By Falco

17 Feb 2025

• US retail investors are at their exuberant best.

• Last week’s US inflation data was concerning but markets shrugged off the bearish thoughts.

• Fed minutes due out this week key to near term sentiment.

• In Australia, RBA to cut rates for first time in four years.

• Japanese economic data for GDP and inflation should show further normalcy.

• Chinese equities to catch up with Europe’s rally vs the US?

As we reflect on last week’s US market performance, just one word comes to mind: complacency. Despite disappointing inflation data, both bonds and equities managed positive returns on the week, leaving some commentators questioning whether the optimism is justified.

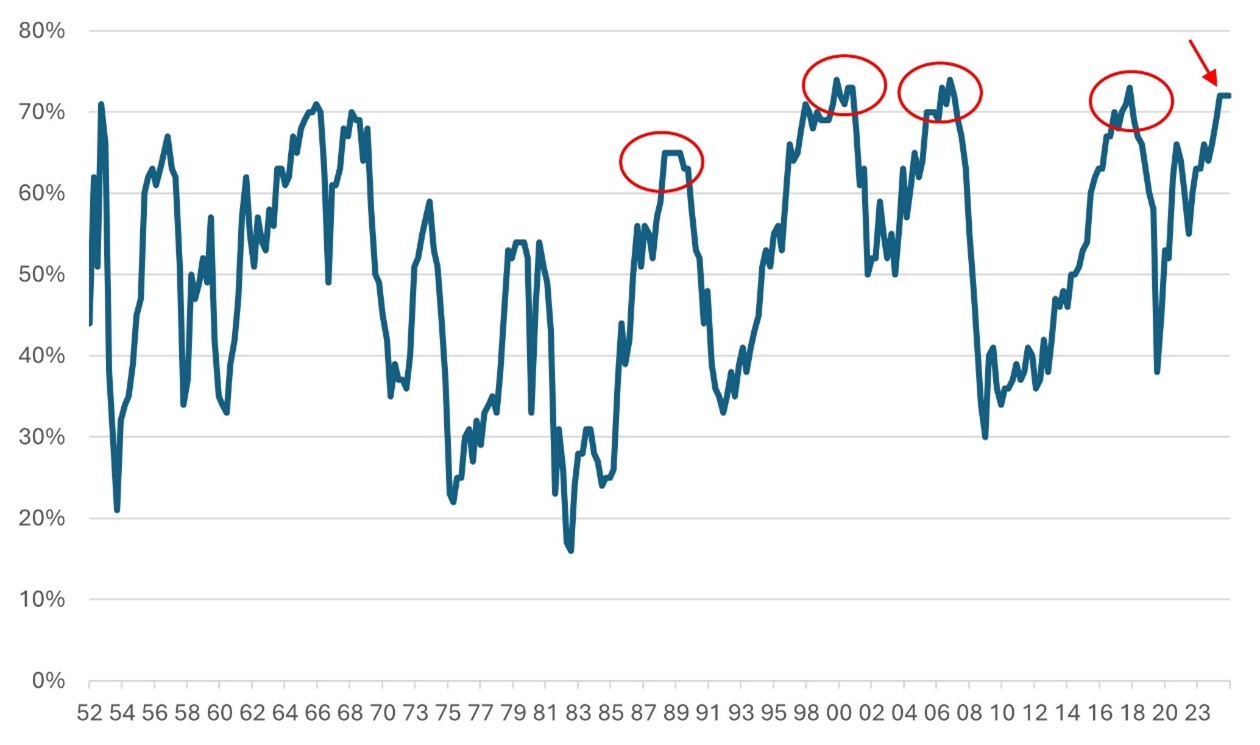

Nevertheless, retail investors remain a driving force behind current equity market strength in the US. According to JP Morgan, retail investor sentiment is at a five-year high, with retail inflows accounting for roughly 30% of average daily market turnover. However, at 73%, the Goldman Sachs Bull/Bear Market Indicator is flashing red—a level historically associated with impending market losses.

Chart 1: Goldman Sachs Bull/Bear Market Indicator Flashing Red Source: Bloomberg

Source: Bloomberg

US Inflation: Another Upside Surprise

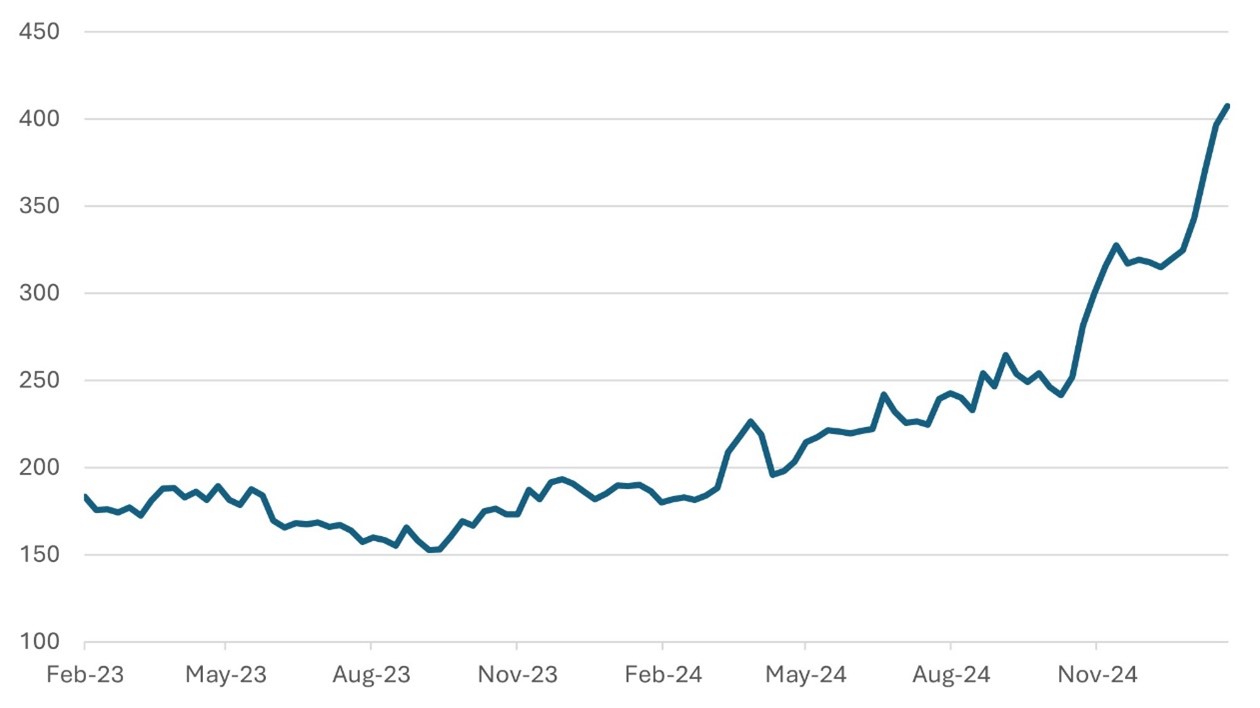

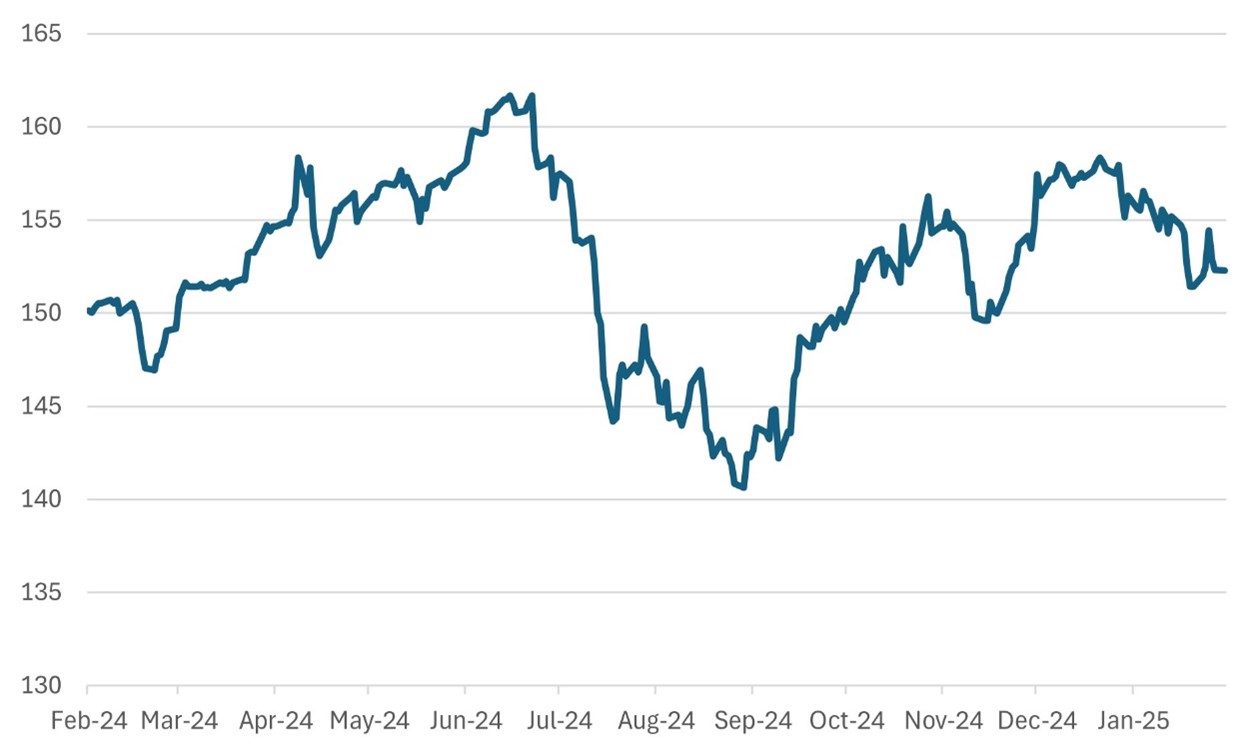

January’s inflation data delivered a negative surprise, with headline inflation rising to 3.0% against expectations of 2.9%. However, of greater concern was the jump in core inflation to 3.3% versus expectations of 3.1%, marking a 0.4% monthly increase that was the highest since March. The data also revealed signs of ingrained inflation, with companies implementing annual price increases at the start of the year. While some categories, like eggs (up 15% because of bird flu) and coffee on the global market up over 100% in a year, saw extreme price spikes, the overall food inflation was more contained at 0.5% month-on-month, which nevertheless affected low-income consumers.

Chart 2: Coffee Spot Price has Doubled in a Year (cents per llb) Source: Bloomberg

Source: Bloomberg

There were some silver linings, too: Owners’ equivalent rent and healthcare costs, for instance, grew at a slower pace. However, healthcare inflation appears out of sync with input prices and could catch up. Meanwhile, the potential impact of future tariffs has yet to materialise, adding another layer of uncertainty to the overall inflation scene.

With inflation persisting, the conversation around the Federal Reserve’s next move has shifted. Markets are now pricing in just one rate cut this year, possibly in late 2025, with a non-negligible risk that the US central bank may even hike rates.

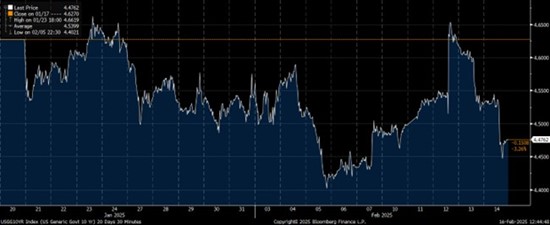

The bond market, too, appears complacent, though last week’s spike in the 10-year yield to 4.66% served as a reminder of the underlying risks.

Chart 3: US 10-Year Government Bond Yield Intra-Day Movement Over Past Three Weeks

Source: Bloomberg

What’s Next for the Fed?

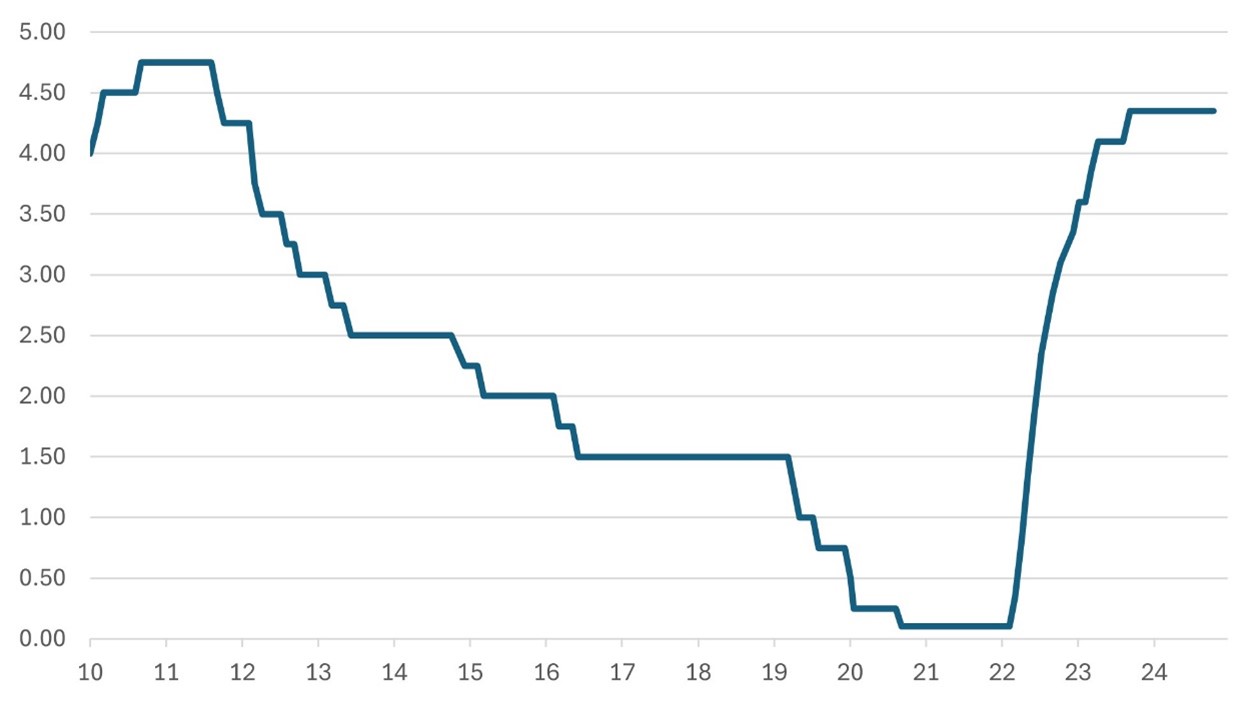

This week, the Fed will release the minutes from its latest meeting held about three weeks ago, which had surprised markets with its hawkish tone. Investors will scrutinise the minutes for clues on the Fed’s views on the current inflation outlook, particularly in light of the proposed tariffs.

The key question for investors is: What if the Fed turns to raising rates instead of cutting? At the start of the year, we flagged the possibility of 10-year Treasury yields reaching 6%, and this scenario remains on the table. With inflation proving resilient and tariff battles looming, the risks are skewed toward higher prices. While the most likely outcome is rates holding steady, investors must prepare for all possibilities—including a rate hike.

RBA Set to Cut Rates After Four Years

The Reserve Bank of Australia (RBA) is expected to cut rates by 25 basis points (bps) this week—its first cut in four years. At 2.4%, inflation has eased to the lower end of the RBA’s 2-3% target range, while the labour market remains robust. Economists anticipate an additional 50 bp of cuts by year-end.

Chart 4: RBA’s First Policy Rate Cut in Four Years Source: Bloomberg

Source: Bloomberg

As the rate cut approaches, the prospect of a more vibrant economy has led to the Australian dollar strengthening against the USD, with sights currently set on 0.65, before it potentially revisits its 12-month high of 0.69.

Chart 5: Aussie Dollar’s Recent Strength Expected to Continue Source: Bloomberg

Source: Bloomberg

Japan – Getting Closer to Normalcy

We are hoping for further signs of normalcy returning to the Japanese economy this week with Japan’s fourth-quarter GDP and inflation data in focus. Economists expect GDP growth of 0.3% quarter-on-quarter and year-on-year inflation of 3%. If the data meets or exceeds expectations, the yen could finally breach the 150 level against the dollar.

The yen’s weakness has made Japan a hotspot for tourism, with cities like Kyoto considering premium pricing on public transport for foreign tourists to manage overcrowding.

Chart 6: JPY/USD to Drop Below 150 Soon? Source: Bloomberg

Source: Bloomberg

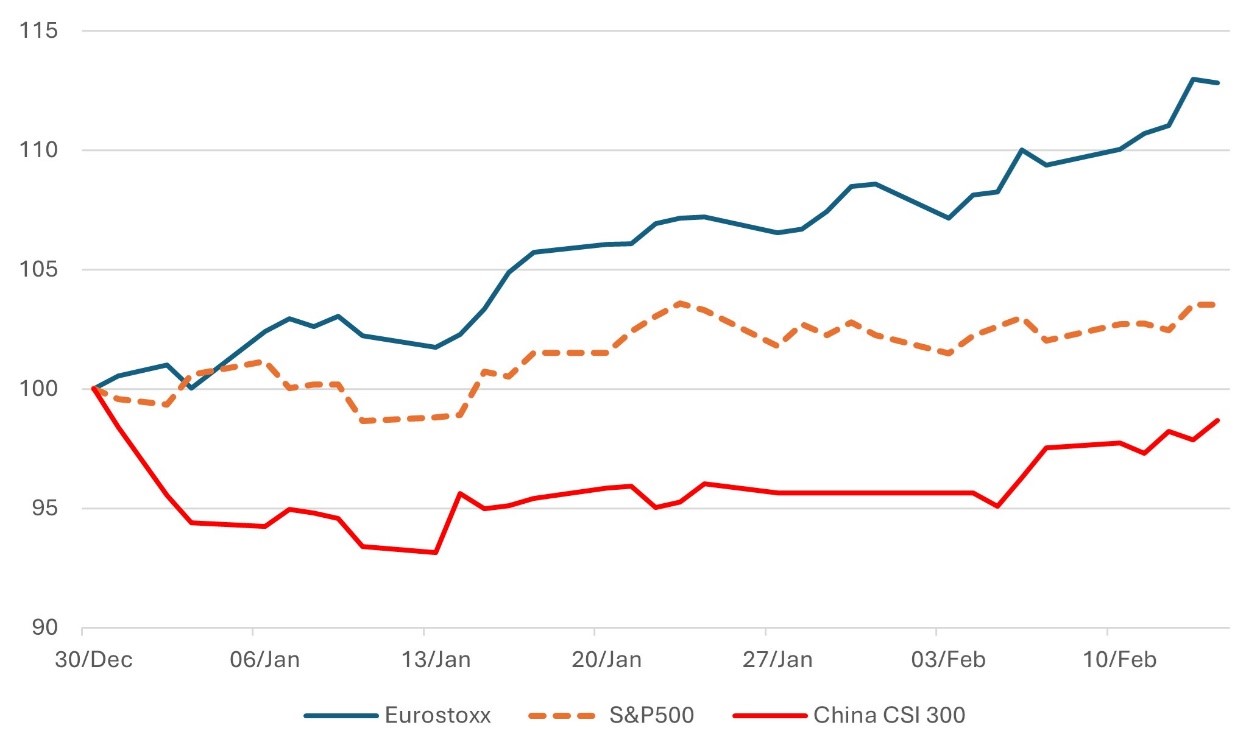

European Equities Leading the Way—Will China Follow?

At the start of the year, we highlighted Europe and China as undervalued markets ripe for a rebound. European equities have since rallied strongly, thanks to the ECB’s dovish stance and fiscal flexibility in France and Germany. In fact, European markets have outperformed the US in local currency terms and even more so in dollar terms.

China, however, has lagged—until now. Green shoots are now visible, particularly in the tech sector, where companies such as DeepSeek highlight China’s competitiveness and attractive valuations. Economists are growing more confident, with JP Morgan upgrading its Q1 GDP growth forecast for the country to 5.3%. Bank lending has also picked up, supporting small and medium-size enterprises. With tariffs less severe than feared, China could join Europe as a leading market in the first quarter.

Chart 7: Europe Leading the Equity Market Rally Year-to-Date Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

17th February 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB