By Falco

30 Jun 2025

The past few weeks have seen growing confidence priced into financial markets regarding forthcoming rate cuts by the U.S. Federal Reserve. This optimism stems from two core drivers: first, the evolving macroeconomic landscape, and second, mounting political pressure from the U.S. government urging monetary easing. As of now, futures markets are assigning an almost 100% probability to a 25-basis-point cut by the Fed in October—a shift that has underpinned much of the recent risk-on sentiment and market performance.

Both the S&P 500 and Nasdaq reached fresh all-time highs last week. But viewed through a broader global lens, international investors might well ask, “So what?” The Euro Stoxx index has delivered a striking 23% year-to-date return in U.S. dollar terms, far outpacing the S&P 500 and Nasdaq, which are each up only around 5%. This divergence reflects deeper structural valuations—U.S. equities continue to trade at a substantial price-to-earnings premium relative to their European peers.

There appears little reason, at least for now, to expect a sharp reversal in the underperformance of U.S. equities. The valuation gap remains unresolved unless the U.S. tech sector begins to post material upward earnings revisions—yet recent trends offer little support for that outcome. While bullish analysts may highlight strength in certain sub-sectors, the aggregate earnings momentum is tepid at best.

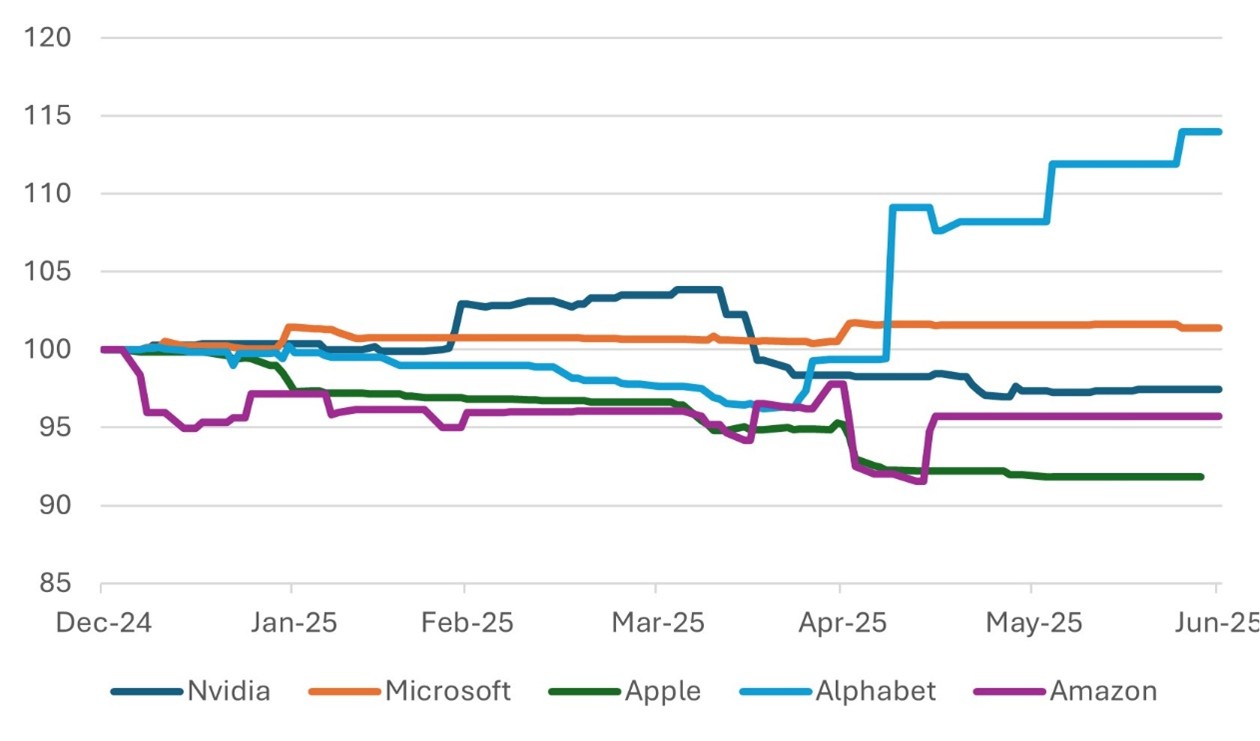

Chart 1: Market Earnings Estimates for Leading US tech Companies Largely Revised Down

Chart shows consensus earnings forecasts for leading tech stocks since the start of the year Source: Bloomberg

Source: Bloomberg

Aside from Alphabet and Microsoft since the start of 2025 earnings estimates of the leading five tech US stocks have seen consensus earnings estimate fall year to from the start of the year.

This sets an uneasy backdrop as markets close out the second quarter and attention shifts to the upcoming U.S. corporate earnings season. Investor nerves are on edge. More than 30 prominent U.S. companies—spanning key sectors such as airlines, autos, retail, consumer goods, and technology—have either withdrawn or withheld full-year 2025 guidance during their Q1 or Q2 updates. This signals a climate of deep uncertainty.

The global macroeconomic backdrop for the third quarter appears increasingly challenging. While uncertainty persists around the U.S. tariff agenda, the balance of risks suggests rising inflation pressures and slowing growth into year-end. The front-loading of global orders—particularly from Asia—has likely distorted demand patterns and may contribute to a sequential decline in quarter-on-quarter growth.

Although selected central banks, notably in Europe, have already cut policy rates, further easing may be limited for the remainder of the year. Amongst emerging markets, the rate cuts in places like India look like they are almost done for this year absent a marked weakness in growth. In the U.S., expectations for imminent Federal Reserve rate cuts may be premature. This week’s U.S. labour market report is expected to show an unemployment rate of around 4.3%—far from a crisis level. The more dovish members of the FOMC are unlikely to find in the data the kind of emphatically weak signals needed to justify a rate cut as early as July.

Democracy, Autocracy, and the U.S. Market Premium

U.S. exceptionalism is increasingly under scrutiny in financial markets, not just in economic terms but also with respect to governance. Last week’s Supreme Court ruling has added to this debate. While procedural on the surface, the decision raises important questions about the traditional balance of power between the executive, Congress, and the judiciary — a core pillar of the U.S. Constitution.

At its heart, the Constitution is designed to manage the tension between democratic accountability and the risk of executive overreach. It relies on institutional friction and public transparency to maintain balance. However, it does not prevent shifts in that balance through mechanisms such as:

The recent Supreme Court judgment may, in practice, reduce the speed and scope of judicial checks on executive power — particularly if Congress remains deadlocked. It has prompted some constitutional scholars to express concern that the U.S. system may be tilting toward a concentration of power in the executive branch, without the usual checks functioning as intended.

From an investor perspective, this evolution is not an academic concern. Political risk is increasingly being priced into assets. The U.S. dollar, for example, weakened again last week, with the DXY index slipping further. Technical analysts now point to a continued trend lower, potentially reflecting investor discomfort with both fiscal and constitutional uncertainty.

Chart 2: Core PCE inflation Moving Closer to Fed’s Target Source: Bloomberg

Source: Bloomberg

Equity valuations often serve as a barometer for investor perceptions of political institutions. Currently, global equity markets in democracies—excluding the United States—tend to trade at average price-to-earnings multiples of approximately 16 to 21 times. In contrast, markets in more autocratic regimes typically command far lower valuations, generally in the range of 10 to 12 times earnings. This persistent valuation gap highlights investor preferences for environments offering greater transparency, institutional stability, and adherence to the rule of law.

Historically, the United States has enjoyed a valuation premium relative to global peers, thanks to its legal infrastructure, depth of capital markets, and institutional credibility. However, that premium may increasingly come under scrutiny as investors reconsider the trajectory of U.S. political governance and its implications for long-term market risk.

Looking ahead, several macro factors could shape market direction in the coming week. In China, key economic data releases will provide insights into whether policymakers are under immediate pressure to expand stimulus efforts to counteract slowing momentum. Meanwhile in the U.S., markets remain fixated on evolving expectations around Federal Reserve policy, particularly as incoming data shapes the narrative around the timing and magnitude of potential rate cuts.

| Date | Event |

| July 1st | China June PMI (flash), global PMI bundle (US, Euro, UK, Japan) |

| July 2nd | Eurozone & Switzerland June CPI; global consumer confidence surveys |

| July 3rd | US June NFP & unemployment; ISM services; ECB meeting account; UK PMI/BoE credit survey |

| Mid-Week | ECB Forum at Sintra (Speeches by Powell, Lagarde, Bailey, Ueda) |

Aside from the day-to-day discussion of US policy the more important discussion is around trade. Little emphatic news flow is in place. Few trade agreements are in place. There are soundings that everything is agreed – we are just waiting the final agreements. The drop-dead date is the 9th of July, but agreements may take a little more time… nothing is for sure. The press is filled with confidence that agreements are in place but there is little that is completely agreed.

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

30th June 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB