By Falco

25 Nov 2024

As we navigate the transition of power from the Biden administration to President-elect Donald Trump, it is striking how analysts continue to argue that the US equity market can sustain further gains in the year ahead.

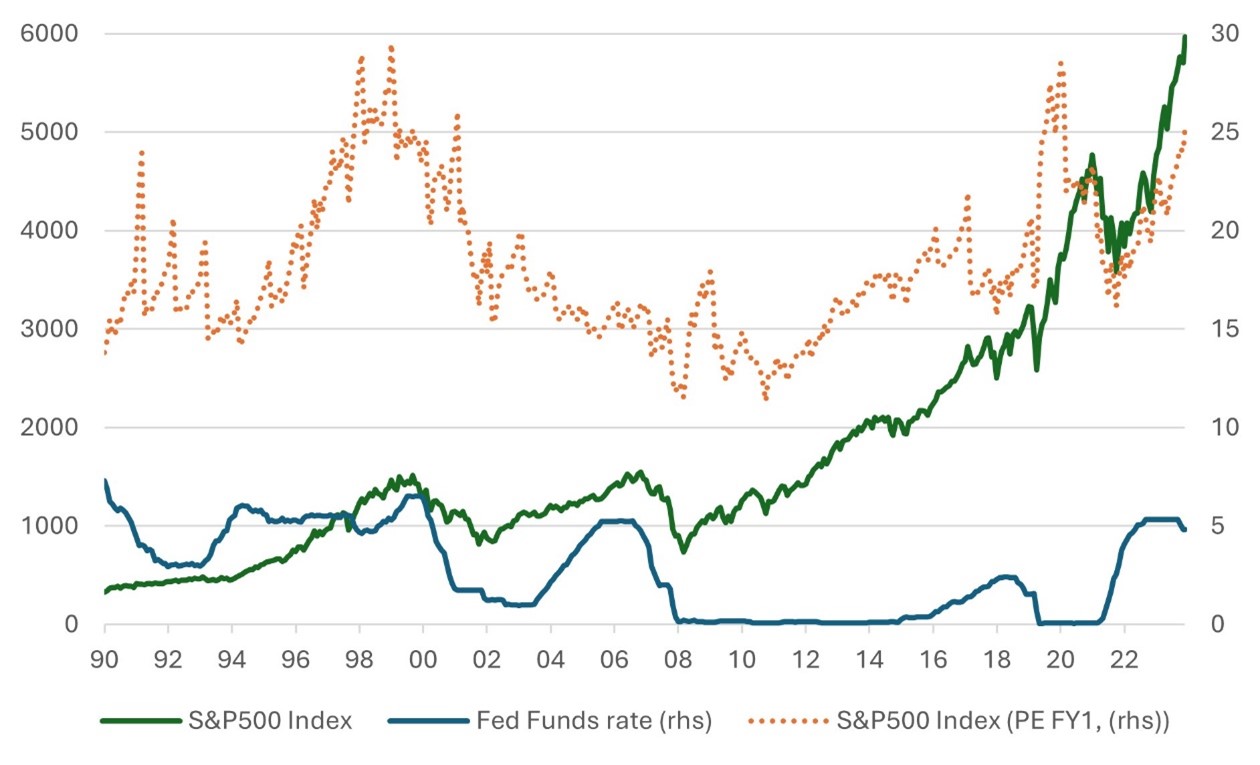

Let’s be honest: few are willing to call a top in the US equity market, which has had a remarkable bull run for much of the past decade. However, it is now perhaps time when we must question – and be concerned – whether the market has outpaced fundamentals. One key valuation metric that encapsulates our concern is the price-to-earnings (P/E) multiple.

According to Bloomberg, the forward P/E multiple of the S&P 500 currently stands at 25.2x. Even accounting for projected earnings growth over the next 12 months, this valuation represents the highest level in nearly 23 years - excluding the anomalous COVID years.

Chart 1: S&P500 - Exceptionally High Valuation Source: Bloomberg

Source: Bloomberg

Defying Fundamentals

Such lofty valuations are challenging to justify unless one assumes that the Federal Reserve will resort to aggressive interest rate cuts in the coming year. For context, consider the period between 2002 and 2003 when the Fed funds rate went on a downward trajectory, eventually reaching 1% in 2004. Despite this, the S&P 500's P/E multiple back then peaked at just 20x forward earnings. Moreover, the market’s recovery during that period was supported by a robust rebound in corporate earnings following the tech bubble bust, with expected earnings for the index rising 50% from a low base.

If we can offer a scenario for 2025 it would be slow rate cuts, tax changes, and animal spirits that support GDP growth of, say, 2.25%.

In contrast, today’s market appears to be banking on a perfect scenario: falling interest rates, resilient earnings growth, and sustained investor confidence. While optimism has its place, history reminds us that markets rarely move in a straight line. Investors should carefully weigh whether current valuations leave enough margin for error or whether the market has simply gone too far too fast.

Markets Tech-ing it for Granted?

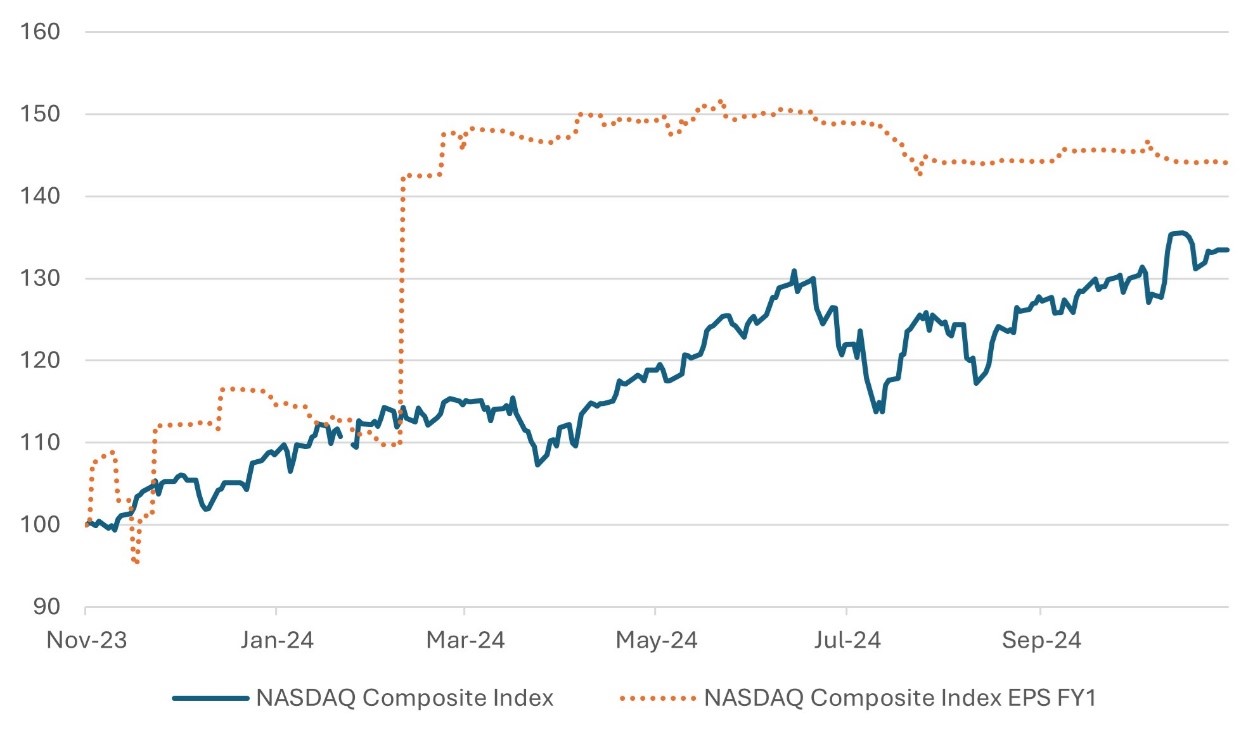

Will the AI tech boom sustain, or be vulnerable over the coming years? That remains a topic of significant interest, as both opportunities and risks shape its trajectory. A key driver of the broader market’s performance has been the tech-heavy Nasdaq index, with standout contributors such as Nvidia playing an outsized role. Nvidia alone has accounted for more than 20% of the Nasdaq’s return this year, underscoring the index’s heavy reliance on a few tech giants to sustain market momentum.

Last week, Nvidia announced Q3 results that exceeded expectations, yet the share price reaction was subdued. The muted response stemmed from slightly lower-than-expected revenue guidance for the ongoing quarter, highlighting how high market expectations can temper enthusiasm even when earnings are strong. Despite this, the tech sector continues to deliver robust earnings, confounding sceptics. Notably, an analysis of the rise in the index of projected earnings versus the price index reveals that the sector has experienced P/E deflation. This indicates that the earnings growth has outpaced price growth, enhancing valuation attractiveness. In contrast, the Magnificent 7 (Mag7) tech stocks have seen P/E expansion of approximately 10%, suggesting a different dynamic in valuation trends within the tech universe.

Chart 2: Scale of Positive Earnings Revisions Stronger than Index Price Appreciation

Nasdaq composite and earnings index rebased to -1Y =100 Source: Bloomberg

Source: Bloomberg

Risks in the Tech Sector: The "Mundane" and the Systemic

While the AI sector’s potential remains immense, risks to it could stem from more mundane, yet impactful, factors. Nvidia, for example, derives 53% of its revenue from gaming—a segment particularly vulnerable to an economic slowdown. If global GDP growth falters, discretionary spending on gaming could decline, pressuring Nvidia's core revenue streams.

Moreover, the growth of AI is intricately tied to the funding ecosystem. Startups driving innovation in AI often require significant investment to bring their ambitious plans to fruition. A tightening funding environment, whether due to rising interest rates or risk-averse investor sentiment, could stifle the pace of AI adoption and technological breakthroughs.

Another critical challenge lies in infrastructure. AI’s rapid expansion necessitates a massive buildout of data centres, which are energy-intensive and require stable, scalable power sources. The industry’s reliance on yet-to-be-developed energy infrastructure introduces a bottleneck that could impede growth. Delays in building sustainable energy solutions or disruptions in supply chains for critical components could pose substantial risks to the sector’s scalability.

Cautious Optimism

While some strategists advocate caution on the tech sector, the broader narrative suggests a remarkable ability to deliver on earnings and innovate in transformative ways. AI, in particular, continues to drive enthusiasm as companies integrate machine learning and advanced algorithms into diverse industries, from healthcare to logistics. However, balancing optimism with an understanding of the sector’s inherent vulnerabilities is crucial.

As we move forward, the interplay of external factors - such as macroeconomic conditions, regulatory scrutiny, and geopolitical dynamics - will play a pivotal role in shaping the tech sector's trajectory. Investors and stakeholders must remain vigilant, recognising that while AI and tech represent unprecedented opportunities, the journey ahead is fraught with challenges requiring strategic foresight and adaptability.

Further Signs of Weak European Growth; Asia on Track

The euro area flash composite PMI fell 1.9 points in November to a level that typically is consistent with stalling GDP growth. However, in Asia, economic data has been stronger than expected, particularly with strong external demand. The strong external demand could also be a factor of companies building up their imports of Asian products ahead of a potential US trade tariff war.

Japanese exports of semiconductor goods to China have been on a tear of late, suggesting a front-loading of technology demand from China ahead of the new US president taking office. In other developments, Japanese inflation remains robust enough to warrant a likely increase in interest rates at the next Bank of Japan meeting in late December. Such a rate increase may help the yen recover from recent oversold levels.

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

25th November 2024

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB