Click Here to Read the Full Version

Events of the weekend are forcing a major resetting of the investment outlook and have caused major disruption to the Middle East. This correspondent is currently based in Mumbai after the closure of Dubai airspace. Below we look at the consequences of the Iranian crisis and reflect on how the year started.

Over the weekend, the markets that remain open have offered a useful real-time stress test of investor psychology. Gold moved higher in thin liquidity, reflecting a predictable bid for insurance rather than outright panic. The initial spike carried the hallmarks of portfolio hedging rather than systemic fear: volumes rose, but follow-through was measured. Such behaviour is consistent with previous geopolitical episodes where bullion absorbs the first wave of uncertainty before broader asset markets recalibrate. The move, at this stage, looks like a geopolitical risk premium being repriced rather than a disorderly flight from financial assets.

Chart 1: Gold price – moderate reaction

Source: Bloomberg

The US dollar also firmed modestly, particularly against higher-beta currencies, though the gains were far from dramatic. Safe-haven demand has been tempered by a countervailing consideration: any sustained escalation in the Middle East carries implications for energy prices and therefore inflation dynamics. Currency markets, in short, are alert but not alarmed. Funding markets remain orderly, and there is no sign of strain in cross-currency liquidity.

Regional equity markets in the Gulf, including the Tadawul, the Dubai Financial Market, and the Abu Dhabi Securities Exchange, have traded cautiously but without capitulation. Financials and transport names softened, while energy-linked stocks proved relatively resilient. There has been no broad-based liquidation and sovereign spreads have remained contained. That matters. Gulf balance sheets are materially stronger than in previous cycles, fiscal break evens are manageable, and liquidity buffers are substantial.

Taken together, the weekend price action suggests markets are adding a risk premium rather than pricing a systemic shock. Historically, sustained financial stress requires tangible disruption to oil flows, to infrastructure, or via direct major power involvement. None of those thresholds appear to have been crossed. Insurance is being bought, but there is no stampede for the exits.

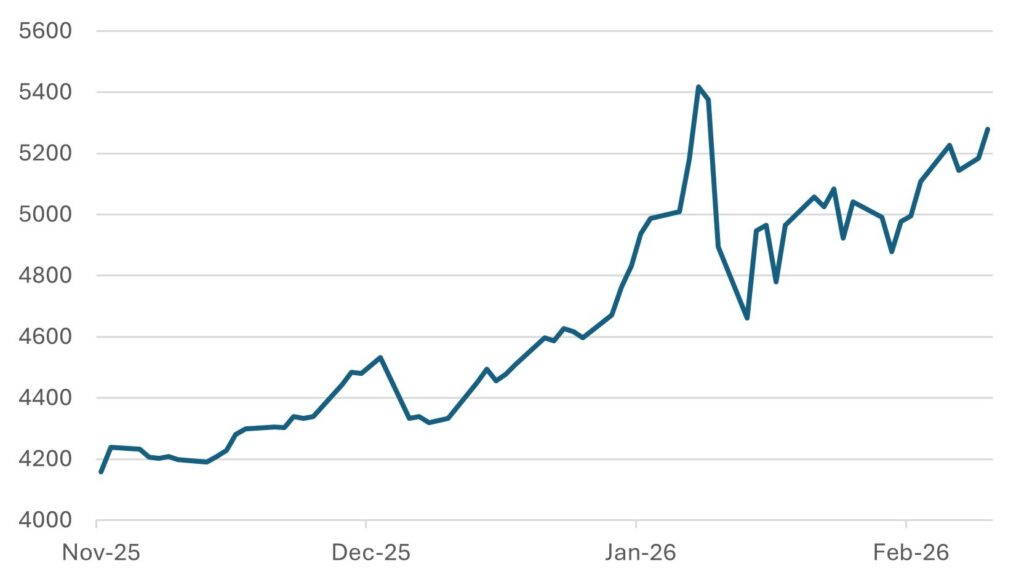

Over the weekend, the markets that trade continuously have provided an immediate gauge of risk sentiment. Gold rose sharply in thin conditions, briefly pushing above the recent $5,200 per ounce level and holding gains of roughly 1.5–2.0% from Friday’s close.

Volumes in futures markets were elevated relative to a normal weekend session, suggesting active hedging rather than passive drift. Worth recalling that during prior Middle East escalations, bullion has typically added 3–5% in the first fortnight before either consolidating or retracing once supply risks prove contained. So far, the move looks precautionary rather than disorderly. The US dollar has firmed modestly. The DXY index has edged higher by around 0.4–0.6%, with more pronounced strength against higher-beta emerging market currencies. EUR/USD slipped back towards the mid-1.07s, while USD/JPY held firm despite already elevated levels. Importantly, US 10-year Treasury yields have moved only marginally, fluctuating within a narrow 5–8 basis point range. That combination, a stronger dollar without a sharp rally in Treasuries, signals defensive positioning rather than a wholesale rush into duration.

In the Gulf, equity markets have traded cautiously but without signs of stress. The Tadawul eased by roughly 0.7–1.0% in early trade, led by banks and transport names, while energy-linked stocks were broadly flat to firmer. The Dubai Financial Market slipped around 0.5–0.8%, and the Abu Dhabi Securities Exchange was down a similar order of magnitude, again with resilience in oil and petrochemical counters. Regional CDS spreads have widened only marginally, by approximately 5–10 basis points, remaining well below the levels seen during the 2020 pandemic shock or the 2022 energy spike.

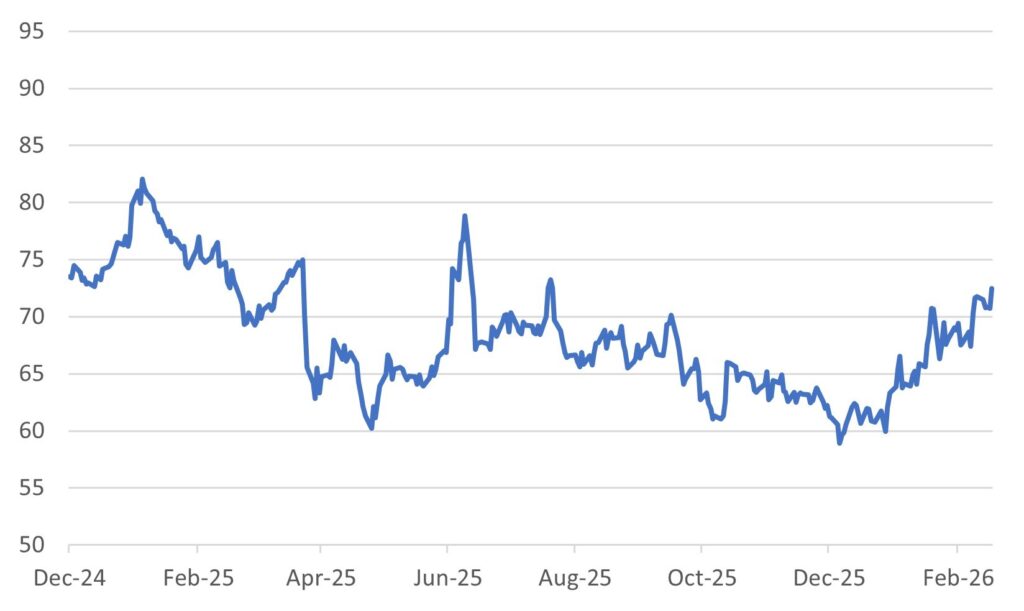

Brent crude, the variable that ultimately determines whether a geopolitical tremor becomes a macro event, has moved towards the low-to-mid $70s per barrel, up around 2–3% since Friday. That rise adds a modest inflationary impulse but remains far from the 10–15% weekly surges historically associated with supply disruption fears.

Chart 2: Brent Oil Price firm but no immediate spike ($bbl)

Source: Bloomberg

Taken together, the data point to an increase in geopolitical risk premium rather than systemic repricing. Gold is up low single digits, the dollar firmer by less than 1%, regional equities down around 1%, oil higher but contained. Markets are hedging, not panicking. History suggests sustained stress only emerges when physical supply is impaired or major powers become directly involved. Neither threshold appears, as yet, to have been breached.

The markets are clearly and at least initially not prepared to price a full and sustained closure of the Strait of Hormuz. Approximately 20–21 mb/d of crude oil and 25–30% of global LNG trade transits this chokepoint daily. A sustained closure could materially affect Brent prices, with potential knock-on effects for inflation dynamics, global growth expectations, and central bank policy considerations. Saudi Arabia and the UAE maintain partial bypass capability but cannot fully offset the disruption.

End-February: A year that has begun to rebalance

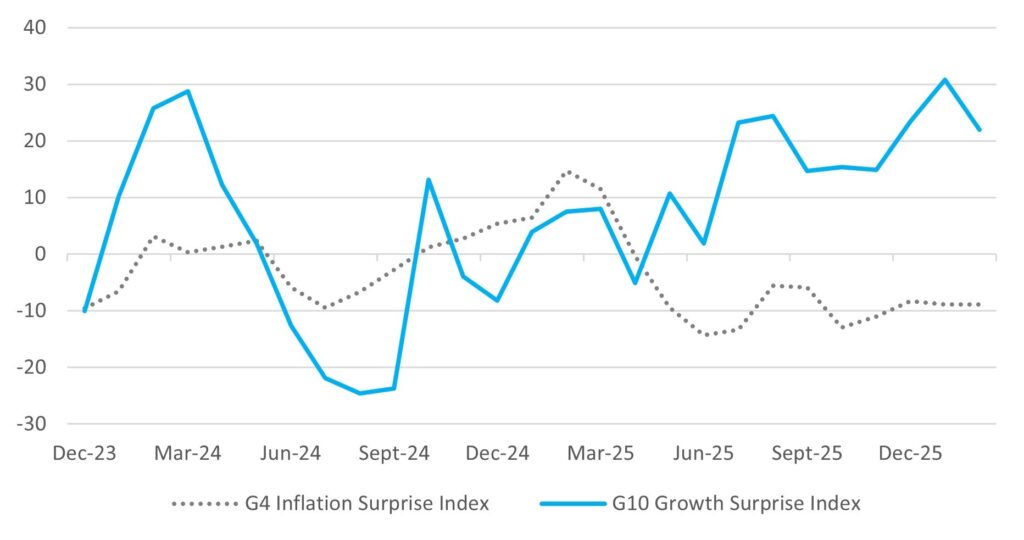

2026 so far has been characteristically different. The year has opened with an economy that is neither overheating nor collapsing. Growth remains respectable, inflation has cooled but not entirely vanished, and labour markets across major economies are softer at the margin without signalling a recession. What stands out in the current environment is not the level of activity but its dispersion. The United States continues to expand, yet fiscal largesse and political noise are eroding the characteristic exceptionalism that has long defined it. Europe is less fragile than feared even a year ago. Asia is quietly marching on. Clearly, the global economy is broadening out. Leadership is becoming less concentrated, and that matters on many fronts.

Chart 3: Economic Surprise Indices

Source: Bloomberg

Japan is perhaps the most symbolic change of all. For three decades, Japan embodied the old order’s stagnation narrative: Deflation, zero rates, and corporate torpor. It now finds itself at the forefront of renewal. Balance sheets are strong. Nominal growth has returned. Clearly, reforms in corporate governance are paying off. A political leadership armed with a super-majority has room to act, and one senses a generational shift in confidence. There is something faintly ironic about this. Japan once dominated the late 20th-century order. It then retreated into introspection. Now, as the old Western consensus frays, Tokyo appears willing to shape what comes next. Contrast that with an America led by a 79-year-old president fighting battles framed in the language of a bygone era. Markets, ever pragmatic, are asking which system looks forward and which looks back.

That question feeds directly into asset allocation. For much of the past decade, the US equity market has been the only game worth playing in town. Concentration in equities reached extraordinary levels in 2025, with a handful of technology giants accounting for the bulk of returns. Early 2026 reflects a discernible shift in that approach. Japan, Korea, and Taiwan are benefiting from the industrial build-out of semiconductors and AI infrastructure. India, riding high on structural growth and demographic momentum, continues to attract capital. China, while politically complex, is seeing selective re-engagement as valuations have become compelling. Europe has staged a quiet revival, supported by fiscal pragmatism and improved earnings breadth. Even Australasia has contributed, with commodity leverage and domestic resilience underpinning returns.

None of this implies it’s all over for the United States. Rather, it suggests that performance leadership may not remain as concentrated as in previous years. Recent performance patterns indicate a broader regional contribution to global equity returns compared to the prior period of US concentration. History reminds us that leadership rotates. The 1970s belonged to Japan and Germany, the 1990s to America, the 2000s to emerging markets. Regimes shift gradually, then suddenly. We may be in the early stages of another such turn.

The resurgence of small-capitalisation stocks reinforces the theme. After years of underperformance compared to mega-caps, smaller companies are finally finding support. Market activity suggests increasing interest in companies outside the largest capitalisation segment, particularly where earnings visibility is clearer. Small caps often outperform when domestic demand holds up and when confidence in the economic cycle improves. Their recent strength suggests that markets favour stability over contraction. It is a subtle but important signal. Breadth is improving. Risk appetite is diversifying.

Chart 4: Global Small Cap Versus Global Large Cap

Source: Bloomberg

Technology, meanwhile, is evolving rather than revolting. The narrative has shifted from multiple expansions to a focus on capital intensity. Yesterday’s growth darlings are now the industrial spenders. Artificial intelligence remains transformative, yet the market has shifted from dreaming of boundless margins to scrutinising the capital costs of AI infrastructure. Data centres, energy supply, semiconductors, and networks require enormous capital. Valuations for many leaders have become marooned, no longer racing ahead on (uncharacteristic) optimism alone. In many cases, they are raising capital to fund the next phase of expansion. The opportunity may increasingly lie not just in platform champions but in the ecosystem of suppliers enabling the build-out. It feels less like a speculative boom and more like a long industrial cycle taking shape. And indeed, market focus appears to be broadening from AI infrastructure providers to companies integrating AI into commercial applications.

Bond markets are perhaps the quietest yet most consequential arena, and maybe the most complacent. The US 10-year yield drifting towards 4% conveys calm. One could argue that the level conveys complacency. Fiscal deficits remain large, geopolitical risks are unresolved, and policy rhetoric is erratic. Yet, term premia appear contained. Bonds are behaving as though inflation is fully tamed and political volatility is irrelevant. Experience suggests caution. Periods of tranquillity in fixed income often precede adjustment. Recent bond market behaviour raises questions about the reliability of traditional correlations during periods of fiscal expansion and geopolitical uncertainty.

Chart 5: US 10-year and Global High-Yield Spreads

Geopolitics continues to buzz in the background. Trade tensions, security alignments, and election cycles are shaping capital flows. The dollar has softened at the margin, reflecting not crisis but doubt. A leadership preoccupied with mid-term politics may favour short-term gestures over coherent strategy. A Middle East stocked high with military hardware is not a good look. Currency markets tend to price such nuances before equity markets do. A world edging towards polycentricity naturally dilutes the dominance of a single reserve asset. That transition, if it gathers pace, would have far-reaching implications for capital allocation and risk management.

Commodities are the clearest expression of structural change. Energy prices have stabilised at levels that incentivise investment. Industrial metals continue to grind higher, supported by electrification, defence spending, and infrastructure renewal. Gold has marched to fresh highs, aptly reflecting both geopolitical unease and scepticism towards fiat orthodoxy. Commodities are increasingly being viewed as part of the broader macroeconomic adjustment process, reflecting supply chain restructuring and geopolitical realignment.

What, then, has defined the first two months of the year? Not exuberance, but rotation. Not collapse, but recalibration. Markets are broadening. Leadership is shifting eastward and outward. Smaller companies are reclaiming relevance. Technology is maturing into an industrial cycle. Bonds are serene, perhaps too serene. Commodities are firming as the real economy retools.

A final observation here: The generational undertone we are currently experiencing is unmistakable. Political systems, corporate governance, capital markets, and even investor psychology appear to be moving from an era defined by hyper-globalisation and financial engineering towards one focused on resilience, production, and sovereignty. Such transitions are rarely smooth and may result in changing patterns of market leadership over time.

The first two months of the year have exposed a simple truth. Concentration worked for a decade; but it may not work for the next. Markets are widening, leadership is rotating, and diversification is adding value again…. but then again there is Iran.

Gary Dugan – Investment Committee Member

Bill O’Neill – Non-Executive Director & Investor Committee Chairman

2nd March 2026

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person’s sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB