By Falco

30 Dec 2024

The markets are experiencing a somewhat uncharacteristic end to the year. The sharp inversion of the US government bond yield curve and the ongoing strengthening of the US dollar, for instance, are reverberating around the global markets.

Although the markets’ initial reaction to Trump’s re-election to the White House back in November was euphoric, they now seem to be more carefully analysing the incoming administration’s priorities. We list below a few challenges to those positive views on markets that have emerged in the aftermath of the presidential elections.

1. Maybe the President-elect’s honeymoon period with the markets is over. The Conference Board’s consumer confidence index fell 8.1 points in December, led by the marked decline in the expectations index, which tumbled 12.6 points to 81.1. Usually, 80 marks the threshold that signals a recession. The data was well below market expectations. Interestingly, those surveyed pointed to the tariff issue as something that they are concerned about.

2. Political bickering has exposed the stark differences on the thorny issue of immigration, sharply dividing the pragmatics and the dogmatics within the movement. We could see more such clashes coming to the fore as the President-elect’s policies take a more concrete shape.against those in the movement that oppose almost any immigration The fallout in the MAGA movement about immigration is pitting private sector reps such as Elon Musk and Vivek Ramaswamy who favour a continuation of visas for top talent in the tech sector.

3. Investors are more worried about the outlook for US inflation and the likely slow pace of rate cuts going forward. The 2-year/10-year Treasury yield spread widened another 7bps this past week to 29bps, the widest since June 2022. The Treasury curve has steepened 21bps since the Fed cut rates on 18 September for the first time in four years, with the 10-year yields having now spiked 97bps since. The US 10-year ended the week at 4.63%, the highest level since May.

4. In developed markets, yields were pulled higher by actions in the US. French yields rose 13bps, the highest since July. The 10-year Japanese government bond yield rose to 1.11%, the highest since July 2011. Latin America has borne the brunt of the sell-off. Brazilian 10-year bond yields are up 75bps month-to-date and approaching the 2006 highs. Mexico’s local debt 10-year yield rose to 10.87%, the highest since 2002.The backup in long-dated US bond yields is affecting the global rates and bond markets, particularly in the emerging markets.

5. The spike in US bond yields is causing some angst in the junk loan market. Investors are starting to realise that a smooth path to lower long-term interest rates is no longer the most likely scenario in the coming quarters. Defaults in the global leveraged loan market rose 7.2% in the year to the end of October.

6. It is worth noting that quite a few investors are nursing some disappointment with the year-end performance of the bond markets. According to EPFR, bond funds attracted $600bn of inflows in 2024, surpassing the previous record of $500bn in 2022.

7. Equity markets were less affected than bond and currency markets. The weakness in yen led to a sharp rally in Japanese equities. The pro-Japanese equity market perspective of foreign investors still appears to be largely intact, largely driven by the premise of long-term corporate restructuring.

Chart 1: Global Economic Surprise Indices – Inflation and Growth

Index Source: Bloomberg

Source: Bloomberg

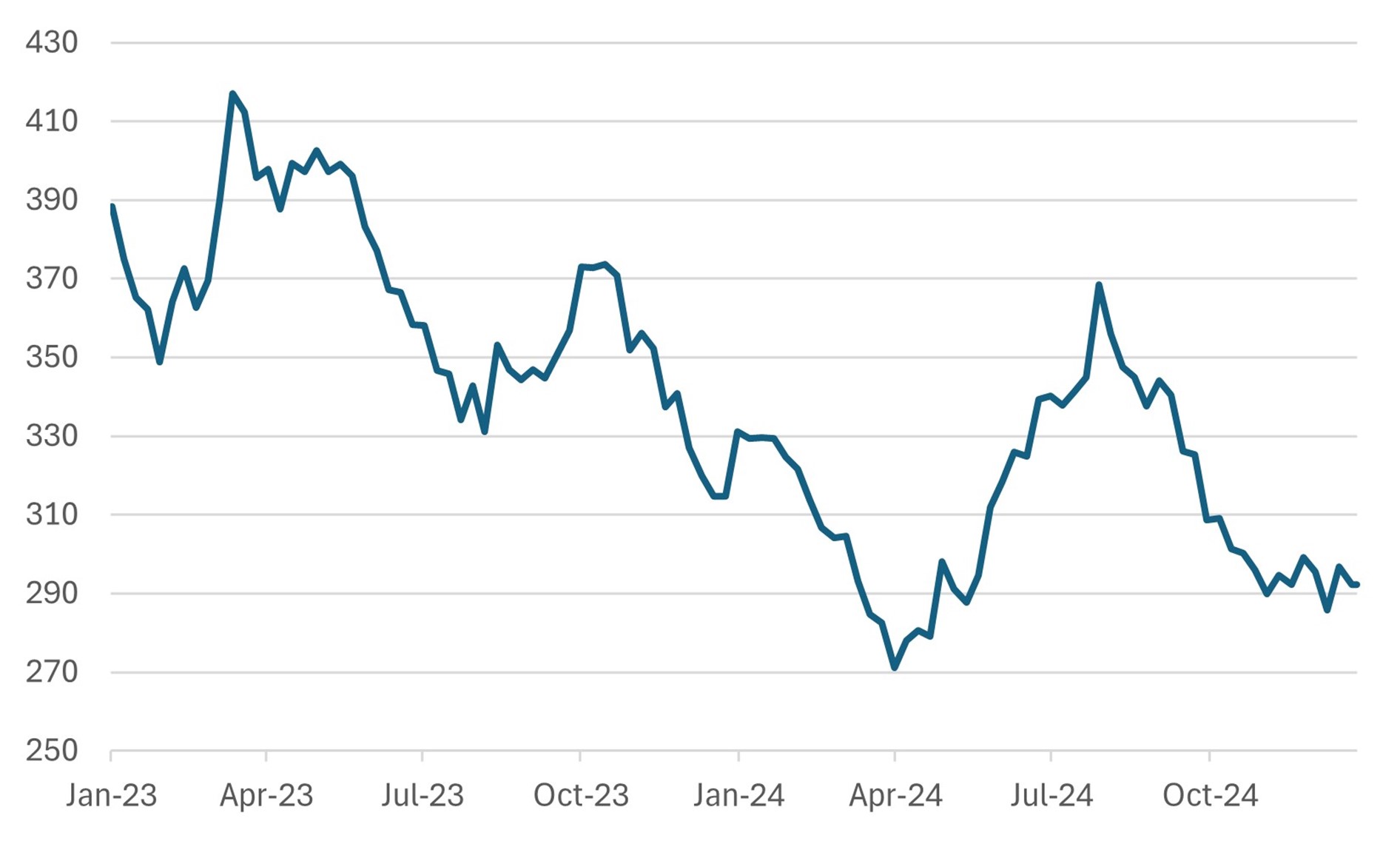

Chart 2: Emerging Market Bond Spread Source: Bloomberg

Source: Bloomberg

Gary Dugan - Investment Committee Member

Bill O'Neill - Non-Executive Director & Investor Committee Chairman

30th December 2024

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person's sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB