By Falco

03 Mar 2025

• Recent economic data out of the US suggests a recession may not be too far away.

• Such an environment may certainly not warrant tariff increases.

• Slower growth with higher inflation will limit the scope for the Fed to react.

• More defensive equities needed in the US with a value bias.

• Bonds will be compromised by tariffs.

• It could well be Jerome Powell’s turn to sit on the “Zelensky chair”.

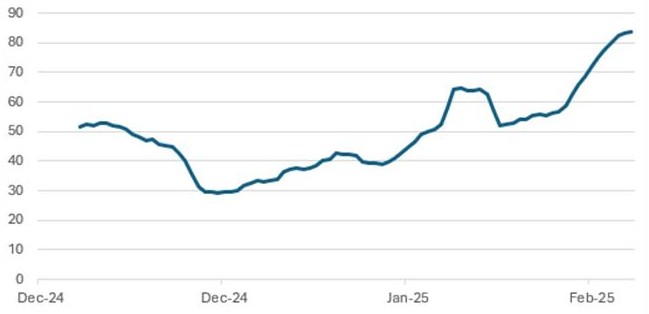

Disappointing economic data out of the US of late has set alarm bells ringing that a recession could be just round the corner. To add to the woes, the Atlanta Fed’s GDPNow forecast has dropped sharply, plunging deep into the negative territory at -1.48% from the 1.5% to 2.0% range seen over the past year (Chart 1). This deterioration suggests that current economic conditions are aligning with recession-like trends, adding to growing concerns about the broader growth outlook.

Chart 1: Atlanta Fed GDPNow GDP Forecast

Source: Bloomberg

In fact, Google search volumes for terms that included the word recession have picked up substantially of late versus where they stood at the end of 2024, suggesting building concerns about current economic conditions in the United States.

Chart 2: Google Searches for “Recession” in the United States

7-day moving average index

Source: Google

Recession or no Recession?

With recession concerns mounting, this week’s economic data assumes greater significance. The ISM Survey is expected to show a slight dip but remain above the key 50 level, signalling that the economy is still expanding. However, market attention will be laser-focused on the Prices Paid Index, as investors have become exceptionally sensitive to any signs of accelerating inflation amid slowing growth. Recent regional surveys, including the Philly Fed, Empire, and Kansas City Fed reports, have all shown substantial increases in the prices paid components, reinforcing inflationary concerns.

Later in the week, investors will scrutinise the February jobs report for signs of stabilisation in the economy. The market consensus expects job growth of 160,000 for the month, with unemployment holding steady at 4%. However, expectations of a slowdown in wage growth could influence market sentiment, particularly in the bond market and Federal Reserve policy expectations.

Where does value lie?

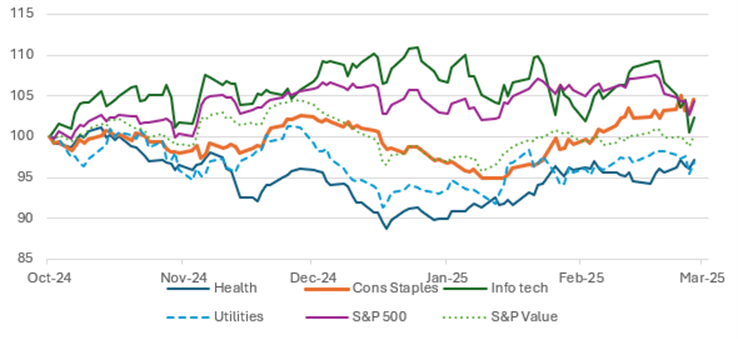

Amidst rising recessionary risks, investors have shifted their focus toward value stocks and defensive sectors. Consumer staples, utilities, and healthcare stocks—the traditional safe havens—have shown strength as concerns about an economic slowdown intensify. However, utilities and healthcare stocks have faced their own political headwinds, with the Trump administration’s policies creating uncertainty that has somewhat compromised their defensive appeal, although, in our view, these sectors should not be ignored.

In the meantime, stocks in the technology and media space have seen significant hedge fund outflows, with Goldman Sachs reporting that hedge funds exited US tech and media stocks at the fastest pace in six months during the two weeks to 21 February. This shift underscores a growing rotation out of high-growth sectors and into value-oriented, defensive plays in the current economic environment.

Chart 3: Value Plays to Outperform Tech if Recession Risk Persists

Source: Bloomberg

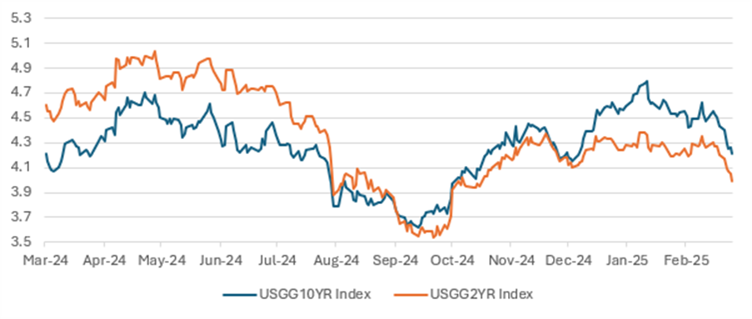

To date the US bond market has held up relatively well. In essence, there has been a bigger discounting of the feared slowdown in growth than any building inflation risk. The two-year and ten-year bonds have fallen in parallel, implying that the market would have the scope to save the economy through early interest rate cuts. At this point, we have our doubts that inflation will easily just drift lower. Remember we have yet to have any emphatic signal emerge that shows inflation is moving lower from recent sticky levels. Moreover, we still have to absorb the promised tariff increases, which, on most economists’ forecasts, would boost inflation by at least 30-40bps.

Chart 4: US 10-Year and 2-Year Drop in Parallel in Recent Weeks on Recession Risk

Source: Bloomberg

If President Trump goes ahead with his threat of new tariffs, it will further exacerbate inflationary risks. In the past few weeks, the president has issued several tariff threats targeting multiple regions:

European Union (EU):

• 25% Tariff Announcement: On 26 February 2025, Trump declared plans to impose a 25% tariff on goods imported from the European Union.

• Economic Impact: The Kiel Institute for the World Economy estimates that these tariffs could lead to a 0.4% contraction in the EU economy and a 0.17% reduction in US GDP.

Canada and Mexico:

• On 27 February 2025, Trump reaffirmed that the tariffs on Canada and Mexico would commence on 4 March, citing ongoing issues with drug trafficking and illegal immigration.

China:

• Trump also announced plans to impose an additional 10% tariff on Chinese imports starting 4 March 2025, citing China's role in the fentanyl trade as a primary concern.

• Chinese Response: China warned that it will retaliate against these increased tariffs, though specific countermeasures have yet to be detailed

Tariffs aren’t the magic cure to the current economic ills

A broad-based increase in tariffs is hardly the conventional approach to addressing an economic slowdown. If President Trump’s policies worsen a potential recession by fuelling inflation at a time of low or negative growth, he will have created a significant economic dilemma of his own making.

Trump could always summon the Fed Chair Jerome Powell to the "Zelensky chair" and have his deputy JD Vance apply some persuasive pressure—cameras rolling-to push for interest rate cuts!

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

3rd March 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB