By Falco

24 Feb 2025

President Trump’s unrelenting stance on tariffs, coupled with deeper cuts to government spending (chainsaw-inspired, as Elon Musk perhaps would prefer), is causing significant disruptions to the US economy. The resulting uncertainty has caused tremendous shock that is rippling through various sectors, leading to market volatility and growing investor unease. The euphoria that followed the election result has made way to a worrying reality of weaker growth and greater volatility.

Chart 1: Marked weakness in US Economic Surprise Index Source: Bloomberg

Source: Bloomberg

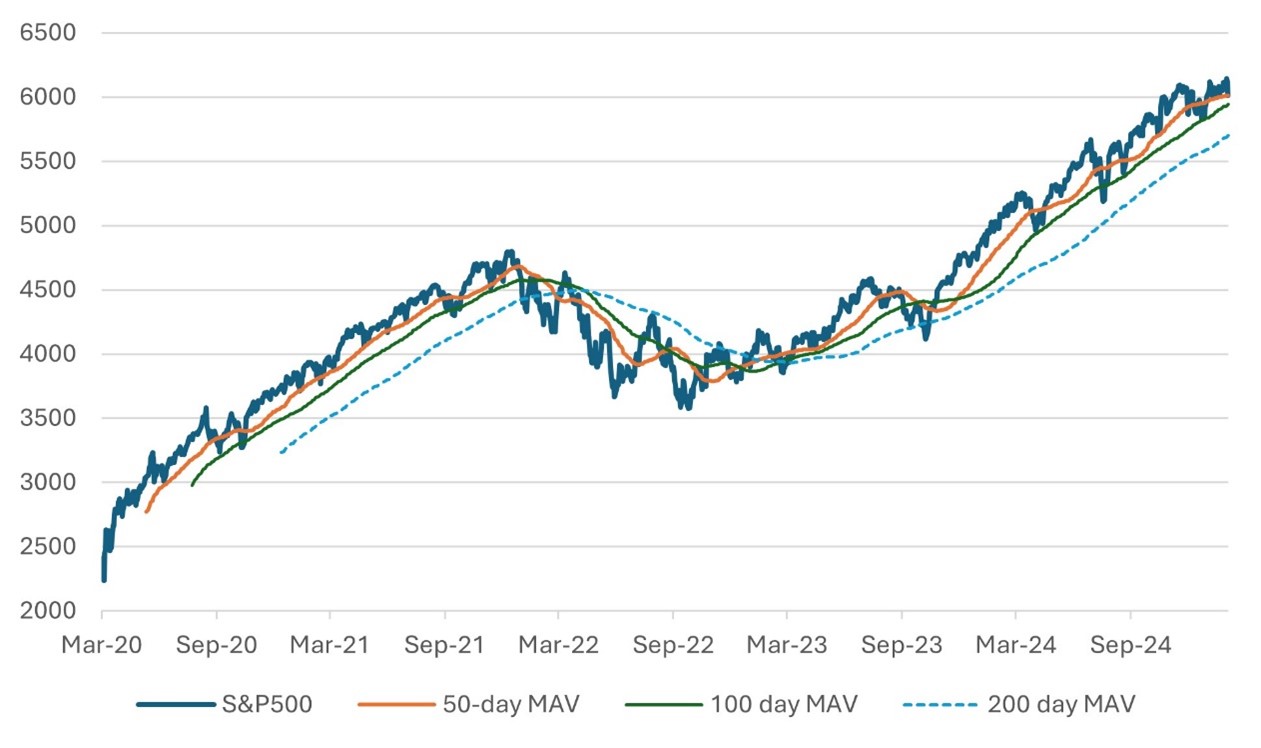

The S&P 500 scaled two new record highs last week but also experienced its worst day this year. While the market is still up 2.5% year-to-date, the balance of risks suggests a potential test of the 50-day moving average on cards, with further losses possible in the coming weeks. As we indicated at the beginning of the year, other markets are more attractive and are already outperforming. The Euro Stoxx index has gained nearly 13% in dollar terms, while the Hong Kong market has surged 17% year-to-date. In our view, investors are seeking diversification away from the US market, which continues to throw surprises that contribute to increased volatility and diminished returns.

Chart 2: Core PCE inflation Moving Closer to Fed’s Target Source: Bloomberg

Source: Bloomberg

Last Friday’s sharp decline in the S&P 500 highlighted a clear rotation out of economically sensitive sectors such as consumer discretionary and technology into defensive sectors such as consumer staples and utilities. Nearly 80% of consumer staples and utility stocks gained on Friday, indicating broad-based sector moves by traders. In contrast, not one information technology stock closed in the positive territory.

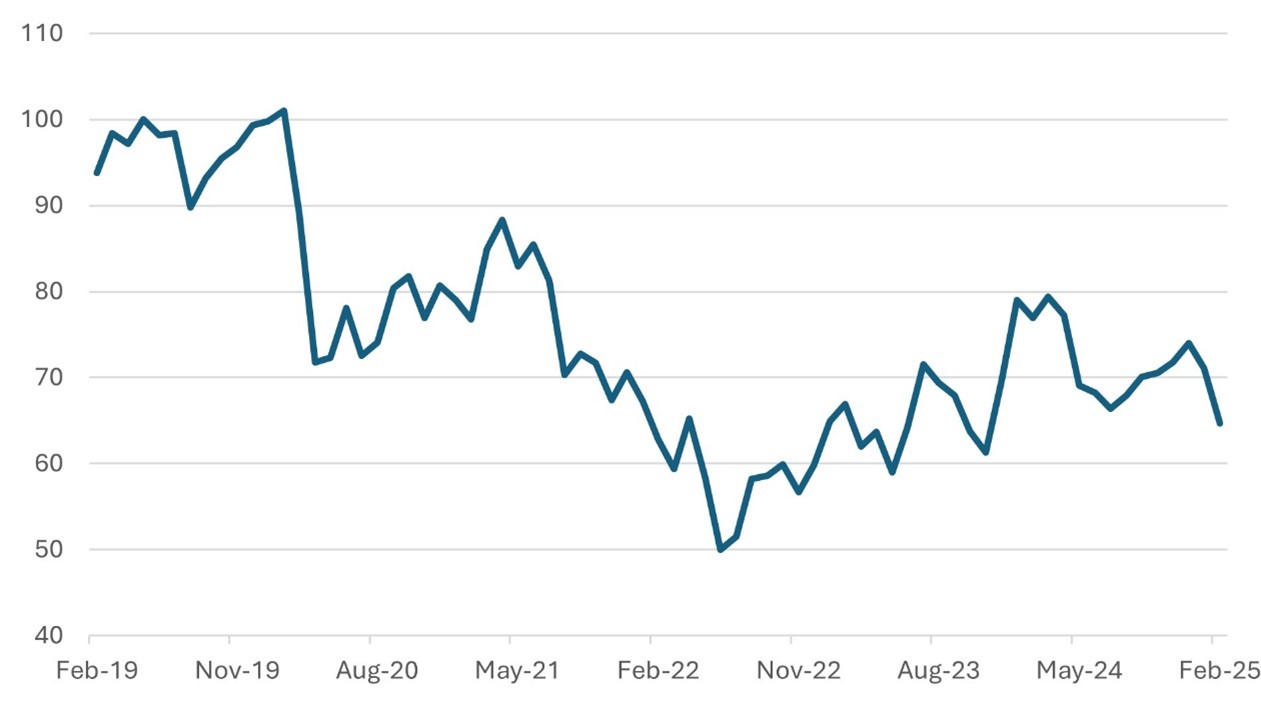

One of the key themes last week was whether the president was losing support from consumers. The catalyst for that discussion was the University of Michigan’s consumer sentiment survey, which reported a decline in confidence amidst persistent inflationary concerns. Final revisions to the data further lowered those numbers, noting consumer sentiment was down to its lowest since November 2023. Perceived inflation likely is the problem here.

Chart 3: US Consumer Confidence on the Slide

University of Michigan Consumer confidence survey Source: Bloomberg

Source: Bloomberg

China: Better News, But Struggling for Great News

There has been a distinct improvement in confidence about developments locally and on the Mainland. What also distinctly stood out and perhaps signalled China’s tech reset was President Xi Jinping meeting Alibaba’s Jack Ma at a symposium with private sector entrepreneurs. While the meeting helped boost sentiments, it also signalled Ma’s “rehabilitation” to the country’s top political circles. There remains a significant focus on the tech sector, which should surpass the real estate market in terms of contribution to GDP (19%) by next year. Nevertheless, much of the dialogue and reporting from the meetings was positive but nothing groundbreaking emerged.

The Chinese economy needs further drivers of growth given consumer demand is slacking and exports are weakening. Foreigners have been putting very little money into China. The country recorded net inflows of only $4.5 billion in 2024. Foreign direct investment fell a record $168 billion last year, the largest drop since record keeping began in the 1990s.

The 12th special study session of the Chinese State Council had a focus on boosting consumption, but little detail was available on the ways to bring about some improvement in consumption.

Chart 4: Hong Kong Equity Index (HSI) Well Ahead of Mainland Index (CSI 300) Source: Bloomberg

Source: Bloomberg

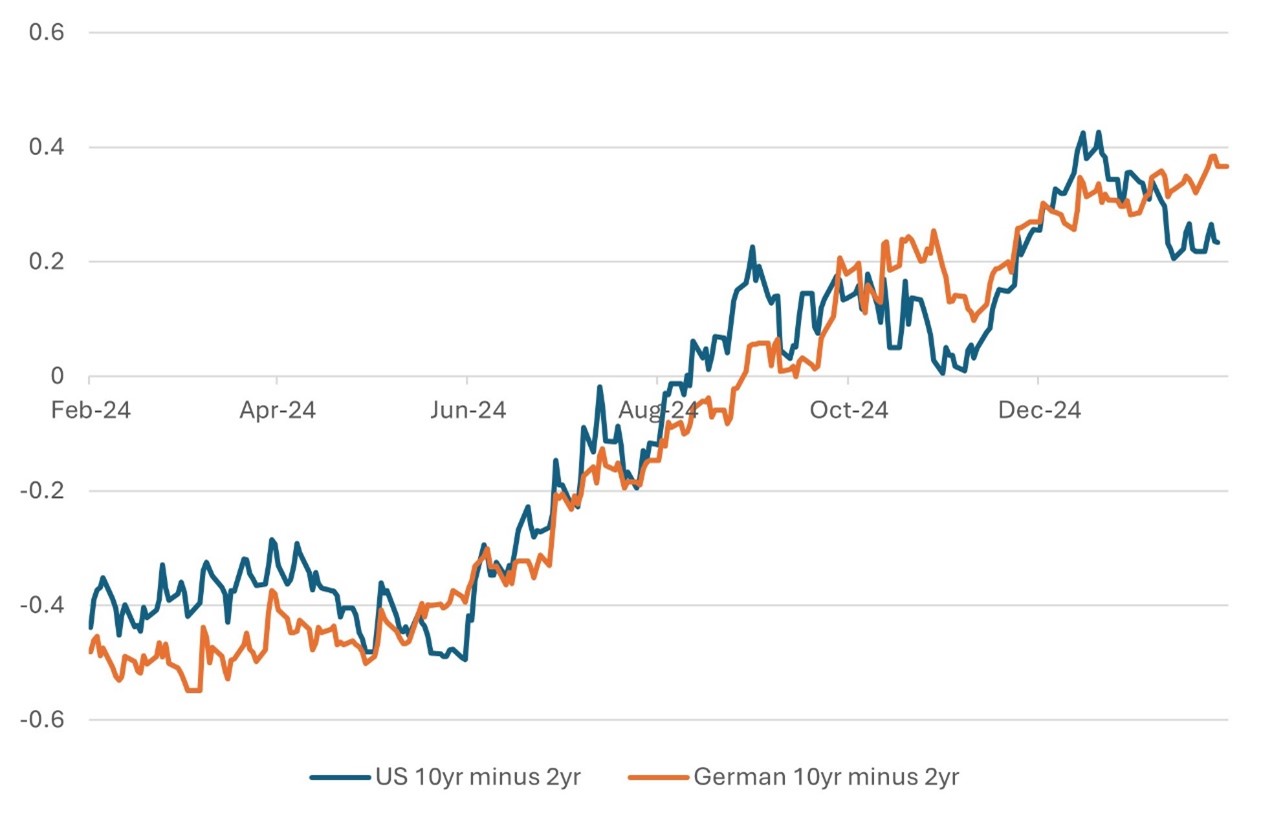

Bond Markets to Diverge?

With talks of tariffs and higher risks of increases in government spending as countries up their defence budgets, the bond markets are very much on watch. The US and German yield curves have recently diverged in terms of shape as the risk to rates and long-term yields have had different influences. Germany/Europe face greater risks of inflation given the likely need to increase defence budgets and hence aggregate spending. Meanwhile the ECB seems committed to rate cuts, which has led to a steepening of the yield curve.

Chart 5: US and German Yield Curves Diverge

US and German 10 year less 2 year government bond yields Source: Bloomberg

Source: Bloomberg

By contrast the US yield curve has gently flattened. There is some building hope that inflation is maybe on its way down. This week’s PCE deflator, the Fed’s preferred inflation measure, is expected to be around 3.6%, closer to the Fed’s target than other measures that have resolutely stayed around 3%. We think there is an increasing concern that US growth is weakening. The recent readings of the US economic surprise index have been noticeable, possibly reflecting the fallout from the impact of the trade tariffs and Elon Musk’s chainsaw approach to trimming government spending (and the federal workforce).

A New Geopolitical Order and Its Investment Implications

Political analysts are actively dissecting the Trump presidency and its broader implications for the global economy. In an intriguing analogy, former MI6 chief Alex Younger, speaking on BBC Newsnight, suggested that President Trump's influence signals a shift toward a new geopolitical order. He likened the current landscape to the Yalta Conference of February 1945, where Russian President Josef Stalin, British Prime Minister Winston Churchill, and US President Franklin D. Roosevelt laid the foundation for a new world order dominated by their three nations.

Today, a similar dynamic appears to be emerging, with global power concentrated in the hands of three key leaders: President Trump, President Xi Jinping, and President Vladimir Putin—each governing with a firm grip. Their policies, ambitions, and interactions are reshaping the geopolitical landscape, marking a clear departure from the multilateralism that defined the past decades.

India, to some extent, and Europe now find themselves on the periphery, navigating an evolving global hierarchy. As new alliances take shape (and some fall apart), they will have profound implications for trade, investment flows, and economic stability. Investors should closely monitor these geopolitical shifts, as they will play a critical role in shaping future market opportunities and risks.

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

24th February 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB.