By Falco

06 Jan 2025

As the new year begins, we try to answer two of the most pertinent questions that investors have fretted over in recent times: Will bonds prove supreme to cash and could markets outside of the US, such as China, offer better returns in 2025?

Will Cash Beat Bonds?

A great deal of consensus seems to have emerged among investors that potentially cash is not the investment to have exposure to as we move into 2025. This is not surprising considering the exceptional performance of US equities last year and increasing concerns that the Fed may not deliver as many rate cuts as expected.

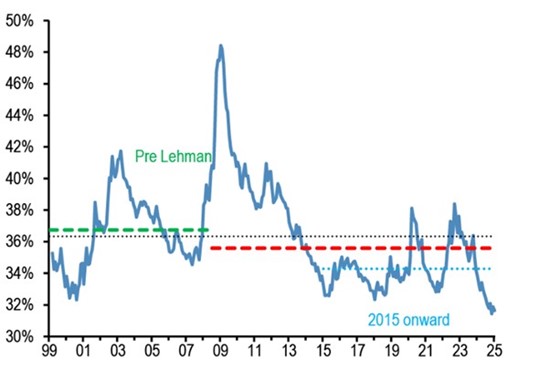

JP Morgan estimates that cash holdings of non-bank investors are at a historical low (Chart 1). Such a low allocation is at least in part because of the long-held assumption in 2024 that the Fed would cut interest rates along expected lines. However, since the start of Q4 2024, the market has shaved at least 100bps off those assumptions, indicating the central bank may not be as forthcoming on rate cuts this year.

Chart 1: Cash Holdings Very Low by Historical Standards

Global Cash held by non-bank investors as a % total holdings of Equities/Bonds/M2 of non-bank investor

Source: Bloomberg, JP Morgan

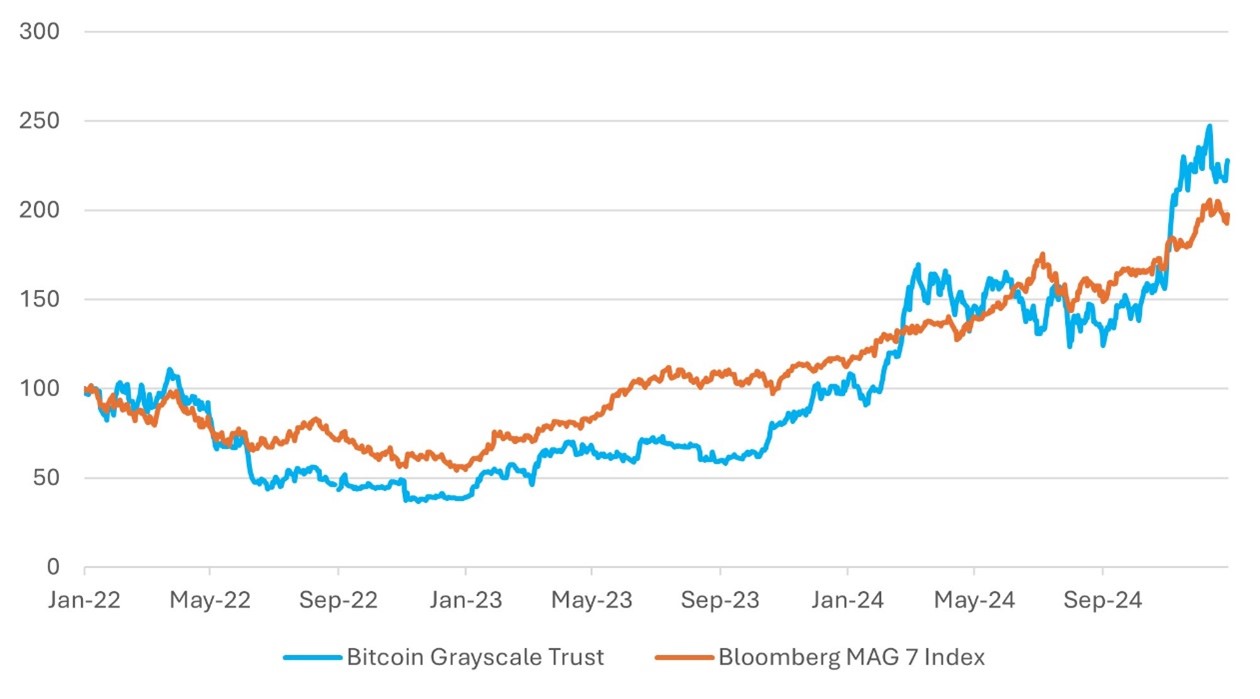

Another possible reason that analysts cite for the low cash allocation in holdings is investors pivoting to gold and crypto currencies as ‘safe’ assets, in a bid to diversify risk. Blackrock’s asset allocation experts recently suggested a 1-2% allocation to Bitcoin. However, the experts weren’t suggesting that Bitcoin should replace bonds; indeed, the risk-reward characteristics of Bitcoin are more akin to the Magnificent 7 rather than a safe asset.

Chart 2: Bitcoin More of a MAG 7 Replacement than Cash! Source: Bloomberg

Source: Bloomberg

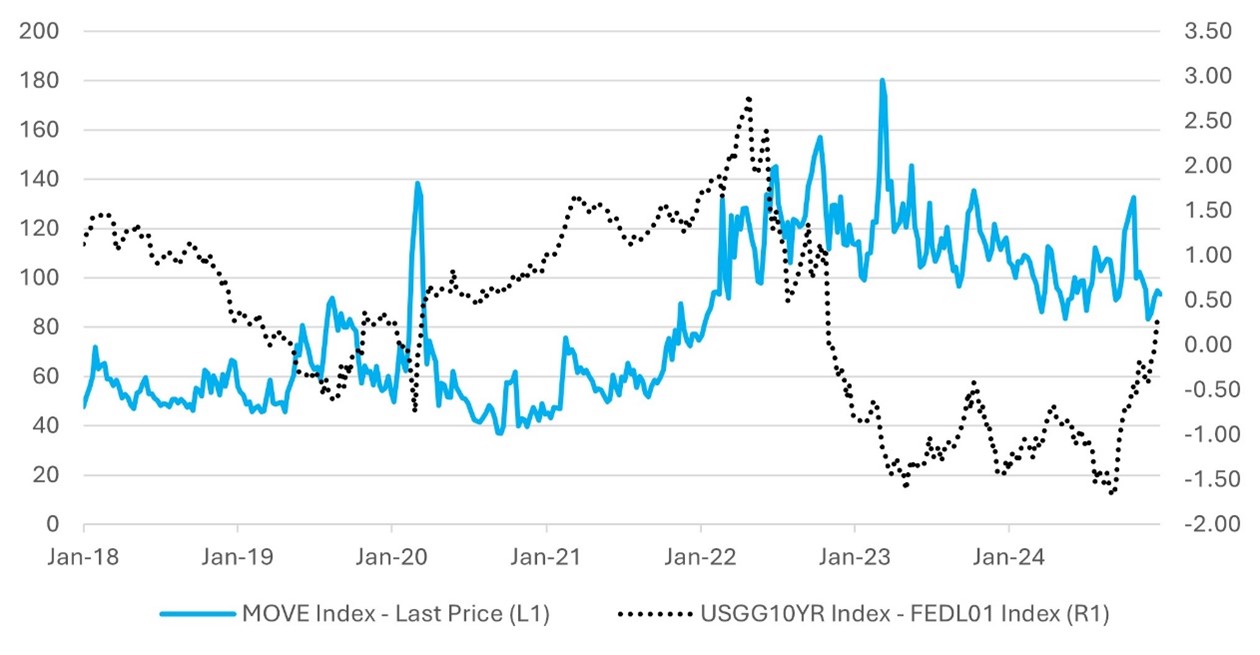

Currently, the US yield curve is quite flat with cash returns faring just 25bps below the US 10-year yield. The market only prices a further 25bps to 50bps of Fed rate cuts by the end of 2025. One would have expected more potential excess return for bonds considering that bond market volatility has remained elevated relative to 2018-22.

Chart 3: More Volatility in the Bond market not Compensated relative to Cas Source: Bloomberg

Source: Bloomberg

Could there be a Growth Surprise from Outside of the US?

As we begin the year, many investors remain optimistic about potential growth surprises in the US economy. President-elect Trump’s proposed policies, particularly tax cuts, are seen as skewing growth risks to the upside. However, these expectations have been widely discussed and debated. With economist forecasts remaining subdued, there may be potential for positive surprises from Europe and China.

In the case of France and Germany, their struggles with politically driven, growth-stifling conflicts are well documented. However, as 2024 concluded, there were signs of a broader push for greater flexibility on fiscal austerity. This shift could pave the way for more growth-oriented policies taking shape in the first quarter. In France, the newly appointed Economy Minister, Eric Lombard, is expected to propose a 2025 budget that departs from strict austerity measures. Such an approach could help restore confidence in the economy, encouraging households—who hold substantial savings—to increase spending.

China’s Economy: Far from a Disaster, Despite the Noise

Although recent headlines have appeared to suggest China's economy is in dire straits, a careful analysis paints a clearer picture. Last week, Premier Xi Jinping expressed confidence that China’s GDP growth will likely hit its 5.0% target for the year. While private-sector forecasts at close to 3.0% are more conservative, there’s no denying that certain sectors in China are thriving.

Dynamic Growth in Green Energy, Technology, and Quantum Research

China remains a global leader in green energy and environmental initiatives. The country is also making significant strides in technology and innovation, investing heavily in semiconductors, artificial intelligence, robotics, and quantum research. These efforts could position China as a leader in emerging technologies.

Fiscal Stimulus: A Question of When, Not If

Given the current state of affairs, for China to make a significant impact on global markets, fiscal stimulus will likely be necessary. Market expectations suggest a rise in the budget deficit to 4% of GDP in 2025, up from 3% in 2024. While the country is taking specific measures, their scope may depend on the economic impact of external factors such as rising tariffs.

Major Stimulus Measures in the Works

China Outlook

China’s strategic investments and forthcoming fiscal measures underscore the government’s commitment to sustaining economic momentum. While uncertainties remain, particularly regarding the external trade environment, the long-term potential of China’s economy remains robust, bolstered by its dynamic growth sectors and focus on innovation.

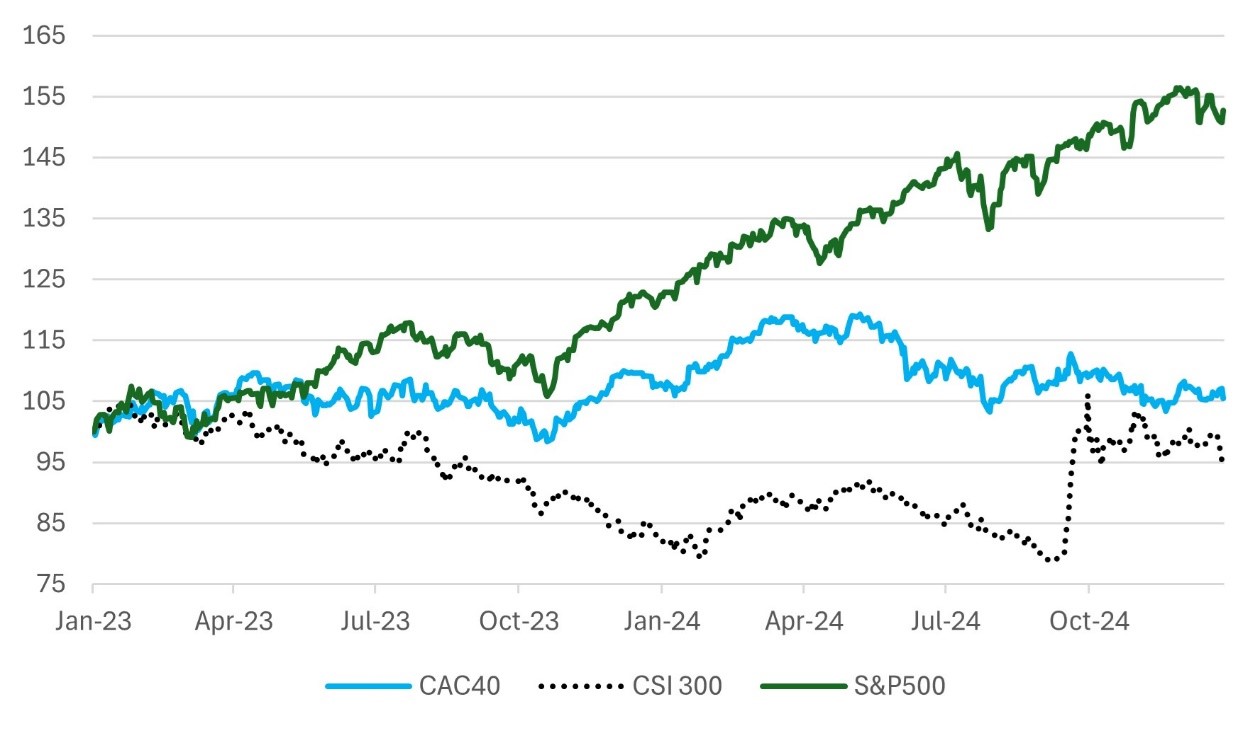

Chart 4: French CAC40, China’s CSI 300 Index and the S&P50 Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

6th January 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB