By Falco

10 Feb 2025

• Market Uncertainty Rises Amid US Policy Shifts – Disruptive policymaking in the US continues to keep investors on edge.

• Consumer Confidence Wanes Amid Inflation Concerns – US consumers fret about near-term inflation worries persist.

• Tech Stocks Face Pressure – High valuations and mixed quarterly earnings outlooks weigh on US technology stocks.

• European Rate Cuts Fuel Market Optimism – Interest rate cuts in Europe have driven strong YTD returns, with potential for further easing.

• Key Events Ahead: Tariffs & Inflation Data – Keep an eye on the next phase of US tariffs and the upcoming inflation report.

• India’s RBI Rate Cut May Revive Equities

Market Sentiment Shifts as Trump Returns to Office

Market sentiment was largely optimistic when President Trump assumed office in January. In particular, analysts pointed to the potential for stronger economic growth, fuelled by renewed business confidence and expectations of significant deregulation. While concerns about tariffs and their impact on inflation lingered, investors largely embraced Trump’s "Make America Great Again" vision. As a result, global investors remained glued to the US markets, with a particular focus on technology stocks and sectors such as banking and consumer goods.

However, one month into the new presidency, that optimism is beginning to shift. President Trump appears to be leaning toward policies outlined in Project 2025—a policy agenda that he previously downplayed, but one that calls for a radical reset of US government administration. Meanwhile, the work of Elon Musk and his DOGE initiative in government affairs has upended some arms of the government and increasingly unsettled markets.

President Trump is Losing the Consumer

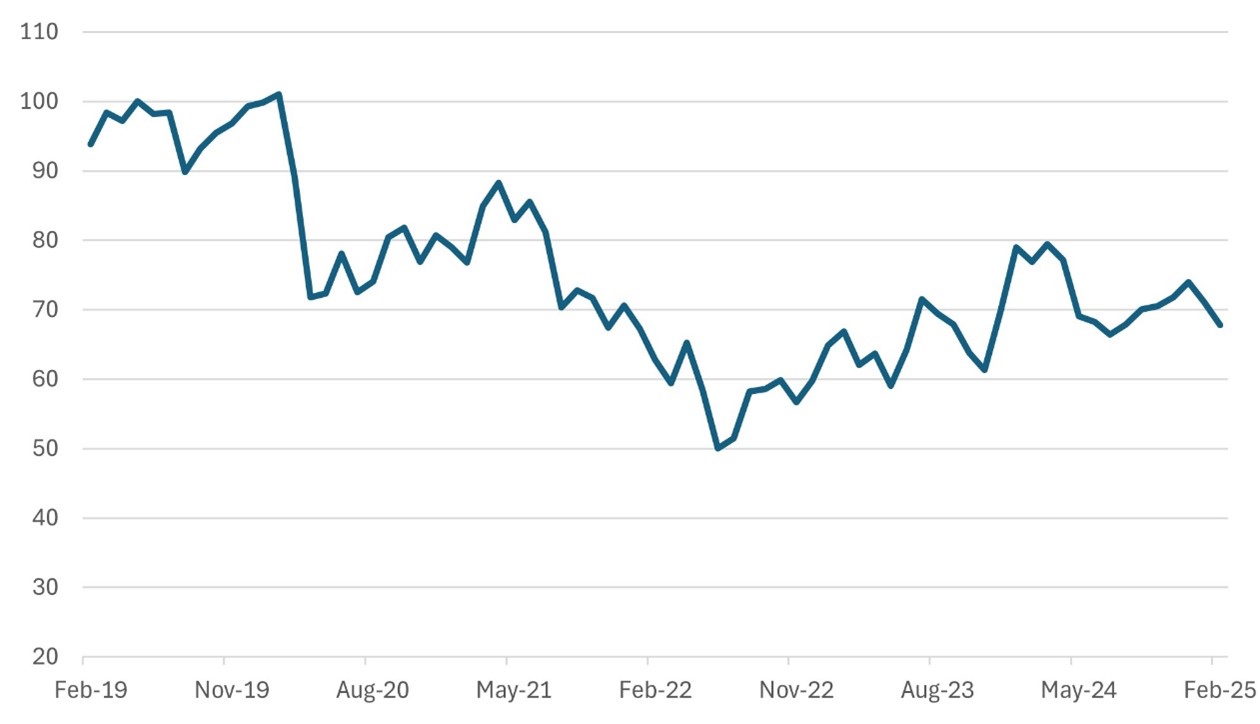

The actions of the president are not only further unsettling the markets but also failing to address the key concerns of householders. The latest University of Michigan Consumer Confidence survey, for instance, shows a sharp decline in consumer sentiment. Against market expectations of a reading of 71.8, the survey came in at 67.8. Consumer confidence has clearly taken a hit. Ironically, one of Trump’s central campaign promises was to combat inflation and restore consumers’ spending power. Yet, instead of easing financial pressures on middle- and lower-income households, his current policy making – or the lack of it – could well be exacerbating the problems.

Chart 1: US Consumer Confidence Survey Dips

University of Michigan consumer sentiment index Source: Bloomberg

Source: Bloomberg

While the survey revealed a significant drop in consumer confidence, inflation expectations rose sharply. Consumers now anticipate a 4.3% inflation rate over the next year, sharply up from 3.3% recorded in the previous month’s survey. This shift underscores growing concerns about purchasing power and economic stability—factors that could shape both investor behaviour and broader market trends in the months ahead.

The Revolving Door on Tariffs

Markets experienced a shaky start to the week as the president unexpectedly imposed significant tariffs on Canada and Mexico. However, to everyone’s relief, he temporarily reversed course after both the neighbours agreed to bolster their border security measures. The respite, however, was short-lived. By the week’s end, tariff-related tensions resurfaced, with the president reintroducing "reciprocal tariffs"—essentially raising US tariffs to match those historically imposed on American goods. The back-and-forth has fuelled uncertainty, making it seem as though trade policies are being crafted on the fly.

Day Traders Don’t Trust It

A recent JP Morgan survey found that 51% of traders now cite tariffs and inflation as the biggest market risks, up from just 27% a year ago when inflation alone dominated concerns. President Trump’s trade policies are not only amplifying existing market volatility but also adding another layer of unpredictability to it.

The conventional wisdom in times of volatility is to focus on fundamentals and ignore short-term noise. But that’s easier said than done. Legal analysts suggest that many of Trump’s proposals – including tariffs – could face significant legal challenges. During Trump’s first term, his administration won just 22% of its court cases, the lowest success rate of any modern president. However, legal battles can take years to resolve, and some within Trump’s inner circle have hinted at an even more disruptive approach: leveraging the US Supreme Court’s recent ruling on presidential immunity to simply disregard judicial pushback.

For traders and investors, this evolving legal and political landscape could mean just one thing—increased volatility going forward.

Getting Back to Fundamentals

US Inflation is Still Sticky and Rates are Unlikely to Decline Anytime Soon. This week’s US inflation report is expected to confirm that inflation remains persistently high, exceeding the Federal Reserve’s comfort level. The headline inflation rate is projected to rise to 3% from the previous 2.8%. While US 10-year bond yields have edged lower, they remain range-bound, reflecting uncertainty among fixed-income investors about the direction of long-term rates. Barring an unexpected downside surprise in inflation—which seems highly unlikely—holding positions remains the prudent strategy.

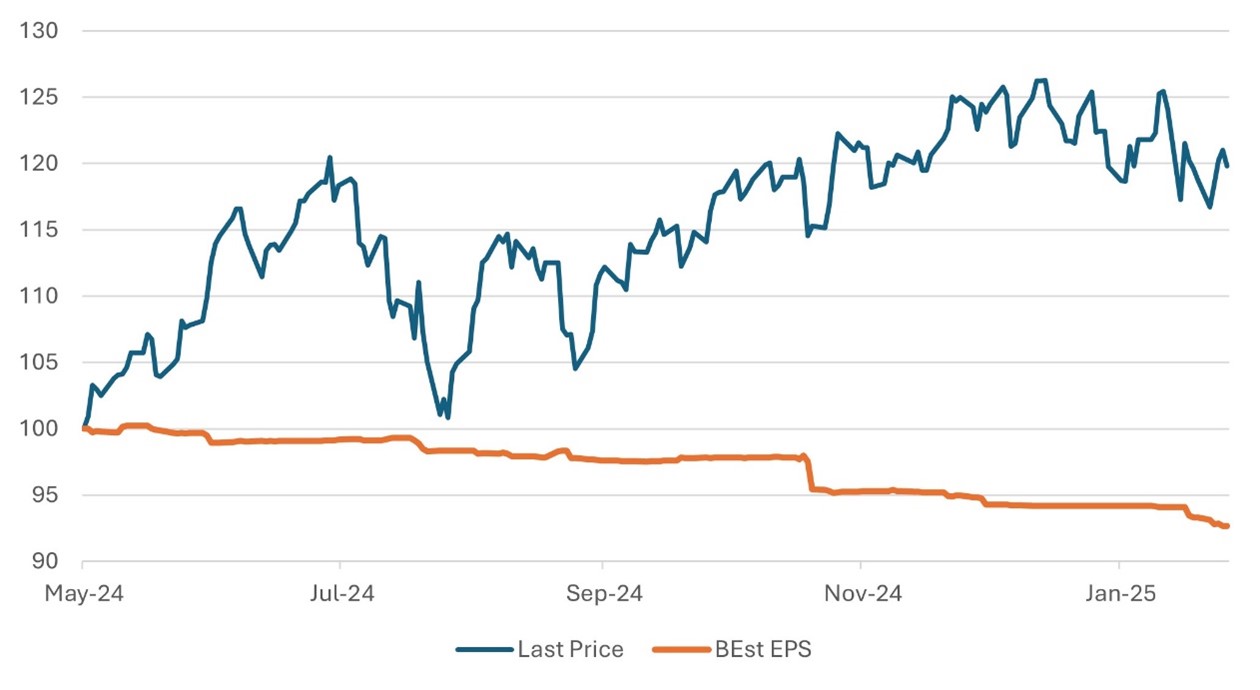

Domestic politics and the high valuation of the market are likely weighing on US equities. The US tech sector appears stagnant. The DeepSeek saga has only fuelled investor uncertainty, making them hesitant to chase tech stocks further. The recent quarterly earnings season has presented a mixed picture, with quite a few companies underperforming expectations. Notably, investor concerns stem more from disappointing forward guidance than from the latest quarterly numbers themselves.

Chart 2: US Tech Sector Earnings Surprise to the Downside Again this Quarter

MSCI US IT Sector Index and Consensus earnings expectations rebases to May 2024=100 Source: Bloomberg

Source: Bloomberg

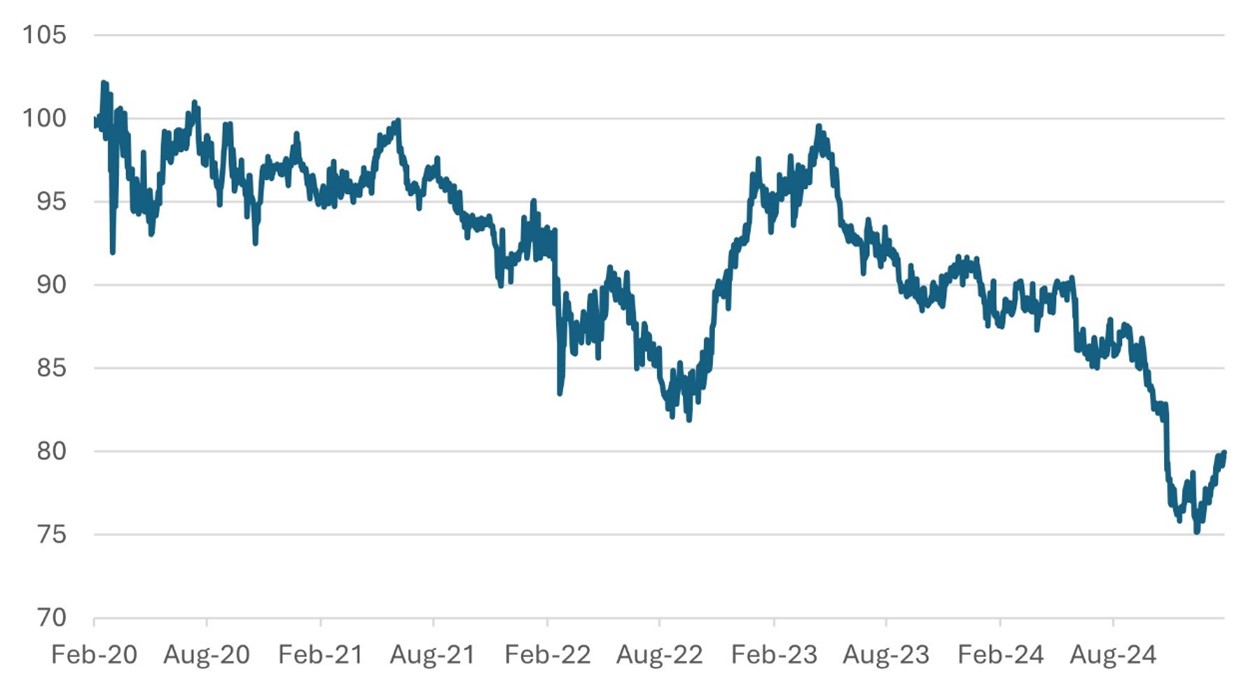

European Equities Gain on Lower Inflation and Rate Cut Prospects

In contrast, Europe’s inflation outlook appears more in control, trending closer to the European Central Bank’s 2% target. Economic activity in the region has shown slight improvement, boosting investor confidence. This optimism has contributed to a strong 7%+ rebound in European equities since the start of the year, significantly outperforming the US market.

Chart 3: Europe ex-UK Equities Outperform from a Low Base

MSCI Europe ex UK relative to MSCI World net TR Source: Bloomberg

Source: Bloomberg

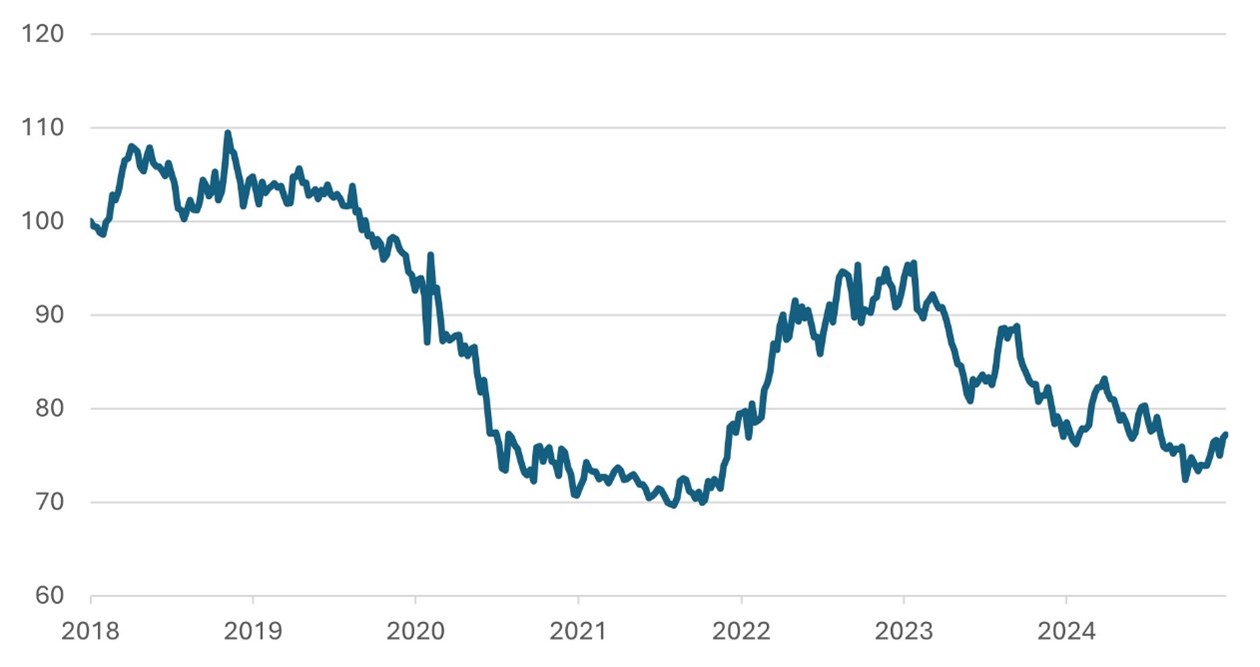

Accelerated UK Rate Cuts Would Provide the Best Antidote to Sluggish Growth

The UK economy, struggling with sluggish growth, is benefiting from interest rate cuts and expectations of further reductions in May. The interplay between interest rates, mortgage rates, and the real estate market is beginning to generate positive momentum in the equity market. While the Bank of England has halved its growth forecast to just 0.75%, the possibility of accelerated rate cuts could provide much-needed support to the housing market and extend the ongoing recovery in UK equities.

Chart 4: UK Equities Rebound and May Have Further Relative Upside

MSCI UK Equities Relative to MSCI World ex UK (net TR) Source: Bloomberg

Source: Bloomberg

Asia – Waiting and Watching

Asian markets remain in a wait-and-watch mode amid mixed signals from the US and China. Following the Chinese New Year, concerns over potential US tariffs have eased slightly, as they have not yet reached the feared 60% level. However, economic confidence data remains mixed, and there are no strong catalysts to drive investors back into Chinese equities—other than their continued relative cheapness.

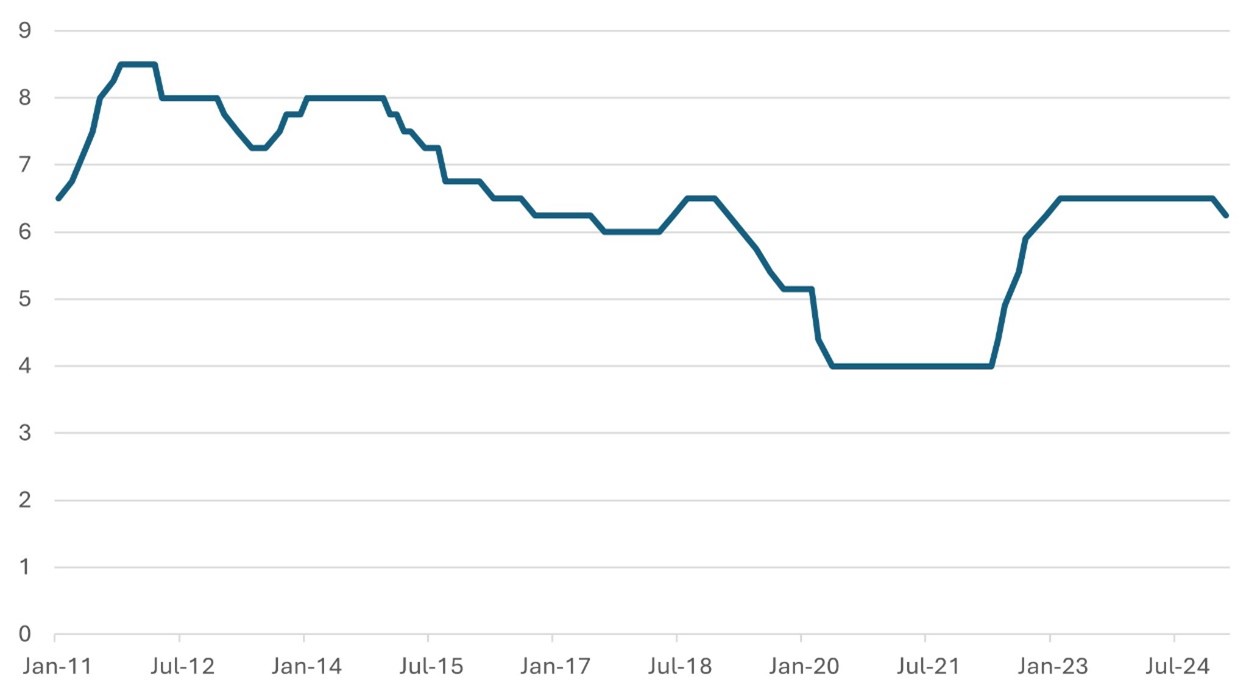

In India, the key question is whether the economy and its equity market can regain momentum following recent underperformance. Like other regions, India’s central bank has stepped in to provide support. With the US dollar’s strength fading somewhat of late and inflation expected to behave, the Reserve Bank of India took the opportunity to cut interest rates by 25 basis points. It was the first cut in rates since June 2020. Market participants anticipate further rate cuts in upcoming meetings, which could help revive economic activity that has slowed down notably over the past six months.

Chart 5: Reserve Bank of India Cuts Rates for First Time Since 2020

RBI Policy Rate (%) Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

10th February 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB