By Falco

20 Jan 2025

Call it an ironic alignment or whatever you may, but the inauguration of President Trump coincides with the celebration of the Chinese New Year of the Snake. The snake is symbolic of wisdom, knowledge, intelligence, intuition, and creativity –ideals that the incoming president would do well to embrace, potentially guiding his decisions for the betterment of all. However, as the new administration takes shape, the word "disruptive" feels like the least contentious descriptor for what could be in the offing. President Trump, on his part, has promised sweeping actions, including potentially hundreds of executive orders targeting immigration and trade. The financial markets, therefore, enter this period of transition braced for volatility, as investors attempt to predict the impact of these promised changes on the economy.

Immigration: Expect big announcements, but action more difficult

Trump has signalled his intention to deploy executive orders aimed at swiftly removing undocumented immigrants from US streets, particularly in specific states or cities, and expediting their deportation. With an estimated 11 million people in the US lacking legal status, these ambitious plans face significant hurdles. The key challenges include securing funding to implement these orders and Congressional approval.

Currently, the Immigration and Customs Enforcement is operating with a $200 million deficit. Analysts estimate that achieving Trump’s deportation targets would incur an astronomical cost of about $88 billion, according to the American Immigration Council. What makes it further complicated is the fact that approximately 70% of deportations from the US interior are initiated by enforcement agencies outside of federal control.

One way forward for President Trump could be invoking the National Emergencies Act of the 1970s, which mandates the use of Pentagon funds and military resources to deport undocumented immigrants. While this approach might bypass a potential Congressional gridlock, it would likely be contentious and polarising, potentially rattling financial markets. Nevertheless, such actions could lead to mass deportations, triggering labour shortages and pushing wage inflation higher as employers scramble to fill vacant roles. This labour market turbulence could inject volatility into equities and bonds, particularly in labour-intensive sectors.

Trade Tariffs: A Prescription for Inflation

Trade policy under the new administration will keep financial markets on edge, with any early announcement on tariffs likely having far-reaching implications. If Trump invokes the International Emergency Economic Powers Act to impose sweeping tariffs, markets could react sharply, driven by fears of accelerating inflation and potential disruptions to global supply chains.

In recent months, Trump has floated dramatic tariff proposals, including a 25% tariff on imports from Mexico and Canada, a 10% tariff on all imported goods, and an eye-popping 60% tariff on imports from China. The market’s reaction to these proposals will largely hinge on whose counsel ultimately holds sway within the administration. Treasury Secretary Steven Mnuchin has reportedly advocated for more targeted and incremental tariff measures to minimise early disruptions to financial markets. However, a more aggressive approach could spook investors, leading to sharp sell-offs in equities and a potential jump in bond yields as inflation expectations rise.

The unravelling of Trump’s policies on immigration and trade will undoubtedly set the tone for financial markets in the coming months. Investors should brace for potential volatility as these high-stakes issues evolve. Markets will be watching closely to gauge the impact of Trump’s decisions on growth, inflation, and overall economic stability. The road ahead promises to be anything but smooth.

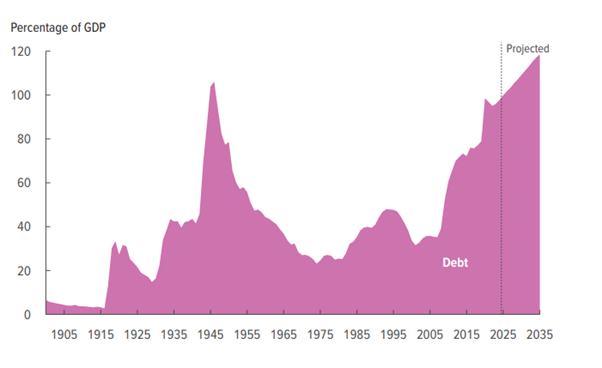

Congressional Budget Office Projections a Strait Jacket on a Trump Administration

This week’s report from the Congressional Budget office (CBO) was a timely reminder of the budgetary constraints that face Trump in his second term. In 2017, when Trump took office the national debt-to-GDP ratio was 77%. This time, as he enters the Oval Office, that number has ballooned to 99%! The CBO expects the national debt to rise by $23.9 trillion over the next ten years, not accounting for the additional tax cuts that Trump has proposed, which could add an additional $4 trillion to the national debt.

Trump’s More Ambitious Plans Will be Constrained by the Burden of Debt

Under current laws, federal debt held by the public is expected to rise substantially, reaching a percentage of GDP not seen since the World War II. Factors contributing to this include rising interest costs, mandatory spending increases, and slower revenue growth relative to economic output. Overall, the CBO's report highlights the long-term fiscal challenges facing the US, with debt levels expected to continue climbing unless significant policy changes are implemented. This raises concerns about fiscal sustainability and places pressure on policymakers to address both revenue and spending trajectories.

Chart 1: CBO Projections of US Federal Debt Burden

Source: CBO

A likely response from the Trump administration could be spurring additional economic growth through deregulation while reducing spending via initiatives led by figures such as Elon Musk and Vivek Ramaswamy, under the banner of the Department of Government Efficiency (DOGE). However, Elon Musk recently tempered expectations, lowering DOGE's target for spending cuts to $1 trillion from $2 trillion. Notably, two-thirds of current federal expenditures are tied to programmes such as Medicare and Social Security—either pledged by Donald Trump to remain untouched or deemed politically unfeasible to reduce.

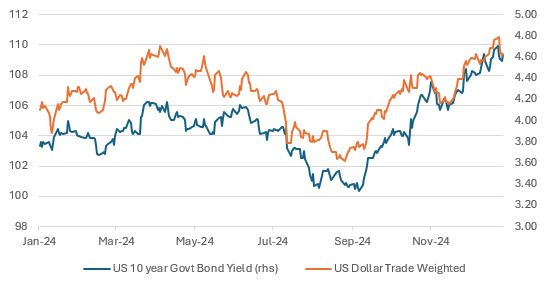

Will Financial Markets Call Trump to Account?

President Trump must closely monitor financial markets to ensure his policies do not disrupt the bond and equity markets. The pressure is mounting. While he may project an air of authority (as demonstrated in the Supreme Court ruling), he remains accountable to the bond and currency markets. The bond market is already vigilant, and the dollar's trajectory will be critical.

A worst-case scenario would mirror Turkey, where political interference in economic policy resulted in rampant inflation, a collapsing currency, and soaring interest rates. Although Trump has hinted at intervening in Federal Reserve leadership, he cannot dictate the bond market. His administration must manage inflation and the deficit carefully, or the markets may respond harshly.

Chart 2: Trump Begins Second Term – This is Where the US 10-year and USD are

Source: Bloomberg

In the immediate term the US equity market looks set to try to re-test the December highs. Last week’s marginally better-than-expected inflation data and a knockout industrial confidence survey from the Philly Fed survey has investors encouraged. Throw in a very good set of quarterly results from several of the banks and the path is clear for some further gains irrespective of long-term concerns about valuations.

Chart 3: S&P500 Targeting a New High in the Very Near Term

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

20th January 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB