week. Moody’s recent downgrade of US credit barely moved yields, but sentiment remains fragile. A poorly received $16 billion auction of 20-year Treasuries saw a yield of 5.047%, the highest since October 2023, and a bid-to-cover ratio of just 2.46, below the 10-auction average of 2.58. Post-auction, 20-year yields rose to 5.127%, while the 10- and 30-year yields climbed to 4.595% and 5.089%, respectively. The 30-year yield pushed above 5% for the first time since 2023—its fourth consecutive weekly gain.

Adding to the bond market’s worries, the House passed the “One Big Beautiful Bill Act,” which the Congressional Budget Office estimates could add nearly $4 trillion to the national debt over the next decade. Japan’s bond market fared no better.

The 20-year JGB yield surged to 2.555%, a 24-year high, following a weak auction. The 30-year yield hit 3.14%, and the 40-year reached a record 3.6%. Investors now eye this week’s US 40-year auction, which will test market appetite further after last week’s poor response to 20-year issuance.

Chart 1: Bond Market Angst

Yields (%) Source: Bloomberg

Source: Bloomberg

Growth Holding—But for How Long?

With all the bad news around it is seemingly comforting that global economic growth has not faltered; in fact, far from it. There have been hot spots such as Asia, and European and US economies have on occasions surprised to the upside. Unfortunately, more challenging times likely lie ahead.

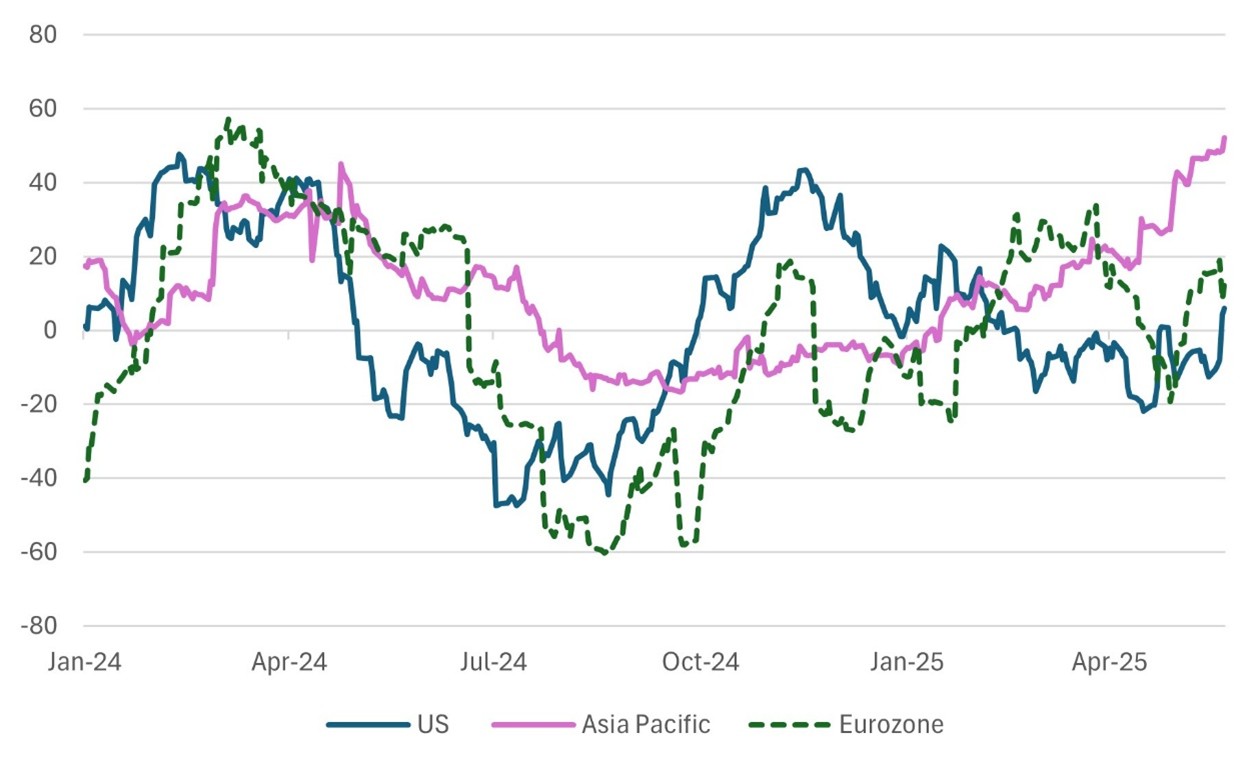

Growth so far has held up relatively well. Indeed, in recent months there has been a rising trend of economic surprises, notwithstanding all the angst around tariffs and US economic policies. Asia has led from the front with positive economic surprises matching the year-ago levels (Chart 2). However, in our view, much of these improvements may prove transitory, as companies have boosted inventories to try to move products ahead of the tariff increases. In a sense, demand is being brought forward to avoid taxes.

Chart 2: Economic Surprise Indices – Asia Leads

Index Source: Bloomberg

Source: Bloomberg

The industrial confidence data for May points to a levelling off in activity. Inflation pressures are rebuilding: the US all-industry output price index hit a two-year high, Euro area service activity softened, and confidence indicators, while modestly better, remain below last year’s levels.

Still, economies appear to be slowing from higher-than-expected starting points. Real consumption in the US is tracking a 3% annualised rate for Q2, while Asian export and production data have exceeded expectations.

Looking ahead, growth is likely to decelerate, with three key headwinds:

• The unwinding of tariff-related front-loaded production.

• US consumer purchasing power coming under pressure from rising prices.

• Slower business investment and hiring amid policy uncertainty.

Outside the US, some governments are actively supporting growth. Germany is pursuing counter-cyclical spending. China has instituted several pro-growth, confidence-boosting policies and the monetary authorities continue to provide modest rate cuts. In emerging markets, policy space is limited, but targeted spending is being used to buffer trade-driven slowdowns.

Central Bank Watch

• US Fed: The latest minutes are due out this week will likely confirm a “wait-and-see” approach to rate changes.

• Mexico (Banxico): The central bank cut rates by 50bps and flagged another cut in June, despite recent spikes in inflation.

• UK (BoE): A June cut looks less likely after strong services inflation pushed the headline CPI up to 3.5%. An August rate cut is still possible.

• Eurozone (ECB): A June rate cut remains likely amid ongoing dis-inflation.

• Indonesia & Australia: The two central banks are expected to keep policy steady this week because of easing inflation data.

Investment Opportunities Beyond the Mainstream

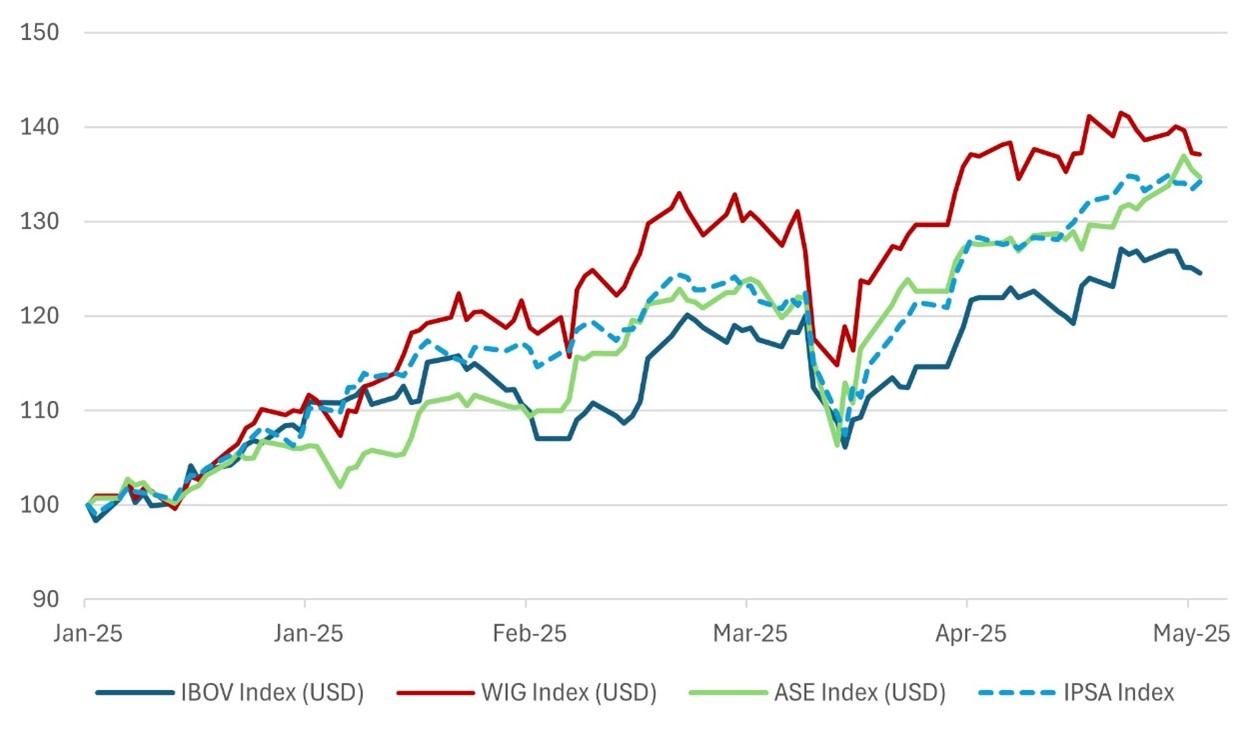

While much has been made of the major European markets outperforming the US, there have been other pockets of outperformance, too. Several smaller equity markets in the region have delivered strong year-to-date performance. Poland, Greece, Brazil, and Chile have all posted gains exceeding 25% in US dollars, significantly outperforming developed markets.

Key drivers of the outperformance include:

1. A robust Latam that is more immune to tariff trouble: Latin America looks to be tracking at around 3% GDP growth and looks likely to be relatively immune to the tariff increases.

2. Partly aided by Germany’s recently announced stimulus plan and ongoing structural change in the smaller countries, several smaller European markets have performed well. Earnings growth in Polish companies is expected to hit double digits this year, and the market remains attractively valued relative to Western peers. Greece has undergone something of a metamorphosis with a transformation in the finance sector.

3. Commodity Exposure: Countries such as Chile, Peru, and Colombia are benefiting from higher commodity prices, particularly copper and energy.

4. Global Asset Rotation: Institutional investors are increasingly looking for less correlated sources of return, moving capital into smaller, under-researched markets.

This reallocation reflects a more general fatigue with the concentration risk in large-cap US technology stocks. Nvidia's earnings release on Wednesday will be closely watched, with growth expected to slow to 67% year-on-year, down from 78% in the previous quarter.

Chart 3: Smaller Markets Remarkable Rally

rebased to Jan 2025=100 Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

27th May 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB