By Falco

16 Dec 2024

• The Fed will likely cut rates this week by 25bps but may make next year's cuts in interest rates more conditional

• The market expects the Fed to signal that the 'normal' level of policy rates are drifting higher

• The recent move higher in the US 10-year shows the market's concerns about debt and fiscal policy sustainability

• The ECB cut rates last week but may fear cutting too aggressively in the future

• The ECB might compound Europe's economic woes by cutting rates too low, triggering a deflationary mindset in the economy

The Fed to Cut but Then by How Much?

We expect the Federal Reserve to announce a quarter of a percentage point cut to the federal funds rate at its Wednesday 18th December meeting. This adjustment would bring the target range of the policy rate to 4.25%–4.5%, marking a continued effort by the central bank to balance economic growth with inflationary pressures.

However, despite this expected rate cut, many economists predict that the Fed will hit pause in early 2025. This cautious approach likely stems from persistent inflationary concerns and the potential economic impact of President-elect Donald Trump's proposed policies, such as import tariffs and tax cuts, which could amplify inflationary risks.

Following the two-day FOMC meeting, the Federal Reserve will release its updated medium-term forecasts for interest rates. The consensus suggests a slight upward revision to the forecast, with the medium-term estimate for the federal funds rate rising to 3.0% from the previous 2.875%. This shift signals a potential recalibration of expectations, pointing to higher short- and long-term interest rates than previously anticipated.

The higher short- and long-term interest rates likely signify an increasing acceptance by economists and the markets that the days of anything as low as one or two percent are behind us. ‘Normal’ short rates could be anything between three and four percent going forward. The recent increase in the US 10-year government bond yield reflects market worries about the persistence of inflation, the risks to the upside on indebtedness, and fiscal deficits.

Chart 1: US Government 10-year bond yield Source: Bloomberg

Source: Bloomberg

US Small Business Confidence Bounces Even Higher

We've discussed the likely boost to economic confidence in the United States following Donald Trump’s re-election. This optimism was evident in the latest NFIB Small Business Survey, which surged to a 3.5-year high. While this rebound might primarily reflect improved sentiment rather than tangible economic activity, it sets the stage for a potential period of robust growth as the new year begins. A sharp rise in confidence typically translates into increased business activity.

Chart 2: US NFIB Small Business Survey Confidence Source: Bloomberg

Source: Bloomberg

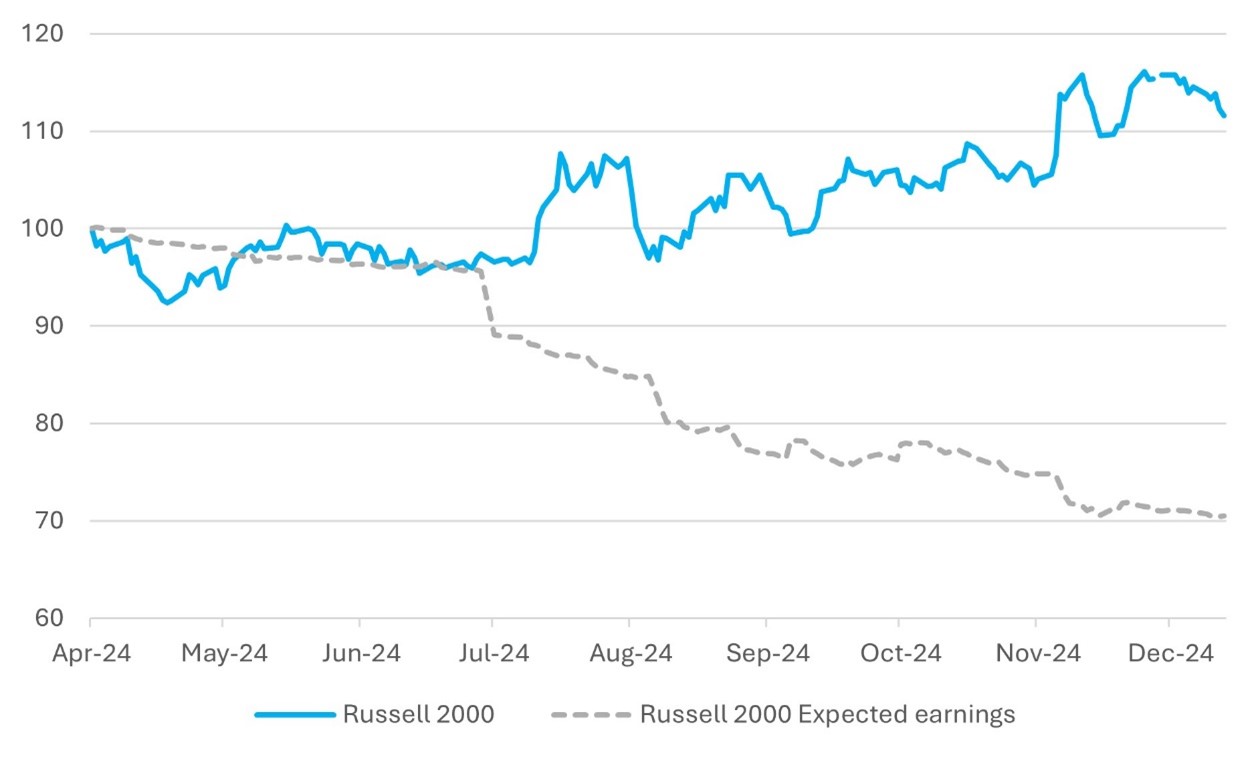

The rise in the NFIB index should bode well for the Russell 2000 index, which a number of strategists wax lyrical about its potential upside, even as earnings forecasts continue to fall.

Chart 3: Russell 2000 Index Rise at Odds with Downgrades to Corporate Profit Forecasts Source: Bloomberg

Source: Bloomberg

In November, the Conference Board's Consumer Confidence Index surged to a 16-month high. However, the critical question remains: will this heightened confidence lead to increased consumer spending? This week’s US retail sales data should show a healthy 0.5% month-on-month increase in spending.

According to McKinsey’s latest quarterly survey of US consumer spending intentions—conducted before the presidential election—confidence remains high, but consumers are increasingly cautious, showing an inclination to delay purchases and trade down. Interestingly, even high-income consumers exhibit spending hesitancy. Compared with the responses from the third quarter, 10% fewer high-income consumers across generations reported plans to splurge in the next three months.

ECB May Need to Cut Rates but Will it Help?

Last week, the ECB cut interest rates by 25 basis points, but it now faces a challenging dilemma. Given the persistently low growth in Europe, the ECB would typically consider more aggressive rate cuts, particularly in early 2025. However, the central bank must contend with weak eurozone growth and a pervasive lack of confidence among both consumers and industrialists. Central bankers likely worry that further rate cuts, in such an environment of fragile sentiments, could backfire psychologically. Instead of stimulating recovery, the cuts might amplify pessimism, worsening the economic outlook, further weakening growth, and potentially triggering a disinflationary spiral. This vicious cycle could ultimately leave the eurozone economy in an even more precarious position.

Recent economic forecasts indicate a subdued growth outlook for the eurozone, with notable concerns for Germany and France.

Eurozone Projections:

• European Central Bank (ECB): On December 12, 2024, the ECB revised its growth forecasts downward, projecting GDP growth of 0.7% in 2024, 1.1% in 2025, and 1.4% in 2026.

• Bundesbank: Germany's central bank has significantly reduced its 2025 growth forecast to a mere 0.1% increase in GDP, citing economic stagnation and potential impacts from international trade tensions.

• OECD: The Organization for Economic Cooperation and Development has lowered France's growth forecast for 2025 to 0.9%, reflecting political instability and economic challenges.

For France, it doesn’t get any better.

Moody’s also downgraded France’s long-term issuer rating to Aa3 from Aa2, citing political instability and deteriorating public finances. Although Moody’s was only aligning its rating with that of other rating agencies, the timing didn’t help. In lingering political concerns for France, previous prime minister Michel Barnier made way for Francois Bayrou, the country’s fourth prime minister in 2024. The economic problems remain the same with a new government trying to find a consensus around a budget plan that addresses the growing deficits yet still leaves enough room for agreement with other parties, particularly Marine Le Pen’s party.

We see further downside risk to the euro – parity still seems something that might be inevitable. There is just no sense in assuming that the region is anywhere close to turning the corner. With growth as weak as it is and the ECB somewhat unsure on policy, the ‘safety’ valve of the economy tends to be the currency. Only a marked weakness in the currency can in a sense rake in some growth by making eurozone products more competitive in global markets – although Donald Trump may have something to say about that! Around 20% of eurozone exports go to the US.

Chart 4: Euro Headed for Parity? Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

16th December 2024

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB