By Falco

13 Jan 2025

What will the global financial markets be like this year? Where does value lie? Will the incoming US administration’s policies cause an upheaval? Will Emerging Markets again rise to the occasion and pull global growth forward? Those are the many questions that investors will have on mind this year as they traverse these times. While we acknowledge that finding a definitive answer to any of those questions will not be easy, this week we have attempted to carefully weigh the options value-seeking investors have at their disposal.

1. The Year of Reckoning for Government Debt?

The financial markets are growing increasingly sensitive to the challenges posed by mounting government indebtedness. While the initial sell-off in US government debt was driven by stubborn inflation and the Federal Reserve’s reluctance to cut interest rates as aggressively as investors had hoped, the current sell-off – and the resulting rise in yields – now seems to reflect growing concerns about the sustainability of government debt and its servicing costs.

According to the Congressional Budget Office, US government debt levels are surging at an alarming rate. Despite this, the incoming president plans to implement tax cuts, banking on the hope that the cuts will spur economic growth, and, over time, help reduce the deficit. However, this approach carries significant risks of distorting the inflation environment.

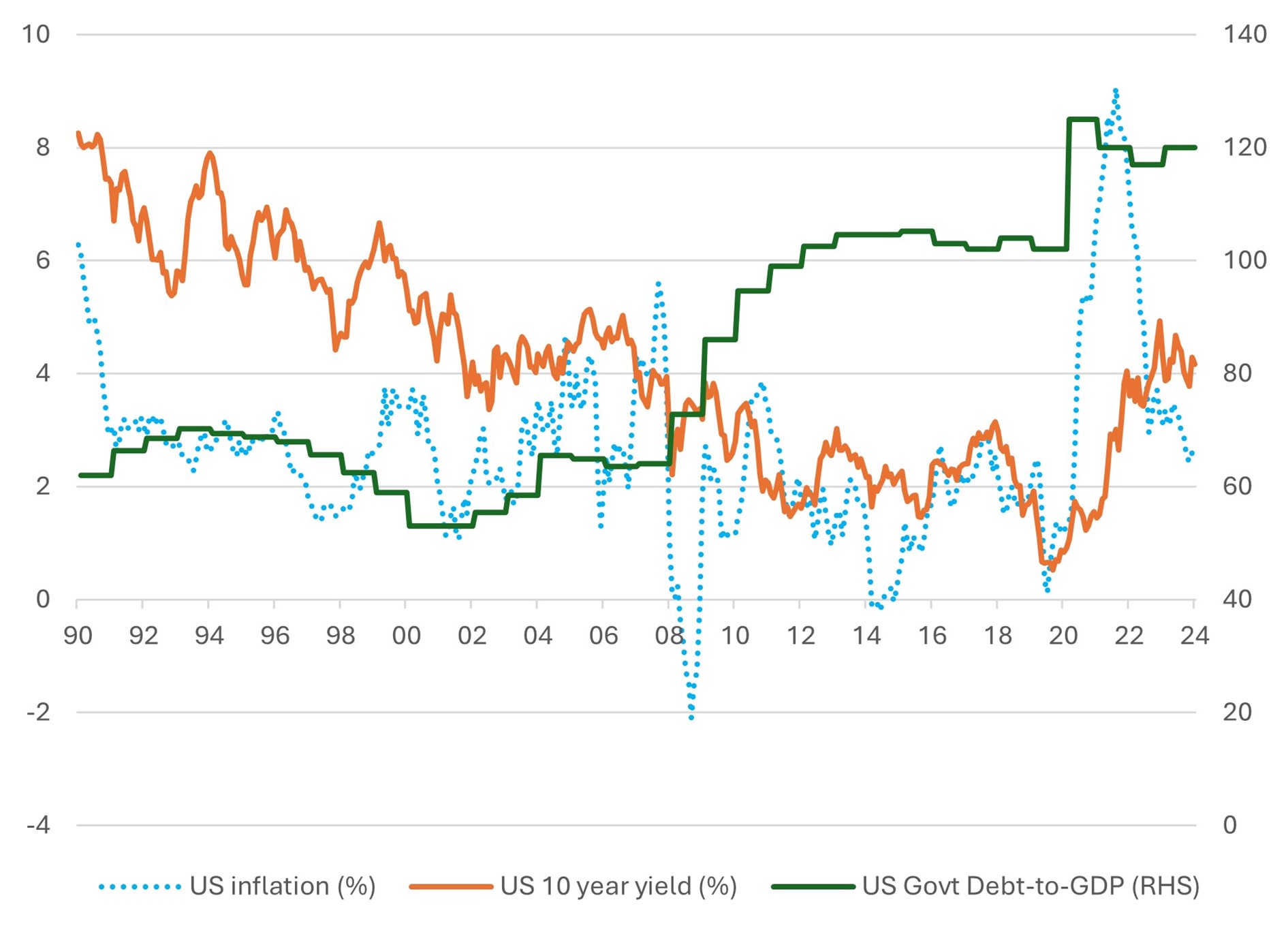

We would like to remind investors here that in the 1990s, when US inflation averaged around 2.7%, the 10-year Treasury yield reached as high as 6%. At that time, the US government debt-to-GDP ratio was only half of what it is today. Now, the US faces an undesirable combination of persistently high inflation and record levels of government debt, highlighting the challenges ahead for both policymakers and markets.

Chart 1: Spike in US 10-Year Yields Justified by Government Indebtedness and Inflation Source: Bloomberg

Source: Bloomberg

In Europe, attempts to cut deficits have led to the fall of governments and caused political turmoil in France and Germany, two of the important EU constituents. To further complicate matters, the UK is facing a crisis of confidence in the gilt market.

The experience of the UK in the past few weeks has shown what can happen when the market loses confidence in the government’s ability to rein in indebtedness. Since the last budget, the UK 10-year gilt yield has risen 50bps, which, if maintained, will increase the interest burden on government funding and affect the real estate market through higher mortgage rates.

2. A Year of Disruption?

President-elect Donald Trump has a pending list of one hundred executive orders that he intends to implement after his inauguration next Monday. Political analysts expect these orders to address Trump’s key pre-election promises such as immigration, energy policy, trade, and federal governance.

Legal Challenges: Legal experts expect many of these executive actions, particularly those concerning immigration and federal workforce restructuring to face immediate legal challenges, potentially delaying their implementation.

Economic Impact: The proposed tariffs could lead to increased consumer prices and potential trade wars, affecting both domestic and international markets. Mass deportations may result in labour shortages in industries reliant on undocumented workers, further affecting the economy.

3. The Tech Sector Needs a Supply of Positive Surprises

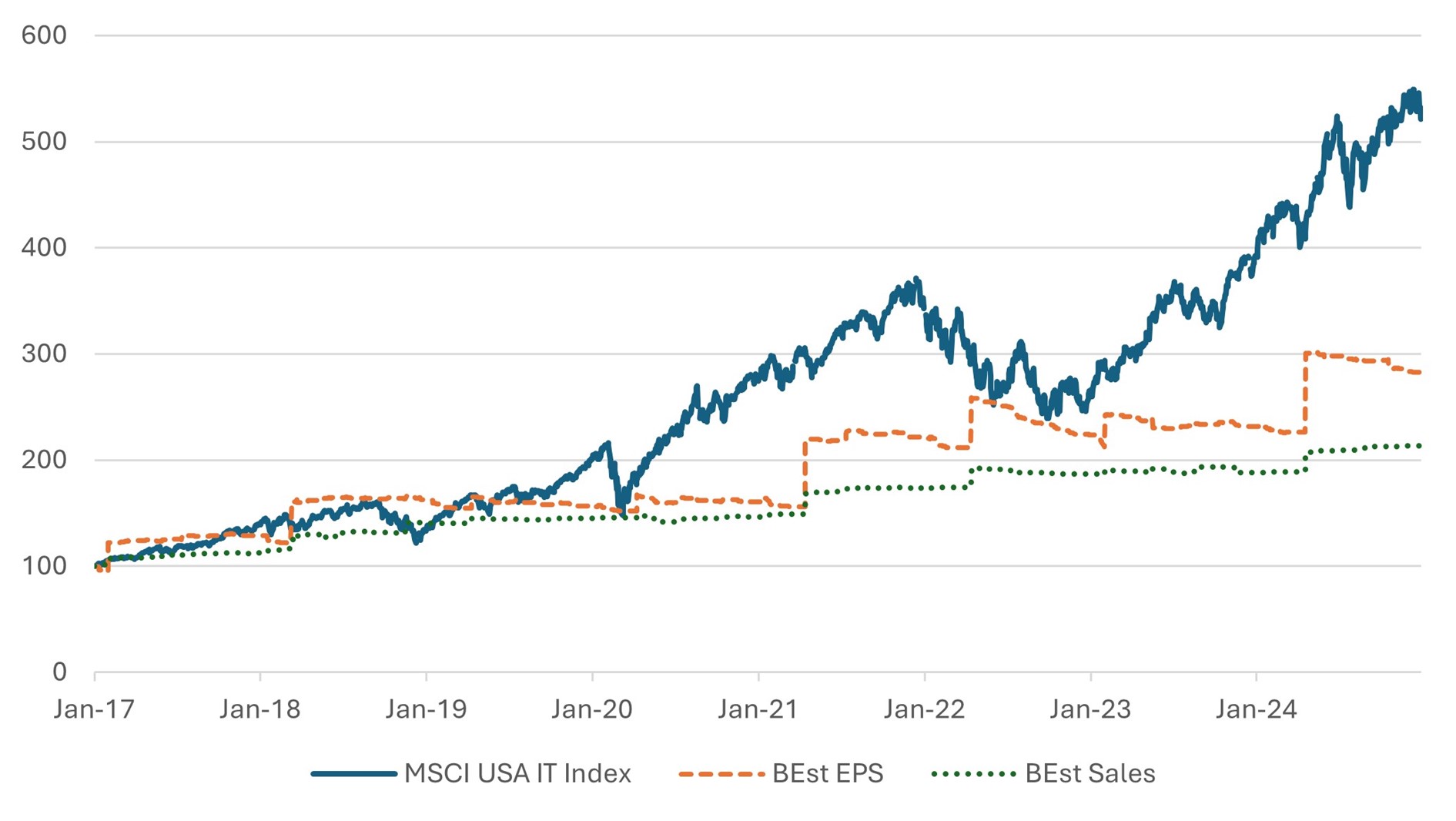

The tech-heavy NASDAQ index has struggled to gain momentum so far this year. While we firmly believe the technology sector will remain a crucial driver of long-term equity market returns, the index’s upside potential is limited without a meaningful revenue or profit growth.

The tech sector appears to be overly relying on Nvidia to deliver positive surprises. Over the next two years, analysts project Nvidia's revenues to grow at an impressive 100% annually. However, the broader picture is less optimistic, with the aggregate revenue growth of the MAG7—which accounts for the bulk of the sector’s earnings—forecast at just 15% annually. For comparison, Apple’s average revenue growth over the same period is expected to be a modest 7%.

Chart 2: MSCI US IT Sector, Price Index Significantly Outpaces Earnings and Revenue

Source: Bloomberg

Part of the problem has been the paucity of positive surprises. Even comments from the Nvidia CEO last week noting potential decades of wait before quantum computing becomes mainstream were sobering. The comments led to an $8bn drop in the value of quantum computing stocks that had so far been running hot. However, to put that sell-off into some kind of context, even though a stock like Rigetti Computing Inc (RGTI) halved in value, it is still up a staggering 775% over the past year!

4. The High Valuation of the US Equity Market is not a Problem until it is a Problem

The US market, with its elevated valuations, appears vulnerable unless the newly elected president can instil confidence in a steady stream of positive developments in the coming months. While the renewal of tax cuts could provide hope for spurring additional economic growth, bond market participants—often referred to as "bond vigilantes"—remain cautious. They worry that such cuts may worsen the national debt and push long-term interest rates higher.

In the initial euphoria following the election results in early November, the yield on the 10-year US Treasury was 4.30%; today, it hovers closer to 4.80%. Any proposed tax cuts are likely to face delays, as the president will need to negotiate with Congress on the specifics. While deregulation could offer targeted support to certain sectors, it is unlikely to ignite a broad market rally.

Although Trump may attempt to promote a positive narrative, persistent concerns in the bond market could weigh on equities. Given the forward price-to-earnings multiple of 24.6x, the US equity market appears increasingly susceptible to profit-taking if investor sentiment deteriorates further.

5. Asia and the Emerging Markets Remain the Great Hope for 2025 Positive Surprises

With the US and European markets grappling with government debt challenges, medium-term hopes for strong returns are increasingly focused on emerging markets. Indian equities ended 2024 with solid, though not stellar, returns, while Chinese equities posted double-digit gains amid a backdrop of high volatility and erratic macroeconomic performance.

We are optimistic about a potential resurgence in both Japan and China in 2025 and, expect the Indian economy to regain momentum after a brief pause. Latin America could also surprise to the upside, particularly if the region’s commodity markets recover and drive growth.

Emerging Markets may contribute the majority of global GDP growth over the next decade, and their financial markets are well-positioned to deliver increasing returns as they continue to mature and attract global capital.

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

13th January 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB