Click Here to Read the Full Version

The global economy appears increasingly uncertain about the path forward. Data, policy, corporate behaviour, and consumer confidence are all pulling in different directions – some reacting to higher inflation, some living in constant fear of it, and some closing their eyes and hoping it disappears. Last week’s dominant theme was a classic late-cycle dilemma: equities looked through the macro shock, supported by earnings, AI capex, and hopes of tangible progress in talks between the US and Iran, while bonds, currencies, commodities, and consumer surveys reflected rising inflation anxiety. The Gulf remains the tail risk. As the weekend evolved, talks shifted toward a possible agreement, with the US President cancelling plans to attend his son’s wedding to deal with Iran – a strong indicator of the administration’s pressing priorities.

Choked supply chains and resulting price inflation are becoming the new normal. We are seeing one of the most significant aluminium supply shocks in recent history, with missile damage to key smelters severely impairing Gulf production. LME stocks have reportedly fallen by a third, physical premiums in Japan and Europe have risen sharply, and the market is moving toward structural deficit after two decades of oversupply.

Inflation here is not just about higher spot oil. It runs as a sequence: freight delays, elevated insurance costs, replacement sourcing, higher physical premiums, inventory drawdowns, then margin pressure or pass-through. The same dynamic is visible in fuel. In the UK, retail sales dropped 1.3% in April, led by a more than 10% collapse in purchases of automotive fuel as households cut back after the price spike in March.

Chart 1: UK Retail Sales of Automotive Fuel Fall 10% in a Month

Source: Bloomberg

Meanwhile, the University of Michigan sentiment fell to a record low of 44.8, with gasoline prices cited as a major pressure point and inflation expectations rising. The current level is even lower than that at any stage during COVID.

Chart 2: University of Michigan Consumer Confidence at a Record Low

Source: Bloomberg

The eurozone delivered the week’s most worrying macro surprise. The S&P Global flash composite PMI fell to 47.5 in May, the fastest contraction in more than two years, with input price inflation at a three-and-a-half-year high and selling prices rising at the fastest pace in 38 months, consistent with inflation approaching 4%. Although the US version was stronger, much of that strength appears to reflect companies building inventories ahead of anticipated price rises rather than genuine demand.

The backdrop is poor: demand weakening, employment deteriorating, and inflation rising. EU finance ministers explicitly framed the region as stagflationary and warned against broad fiscal stimulus. In the UK, April borrowing came in £24.3 billion above expectations while retail sales fell sharply. The Bank of England and the Treasury face the same bind: the energy shock is hitting households, tax revenues, and debt-interest costs simultaneously.

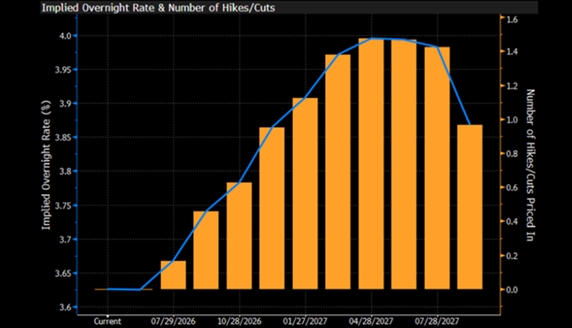

Kevin Warsh’s appointment as the Federal Reserve chairman, amid the backdrop of spiralling inflation and nosediving consumer sentiment, assumes greater significance. Warsh, on his part, promptly described any rate-cut discussion as “crazy” given the current 3.8% inflation and a stable labour market, calling for the removal of the easing bias without yet advocating an immediate hike. FOMC minutes from the April meeting showed more policymakers are open to tightening if inflation persists; markets are increasingly pricing the next move as up, not down.

Chart 3: Market Pricing of Fed…Tightening!

Source: Bloomberg

The ECB is in a different but equally difficult place. Growth is worse, the energy shock is nearer, and the price impulse is more visible. A Reuters poll showed economists expecting a June ECB hike and possibly another later in the year.

US equities rose for an eighth consecutive week, with the S&P 500 advancing 0.9% on the week, exhibiting notable resilience given 30-year Treasury yields touched 5.20%, their highest since 2007. Equities are pricing higher nominal growth; they are not, however, pricing higher discount rates. That tension will eventually resolve itself, and not gently.

Investor flows were less supportive. Global equity funds saw their first weekly outflow in nine weeks, losing $6.1 billion. US equity funds lost $12.1 billion while European funds gained $4.6 billion. Technology attracted $6.9 billion of inflows with investors de-risking their cyclical positioning but not abandoning AI. Global bond funds took in $21.9 billion, a substantial positive flow for a seventh consecutive week; gold and precious metals attracted $2.3 billion. The dollar index closed at a six-week high of 99.24, with the euro around $1.16 and sterling around $1.34.

The private-market story took a major step toward public-market price discovery. OpenAI is preparing to confidentially file for a US IPO, while SpaceX filed for what could become the largest IPO in history. Together, the two potential mega-listings would test the appetite for extreme-duration growth assets at a time when long yields are elevated. If OpenAI prices near its reported $852 billion valuation, it would reset marks across AI infrastructure, model companies, data-centre power demand, and listed AI proxies, and the scale of potential issuance is arriving just as global equity funds have turned to net redemptions.

Meanwhile, stress in the private credit space is becoming more visible. Fitch reported that the US private credit default rate rose to 7.0% in April, up from 5.8% a year earlier. The private-market story is therefore bifurcated: AI and space assets command scarcity valuations; levered cash-flow lending is losing the tailwind of expected rate cuts.

The Gulf remains the central market-moving risk. The World Bank is understood to have seen 27 countries move to secure access to crisis funds since the Iran war began, reflecting balance-of-payments stress now spreading through fuel importers and fertiliser-exposed economies.

In the US: April PCE inflation, personal income and spending, revised GDP, durable goods, consumer confidence, home sales, and bond auctions.

Outside the US: preliminary national inflation prints in Europe, ECB minutes, Japan inflation and industrial data, China industrial profits and PMI, and central-bank decisions in South Korea, New Zealand, South Africa, and Hungary.

The closure of the Strait of Hormuz, layered on top of the Red Sea still being effectively off-limits, has forced a fundamental revaluation of every node in global logistics. Around 20% of global oil and LNG previously moved through Hormuz; traffic is now at roughly 5% of pre-conflict levels. Both these important passages gone simultaneously imply the Cape of Good Hope is no longer an emergency detour; it’s the new normal, adding two weeks and hundreds of thousands of dollars per voyage. The strategic lesson every government is absorbing is the same one that Ukraine has already taught about energy pipelines: infrastructure one assumed was permanent can vanish, and supply chains built around efficiency rather than resilience are the ones that break somewhat easily. What’s now being quietly repriced is political exposure, how many hostile hands sit between your goods and your market.

The potential winners are countries that happen to be outside that exposure. Sri Lanka’s Colombo, non-aligned, Indian Ocean-centered, with Chinese, American, and Indian terminals operating side by side, is surging. The Middle Corridor through Central Asia, the Caspian, and Turkey is attracting billions of dollars in urgent investment, with Turkey’s vice president describing it as no longer an alternative but “a mandatory choice.” And Thailand’s long-envisioned land bridge across the Kra Isthmus, two deep-sea ports connected by rail to bypass Malacca entirely, has evolved from a perennial white elephant to a live infrastructure bid, simultaneously backed by Washington and eagerly awaited by Beijing. Long treated as a fixed background, geography is now becoming one of the most valuable strategic assets of the decade.

Gary Dugan – Investment Committee Member

Bill O’Neill – Non-Executive Director & Investor Committee Chairman

26th May 2026

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell a security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person’s sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth is Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB