By Falco

03 Feb 2025

It was perhaps a foregone conclusion that President Trump would turn to tariffs as a tool to address seemingly unrelated issues such as immigration and the fentanyl crisis. His decision to restore 25th President William McKinley’s name to a US landmark—North America’s tallest peak— further underscores his inclination to wield trade policy as a geopolitical weapon. McKinley was a 19th-century champion of high tariffs, who, Trump says, made the United States richer through tariffs.

That’s not good news for the global economy, though, which now faces fresh downside risks. President Trump’s newly announced tariffs—25% on imports from Canada and Mexico, and 10% on imports from China—pose a significant threat to growth and inflation. Retaliatory measures from affected nations are all but certain, adding to the economic volatility.

What makes this round of tariffs especially concerning is the supposed rationale behind them. Rather than being framed solely as trade policy, the administration is openly presenting them as leverage to curb immigration and disrupt fentanyl trafficking into the US. Yet this justification appears tenuous at least for Canada which accounts for just 1% of known fentanyl and illegal immigration flows, according to official sources.

Compounding the uncertainty is the lack of clear benchmarks or a defined timeline. For instance, there is little clarity on what conditions would justify lifting the tariffs. A measurable drop in fentanyl supply? A decline in illegal border crossings? Without specific criteria, investors and businesses are not only left guessing about the potential impact of these measures but also their duration and ultimate resolution of this policy shift.

Recent analyses provide specific estimates on how the newly imposed tariffs by the US on Canada, Mexico, and China are expected to affect the US economy:

Impact on US Economic Growth (GDP):

• Goldman Sachs Analysis: The firm projects that the new tariffs could lead to a 0.4% reduction in US GDP.

• Tax Foundation Study: This analysis estimates that the proposed tariffs could reduce long-term US economic output by 0.4%.

Impact on Inflation:

• Goldman Sachs Projection: The firm anticipates a 0.7 percentage point increase in core inflation because of the tariffs.

• American Enterprise Institute Estimate: Studies suggest that the average American household may lose between $1,000 and $1,200 in annual purchasing power as a result of the tariffs, indicating a significant inflationary effect.

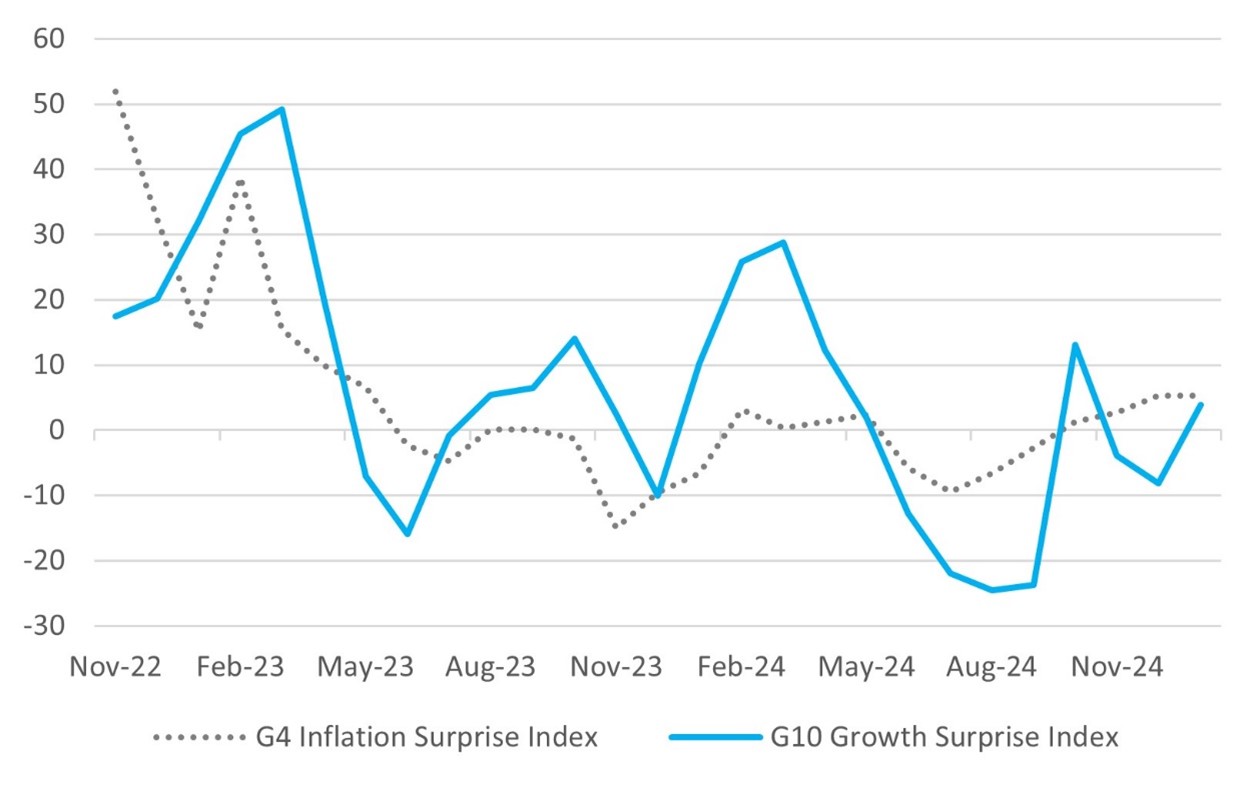

Global inflation and growth surprises, which have been relatively neutral in recent months (Chart 1), are likely to diverge—with inflation exceeding expectations and growth falling short. We anticipate higher long-term US government bond yields and expect equities to react negatively to the threat of tariffs.

Chart 1: Global Economic Surprise Indices – Inflation and Growth

Index Source: Bloomberg

Source: Bloomberg

The latest trajectory on growth and inflation is not good for markets. The Fed rang the bell of caution on market hopes of rapid rate cuts, and will feel vindicated by the President’s actions. The Fed will be concerned that the tariffs will ultimately result in higher inflation and lower growth. We will have to see how the markets react and how much caution will be priced into the current expectations for rate cuts in 2025. As of Friday, the market was still hoping for 50bps of rate cuts in 2025 – dream on!

January Market Trends: A Shift in Sector Dynamics

January saw some notable market movements, reinforcing key themes we’ve been advocating for. The negative return in the Global IT sector for the month aligns with our earlier concerns that the industry might struggle to replicate the excess gains of 2024. The unveiling of DeepSeek ten days ago was a catalyst for investors to sit up and take notice, but it may not necessarily overwhelm the US majors. It does, however, underscore the reality that tech is no longer a guaranteed source of outsized returns. Increasing competition and regulatory scrutiny may further weigh on the sector in the near term.

Meanwhile, traditional sectors demonstrated resilience. Strong and steady returns from banks in equity markets – alongside robust performance in high-yield bonds, of course – highlight that "old economy" companies can still generate solid returns—particularly in an environment of normalised interest rates and stable economic conditions. This shift suggests that investors are recalibrating portfolios, favouring sectors that benefit from higher interest rates and a more balanced macroeconomic backdrop.

Table 1: Global Equity Sector Total Returns ($) for January 2025

| -1 month | -3 months | -12 months | ||

| Energy | 2.6% | -0.5% | 6.4% | |

| IT | -1.5% | 4.4% | 25.8% | |

| Consumer Staples | 1.9% | -0.2% | 7.0% | |

| Consumer Discretionary | 4.6% | 17.1% | 29.1% | |

| Healthcare | 6.4% | -1.0% | 4.8% | |

| Banks | 8.1% | 12.0% | 38.6% |

Source: Bloomberg

Key Takeaways

1. Tech Sector Reality Check – While innovation in the sector continues, valuation concerns and heightened competition are tempering expectations for outsized gains. Investors may need to be more selective, focusing on companies with strong cash flows rather than speculative growth.

2. Financials Gaining Favour – With interest rates at more normalised levels, financial institutions are well-positioned to benefit from improved net interest margins and credit stability.

3. Diversification Matters – The outperformance of banks and high-yield bonds highlights the importance of a diversified portfolio. The days of relying solely on tech for market-beating returns may be behind us.

Gold Has More Upside

Gold hit a new all-time high last week, and with the impending trade war, we can only see further upside. We continue to advocate that investors should ordinarily aim to have around 5% of their assets in gold. From a technical perspective Gold’s uptrend has regained momentum, with the yellow metal moving to a record high of $2,817. Technical analysts believe that a sustained rally could see buyers targeting $2,830, followed by $2,900 and eventually the $3,000 mark.

On the downside, analyst suggest that only if the metal fell below $2,750 would there be more serious profit taking.

Chart 2: Gold Price Hits an All Time-High and Appears to Have Further Upside Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

3rd February 2025

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB