By Falco

14 Apr 2025

Due to the breadth of issues in the markets at present, we are sending out two weeklies this week, the first on the immediate challenges and the second on the potential silver lining for the markets.

The past week has seen President Trump's tariff regime undergo significant shifts, leaving the markets to digest the implications of the moves and the broader consequences for US assets.

Liberation Day (April 2) saw the US administration announce a universal 10% tariff on all imports, alongside higher "reciprocal" tariffs for 57 countries, with the most aggressive being a 145% effective tariff on Chinese imports. This move was designed as a strategic escalation, but it also placed immense pressure on global markets.

Tariff Pause (April 9) came after mounting backlash, with the administration halting the increased tariffs for 90 days for most countries, excluding China. This pause provided temporary relief to the markets, but the ongoing uncertainty surrounding future trade policies remains a cloud over market sentiment.

Tech Sector Exemptions (April 12) were another adjustment, as the administration exempted certain electronics, such as smartphones and computers, from the new tariffs. These products, however, remain subject to a 20% tariff specifically targeting Chinese imports. The irony is not lost on market participants: just days earlier, US Commerce Secretary Wilbur Ross had stated that the purpose of tariffs was to bring iPhone production back to the US, a goal seemingly undercut by the exemptions.

While this past weekends backslide by the administration will likely bring further relief in the short term, market volatility remains a significant issue. Tariff uncertainty continues to overshadow economic forecasts, with many companies retracting earnings guidance as they try to grasp the longer-term implications of tariffs on profitability.

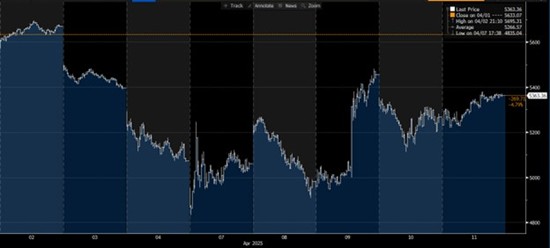

Chart 1: S&P 500 Rebounds to -5% Since “Liberation Day”

Source: Bloomberg

Chart 2: US 10-year Intraday Rises 60bps as Inflation Becomes More Important Than Recession

Source: Bloomberg

The knee-jerk market optimism following the latest tariff pause may be short-lived. The destruction of trust in US policy has the potential to leave a long-lasting legacy of de-rating US assets. After all, the Trump administration has a long way to go, and the market’s renewed volatility suggests that the full ramifications of these tariff policies may not yet be fully realised.

The End of US Exceptionalism

The challenges of recent weeks have reignited debate about whether we are witnessing the end of US exceptionalism. From our perspective, the era of US asset market dominance in the global financial system may already have peaked. US policymakers appear to have lost all sense of practicality—despite the country's ongoing reliance on foreign capital to sustain the “luxury” of cheap funding it has long enjoyed.

Even as US asset markets undergo significant corrections, the House of Representatives has pushed forward with a 2025 budget plan that would add $5.7 trillion to the national debt over the next decade. In the current uncertain environment, persuading global investors to underwrite such an aggressive expansion of indebtedness will be no easy task.

Meanwhile, the yield spread between US and German 10-year government bonds has widened by 43 basis points in just a matter of days—a sharp move that, while not unprecedented, underscores the shift in sentiments. The US Treasury market’s long-standing status as the world’s risk-free benchmark is now facing serious scrutiny.

Chart 3: US 10-year Government Bond Yield Spread Over Germany Spikes

Source: Bloomberg

The high valuations vis-à-vis the mixed outlook given the pressure of tariffs have probably led to a peaking in the performance of the US equity market relative to the rest of the world in recent weeks. It’s also worth reflecting on the fact that from 1969 to 2015 despite the US economy dominating the world its equity markets went through several cycles of under- and outperformance. Will the last 15 years be seen as just an exceptional period of outperformance that has inevitably come to an end?

Chart 4: MSCI USA Relative to MSCI World ex US Rolls Over Source: Bloomberg

Source: Bloomberg

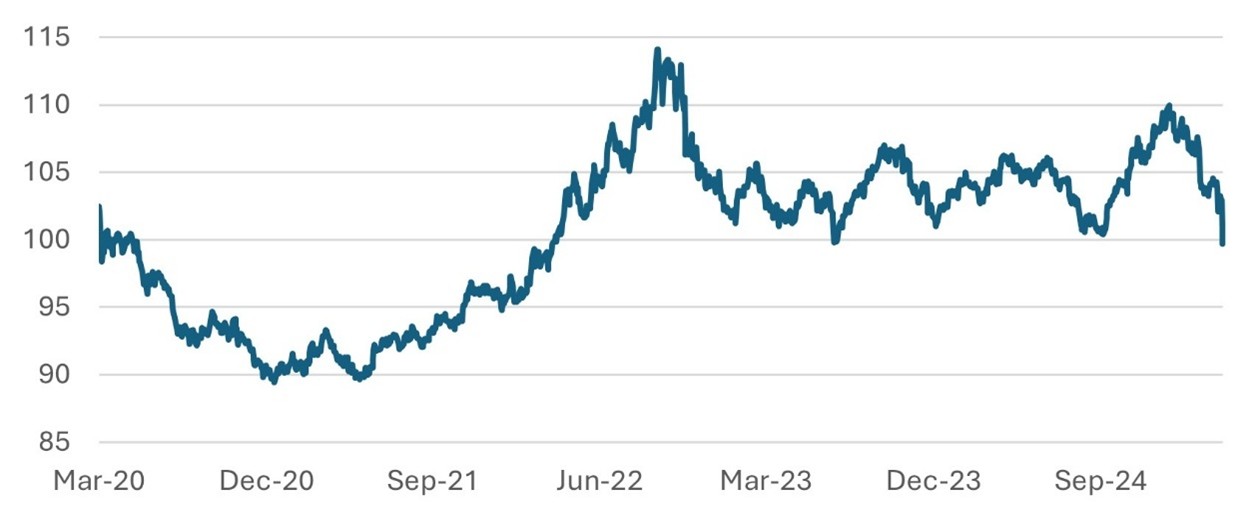

The dollar also looks vulnerable and sits at a key support level. The Dollar Spot Index has fallen around 10% from its peak on 13 January and is down 9% over the past 12 weeks. The index appears vulnerable to potentially falling a further 10% to the 2020 low.

Chart 5: Dollar Spot Index Source: Bloomberg

Source: Bloomberg

What views do we trust?

1. Pro-gold. The events of the past few weeks are a taste of what’s to come: greater uncertainty, higher inflation, and US assets under potential structural selling pressure.

2. Global equity exposure to value plays in Europe and Asia. Be selective buyers of sectors that have more secure returns such as utilities and infrastructure.

3. Global high-grade bonds (40% allocated to US) not US bonds, cautious on credit

4. Seek income over capital gain; Greater allocation to real assets such as commodities, and secure income assets – selective real estate, private debt, and infrastructure.

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

14th April 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB