By Falco

10 Mar 2025

• President Trump’s erratic policymaking is taking its toll on growth and markets

• It is difficult to see logic in Trump’s tariff actions, which can only increase inflation

• Therefore, there is logic in investors switching portfolio allocation to non-US markets

• There is logic also in worrying about higher inflation and growth, which should keep US 10-year yields rangebound

• The resulting drop in the USD could be a harbinger of what is to come; we prefer EUR

• As we have frequently argued, the perception of US market exceptionalism may be overstated

The Illogical US Economic Policymaking

We remain deeply sceptical of commentators who attempt to impose logic on what is, quite frankly, illogical economic policy making in the US. According to these commentators, it is as if we are entering a new era of rational decision-making, if only that were true. If logic and consistency truly guided policy, then one would expect the US president to implement economic policies and stick to them. Yet, if tariffs are merely a negotiating tool, investors are left wondering: what exactly is being negotiated when there is so much back and forth?

The latest round of tariff announcements underscore this uncertainty. Newly announced 25% tariffs on Canadian and Mexican imports, alongside a 20% hike in tariffs on Chinese goods, now affect $1.3 trillion in trade. Markets, already rattled by the administration’s erratic stance on trade policy, are struggling to assess the long-term implications. The US government, to defend its actions, has argued that short-term market volatility is an acceptable trade-off for – what it considers – long-term restructuring. Treasury Secretary Scott Bessent recently stated that these disruptions are part of a broader strategic realignment—but investors remain unconvinced.

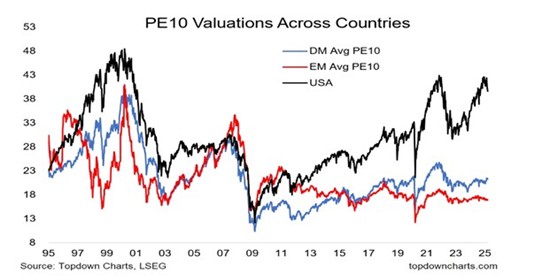

Logical Outperformance of EAFE versus the US

Given the current uncertainty, there is clear market logic behind the recent outperformance of global equities vis-à-vis the US market. The valuation premium of US equities over the rest of the world (Europe, Australasia, and the Far East, or EAFE) remains near historic highs, yet, the perception of US market exceptionalism may be overstated.

Chart 1: Shiller PE valuations highlight the extreme valuation premium of U.S. equities

Source: Bloomberg

The recent outperformance of European and Asian equity markets relative to the US may continue. A period of outperformance is only just starting to reverse years of underperformance.

Chart 2: MSCI EAFE Index net Total Return Index Relative to the US Source: Bloomberg

Source: Bloomberg

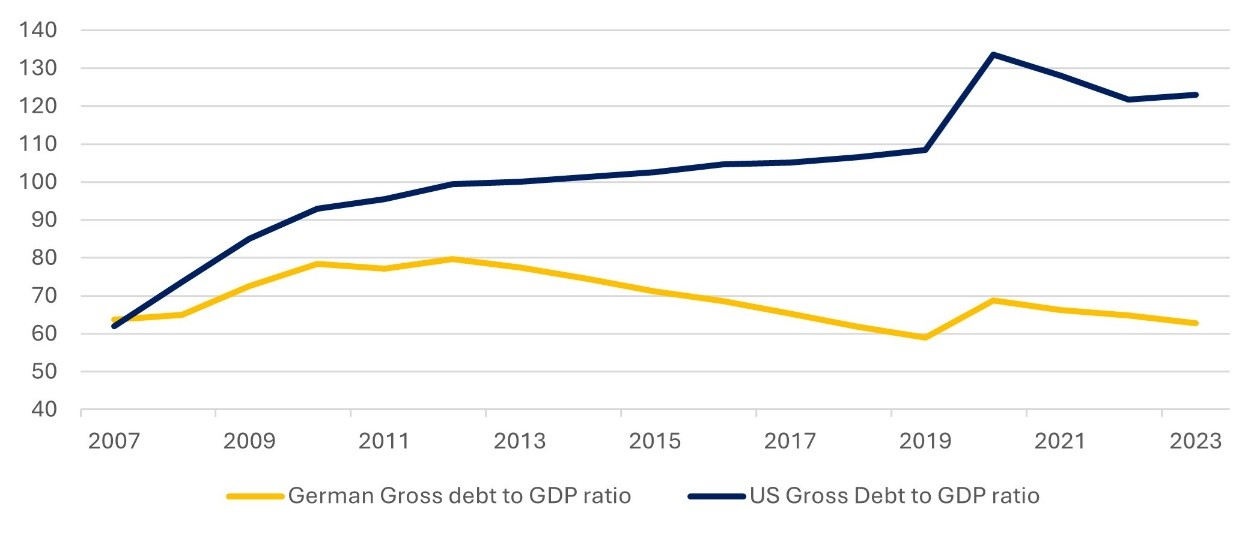

A key driver of this outperformance is the improving relative fundamentals of markets outside of the US. Take Europe, for instance, where Germany, among other nations in the continent, is significantly increasing its defence budget, signalling greater fiscal flexibility and a willingness to recalibrate but not exaggerate debt-to-GDP ratios.

For years, the US economic growth has been artificially propped up by ever-increasing debt. It is akin to a neighbour flaunting a new sports car and an expensive vacation—only to be exposed later that both were purchased on credit. Would you consider them truly wealthy, or merely living beyond their means? The numbers tell the real story: Germany’s debt-to-GDP ratio stands at 63%, while the US’ has reached an unsustainable 120%.

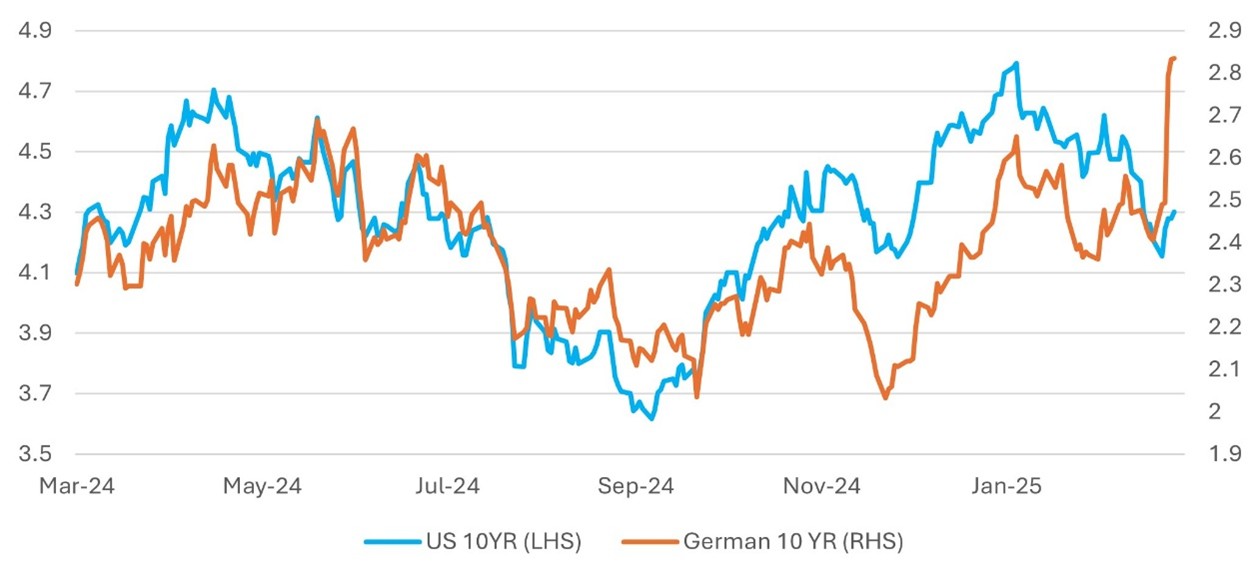

It’s Germany’s turn now to use the credit card. The likely German coalition that will run the next government announced a proposal that includes a €500 billion special fund dedicated to infrastructure projects and the removal of caps on defence spending, potentially leading to more than €1 trillion in additional borrowings over the next decade. While defence spending in 2024 has been around 2.1% of GDP, the coalition is proposing a further hike in defence budget to 3%. The 42bps increase in the German 10-year government bond yield reflects the markets’ sharp change in perception of the future.

Chart 3: US government Debt at Almost Double the Ratio of German debt-relative-to-GDP

(%) Source: Bloomberg

Source: Bloomberg

In Japan, the economy is normalising (although under the burden of domestically owned government debt) and the corporate sector is radically pushing ahead with restructurings. Half of the major Japanese companies are in a net cash position, which implies an opportunity to increase dividends or buy back shares. In China, the government has a technological and cost advantage over many of its competitors in key growth industries. Moreover, it is the second-largest economy in the world (18% of global GDP) with a very modest weight (2.9%) in global equity market indices. China’s debt-to-GDP ratio is around 88%, well below that of the US.

A Logical Pricing of Recession and Inflation Risk in the US and German Bond Markets

It is tough to gauge where the US 10-year government bond yields will settle given the current drama in the US economy and geopolitics. We try to piece together the jigsaw puzzle.

1. Spending Cuts Remain Elusive – Despite the political noise, meaningful cuts to US government spending seem unlikely in the near term. Last week’s pushback in the president’s cabinet meeting against proposed staff cuts underscores how politics often stands in the way of aggressive cost reductions. This week is also critical for keeping the US government open with another extension vote due.

2. There’s no Getting Away From Tariffs, i.e., we are staring at higher inflation – The latest independent estimates suggest that US inflation could rise by 30-5bps in 2025. This week sees the release of the February inflation report with the consensus expectations for a small drop to 2.9%. It’s far too early to expect to see any impact from (higher) tariffs.

3. Rate Cut Expectations vs. Labour Market Resilience – The bond market remains more focused on recession risks and is already pricing in a 25-basis-point rate cut from the Fed this summer. However, conventional wisdom suggests that the Fed typically avoids cutting rates unless the unemployment rate rises above the 4.5%-5.0% range. With February’s unemployment rate still at 4.0%, the labour market remains resilient, potentially complicating any rate cut decision.

4. Mixed Economic Signals – US economic data remains weak overall. The Atlanta Fed’s GDP tracker currently sits at -2.4%, down from a recent low of -2.8%. The manufacturing sector continues to struggle under the weight of policy uncertainty, while the service sector is expanding. Both, however, indicate persistent inflationary pressures.

Chart 4: US 10 Year Yield plotted against German 10 Year Yields Source: Bloomberg

Source: Bloomberg

Investors are drawn between pricing a recession and a spike in inflation with the current US 10-year yield about right in the very near term. The drop in the US 10-year yield January onwards until very recently reflects the policy mayhem and the consequent drop in US economic activity. The market went from expecting a vibrant start to the year to seeing data that suggested a recession was at hand. In just the last week, we have seen the market increasingly getting concerned about the impact of tariffs on inflation. Hence, we have a bias to the shorter duration, which is more concentrated around the 2-year area of the curve. We suspect this week’s inflation has a bias to being above expectations given the strong showing of inflation in the industrial surveys.

Chart 5: Market Expectations for the Number of Fed Funds Rate Cuts by the end-of-the-year Source: Bloomberg

Source: Bloomberg

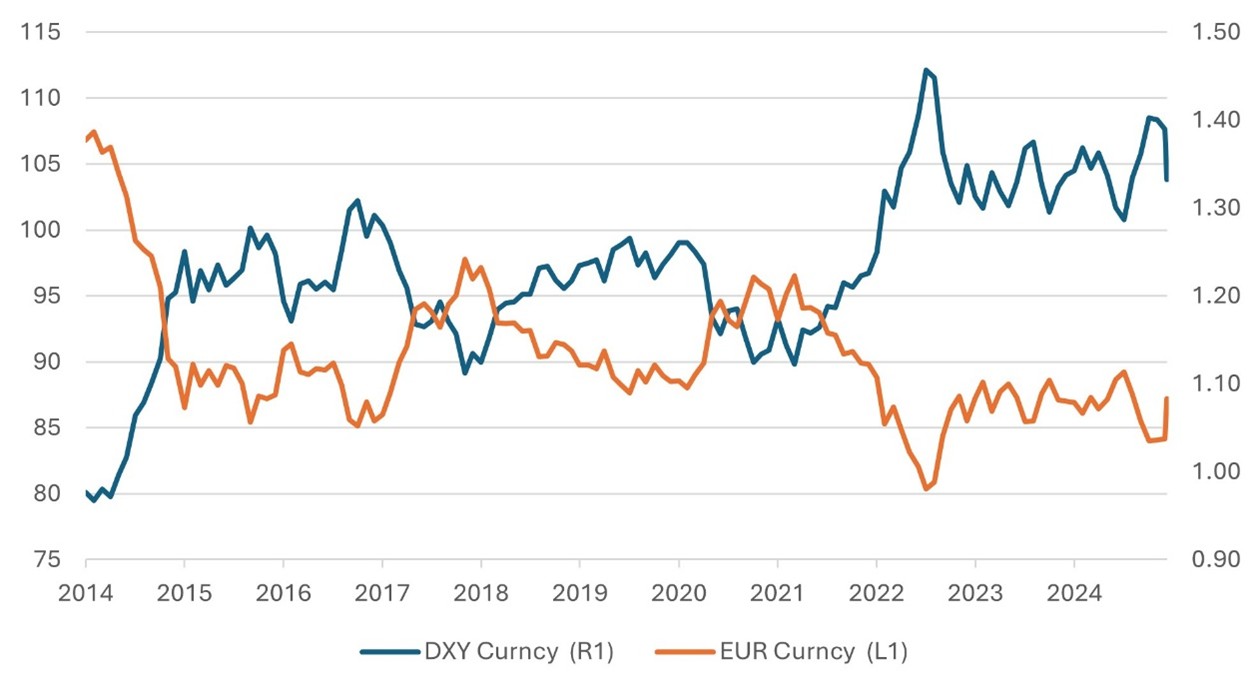

The Logical Drop in the Dollar... With More Likely to Come

As forward expectations for interest rates have dropped, we have logically seen the drop in the value of the dollar. However, we believe there is more to this value decline – for instance, there is a genuine concern in global markets about the direction of US economic policy making. It feels like “the Emperor has no clothes” moment when the market strips away the last vestiges of US exceptionalism.

Chart 6: US Dollar at Risk of a Further 10% Dro Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

10th March 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB