By Falco

28 Apr 2025

Investors find themselves navigating a period of uncertainty, particularly as they await greater clarity on tariffs, with the US-China negotiations remaining a focal point. While the concerns are warranted, patience is essential, as the resolution of these trade tensions remains fluid, and there is no clear timeline for when – and if – a consensus would emerge. In the meantime, investors are closely monitoring economic data for any early signals of how tariffs are influencing global growth and inflation.

The market is particularly attuned to sectors such as manufacturing, retail, and commodities, with any significant shifts in these sectors likely to serve as early indicators of broader economic consequences. As the economic outlook continues to unravel, thanks largely to the turmoil caused by tariffs, much will depend on the timing and substance of tariff-related news in the coming months.

A Global Economy Holding Its Breath

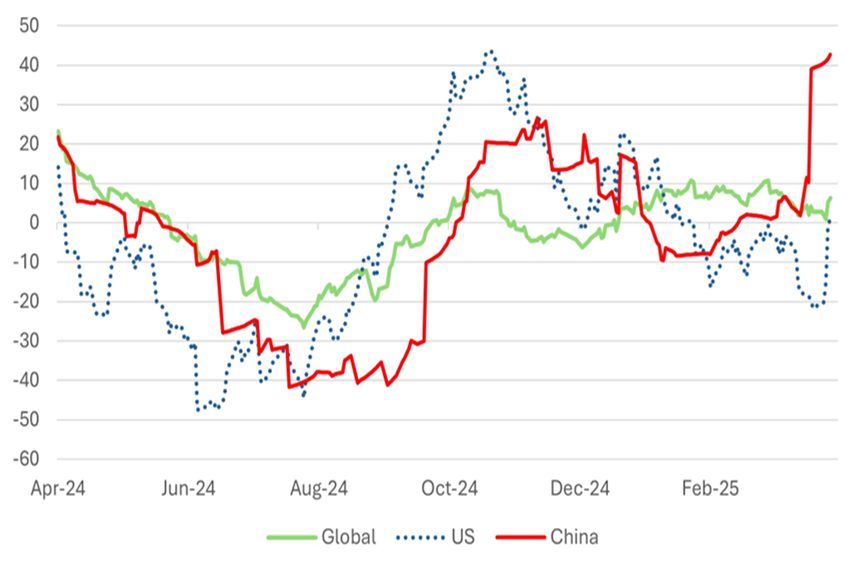

If only President Trump had left well enough alone. Recent economic data from both the United States and China have been positive, indicating that the global economy was in a solid position before tariff-related concerns spooked sentiments and markets. China’s Economic Surprise Index, for instance, has surged to its highest levels in months, and the US saw a notable uptick in growth in recent months. Other economies, too, appeared robust, but that, unfortunately, seems set to change.

Chart 1: Economic Surprise Indices Show a Robust Global Economy Before Tariff News

Source: Bloomberg

The IMF’s Revised Forecasts

The IMF updated its economic forecasts last week, offering a glimpse into the global economic trajectory post-tariff turmoil. Key revisions include:

The US has been hit the hardest, with projections for both growth and inflation worsening. In contrast, the IMF has downgraded its inflation forecast for the Eurozone, providing the European Central Bank (ECB) with the room to potentially cut interest rates to stimulate growth. ECB officials have already indicated the possibility of a rate cut in June.

Implications for Eurozone Bonds

The ECB’s more dovish stance bodes well for Eurozone bonds, with markets now expecting a number of rate cuts through the remainder of the year. While US rate cuts are also anticipated, they may be accompanied by a steepening of the yield curve, which could pressure long-duration bonds. Cutting rates in an inflationary environment could erode confidence in the bond market, particularly if the ECB pursues aggressive stimulus measures.

Tariffs and the Trade Tensions Vacuum

Markets remain on a wait-and-watch mode as they wait for clarity on the final tariff arrangements. Despite numerous attempts by countries to engage in trade talks – and notwithstanding the flip-flops by the administration – US officials have not yet reached concrete agreements on trade, including with Japan and South Korea. The Trump administration reportedly received 18 trade proposals but continues to emphasise patience as negotiations continue.

The good news is that the administration seems to be backpedalling on several of its initial tariff threats. For instance, on 23 April, President Trump announced that car parts would be exempted from tariffs, including those on imports from China and their steel and aluminium duties. However, the 25% tariff on fully imported foreign cars remains in place, along with a new 25% duty on imported car parts set to begin on 3 May. This partial rollback is designed to alleviate pressure on automakers while preserving some of Trump’s protectionist measures.

The Outlook: Market Confusion and Economic Disquiet

Despite some positive news, the market still seems to be in a state of uncertainty, lacking a clear handle on the likely impact of tariffs on the US as well as global growth. Surveys last week showed a marked decline in both industrial and consumer confidence. The S&P combined surveys for manufacturing and services fell to a 16-month low, indicating a deteriorating outlook.

Relevant economic data remains scarce at this point and will only become relevant with the passage of time

This leaves markets without concrete indicators to assess the likely trajectory of global growth—despite investors increasingly turning to economic data to gauge the impact of tariffs. While some tariffs have already been implemented, others are on temporary hold, and some have been cancelled. The resulting uncertainty leaves companies hesitant to make major investment decisions, especially those contemplating significant capital expenditures.

Corporate America on Pause

US companies, as they report first-quarter earnings, are increasingly shying away from providing clear guidance on their revenues and profits for the second quarter. A growing number of firms are halting shipments to the US for fear of unpredictable tariffs. Companies, especially in sectors such as tech and automotive, are in a tight spot, with shifting tariff policies complicating their ability to plan and price effectively.

Equity Markets: Relative Judgment Over Absolute Confidence. When assessing equity market performance, relative judgment seems more relevant than absolute predictions

European markets, for instance, continue to look better positioned both economically and from an investment standpoint. Active managers in Asia report generally positive news from China and Japan.

In China, while certain sectors will inevitably face headwinds from tariffs, active managers are finding companies with single-digit P/E multiples and strong visibility over robust domestic growth, with earnings growth rates expected to be around 20%. In Japan, although tariff negotiations remain unclear, domestic demand and corporate restructuring efforts remain favourable themes for stock selection,

US equities remain under pressure even if they managed to generate a 4.6% return last week. This week sees a blockbuster week packed with earnings from across tech, healthcare, finance, and energy. Four of the magnificent 7- Apple, Microsoft, Amazon and Meta report. Among the other sectors reporting the market will be particularly interested in the consumer sector where reports and comments will be scrutinised for robustness of consumer demand and signs of inflation. Coca Cola, McDonald’s Starbucks and Kraft Heinz are among those reporting. UPS may give us a take on whether they see an early impact from the first round of tariffs.

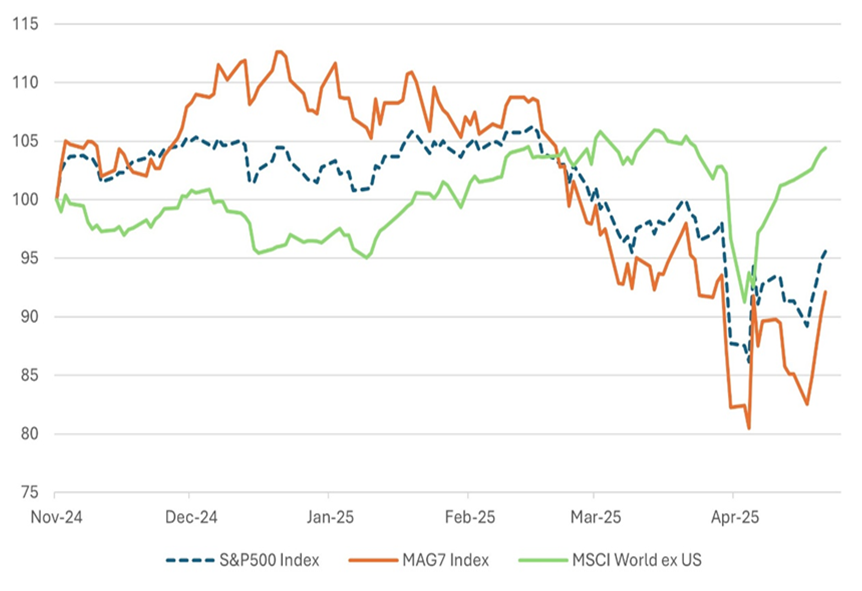

Chart 2: World ex US has outperformed MAG7 and S&P500 since US Election Day

(local currency rebased to November 5th =100)

Source: Bloomberg

Indian Equities Solid Amid Uncertainty

Indian equities have emerged as standout performers throughout this crisis. The Nifty 50, which represents 50 of the largest Indian companies listed on the National Stock Exchange, has rebounded nearly 10% from its early April low. Minutes from the Reserve Bank of India’s most recent meeting, held in early April, revealed that the Indian central bank anticipates further rate cuts this year, as it remains confident that inflation is under control. We remain overweight Indian equities, as the outlook for growth remains strong despite prevailing global uncertainties and political challenges.

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

28th April 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB