Click Here to Read the Full Version

The Middle East crisis can be viewed as a context in which portfolios are being tested, rather than one that necessarily leads to structural changes. Markets have already priced in the first phase of the shock, but uncertainty around duration and escalation remains high, which may limit conviction around large shifts in asset allocation.

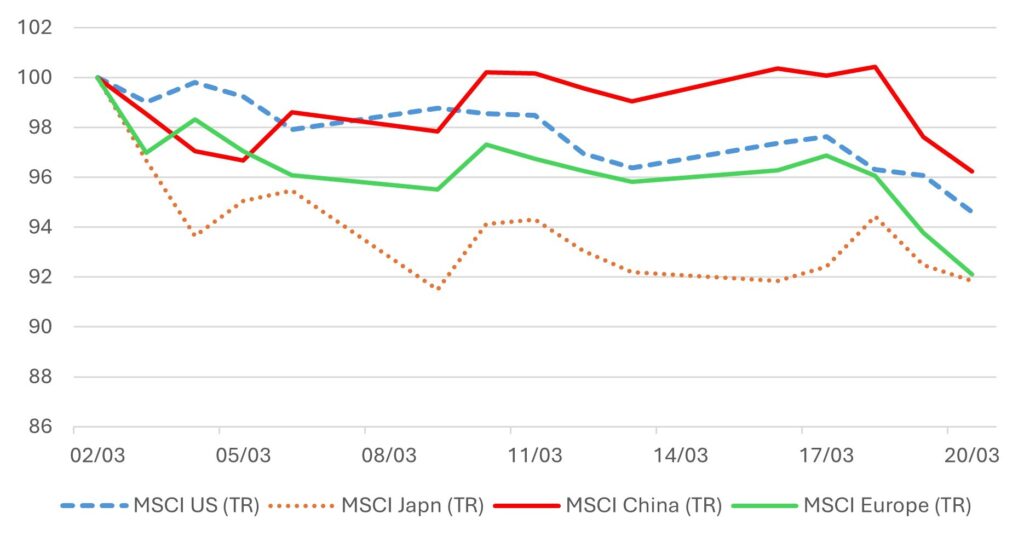

The market reaction to the current crisis remains consistent with an energy shock that is now feeding into inflation expectations and policy repricing, but it has not yet fully translated into a collapse in global growth. The initial data confirm a classic terms-of-trade adjustment. Since the start of the crisis, Brent crude is up 54.8% and natural gas 8.3%. Equity markets have responded asymmetrically. Global equities are down 6.9%, with sharper declines seen in regions structurally exposed to imported energy: Europe is down 10.4%, while Asia ex-Japan has declined 8.4%. By contrast, energy exporters have outperformed, with Saudi Arabia up 2.2% and Nigeria up 4.3%. Sectorally, energy is up 7.6%, while declines have been seen in industrial materials (15.9%), consumer staples (10.2%), healthcare (10.1%), and banks (8.9%). Technology (down 3.6%) has shown relative resilience so far, though it may be sensitive to higher rates and funding conditions.

Chart 1: Absolute Performance of Major Markets Since the Iran Crisis Started

Rebased to Jan 28th ’26=100

Source: Bloomberg

In fixed income, the dominant move has been a bear flattening. US 2-year yields are up 52.5 basis points (bps), while yields on the 5-year and 10-year are up 50.6 bps and 44.2 bps, respectively. This reflects a sharp repricing of the policy path rather than a clean recession signal. In FX, the dollar is stronger, up 2.0% on a trade-weighted basis, alongside the Swiss franc (up 2.4%), while sterling is down 1.0% and the yen has weakened by 2.0%, underlining Japan’s exposure to imported energy. Interestingly, precious metals have not behaved as safe havens. Gold is down 14.9% and silver 27.6%, reflecting real rate pressure and positioning rather than geopolitical hedging.

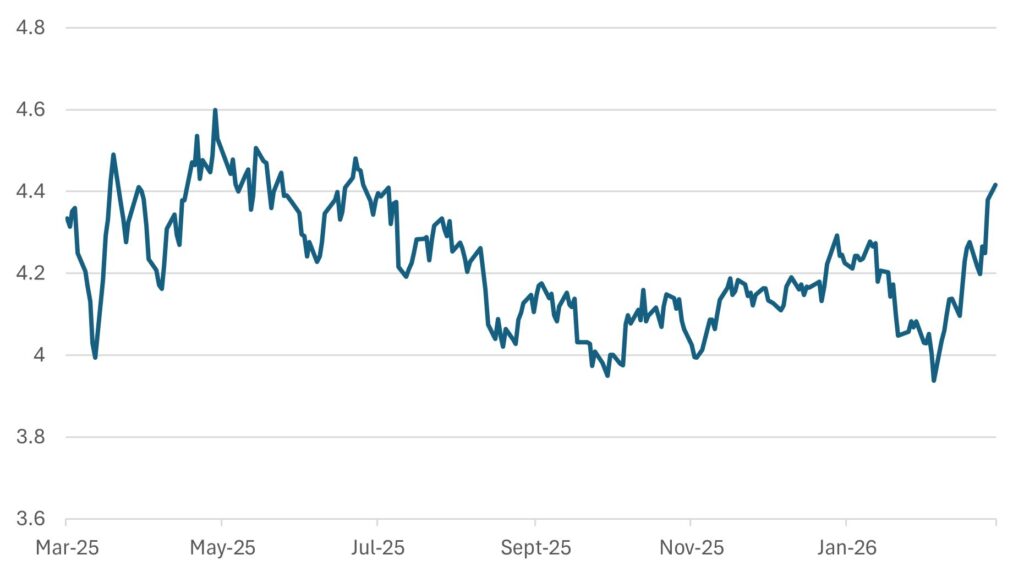

Chart 2: Core PCE inflation Moving Closer to Fed’s Target

Source: Bloomberg

The key macro takeaway from JP Morgan’s latest work is that the current shock is expected to raise inflation materially while only gradually eroding growth. A sustained period of oil near current levels would lift global inflation by approximately 0.8 percentage points (pp) and reduce global GDP by roughly 0.5 to 0.6 pp over time. However, the starting point for global activity is relatively strong, implying the near-term hit to growth should be modest, with the slowdown becoming more visible through the remainder of the year rather than immediately.

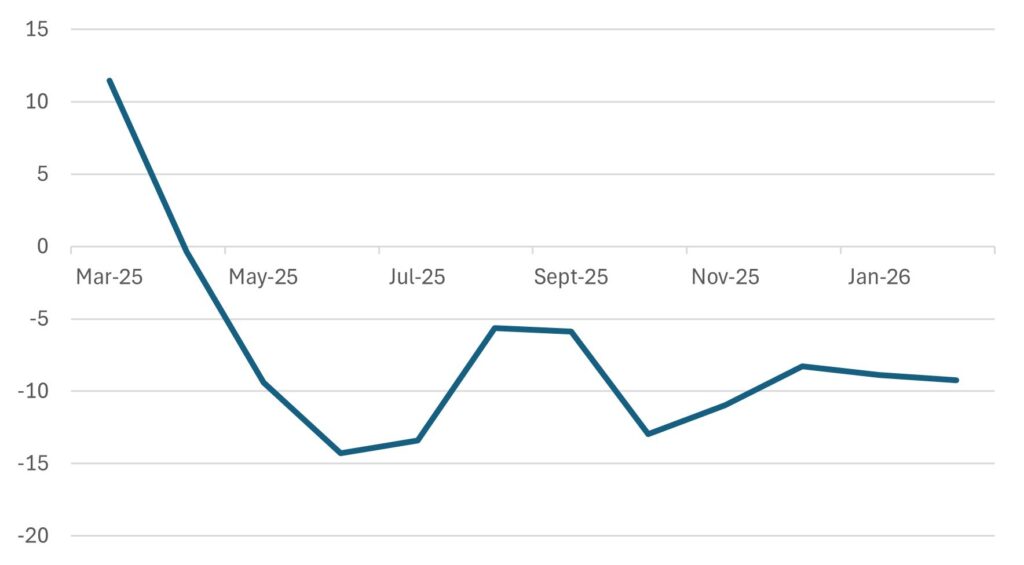

Chart 3: Waiting for Inflation Surprises after Recent Benign Data

(Citigroup inflation surprise index)

Source: Bloomberg

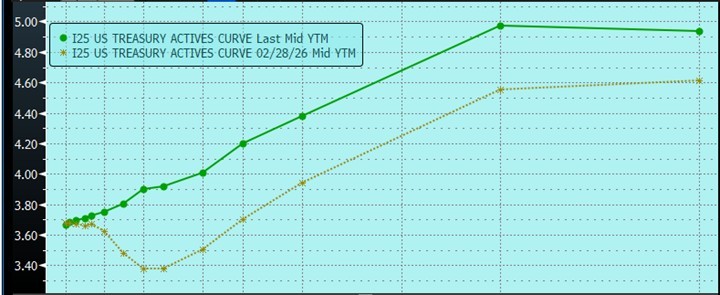

The flattening in yield curves is central to understanding the current macro signal. This is not a classic demand-driven slowdown where long-end yields fall sharply. Instead, the front end has repriced higher, as central banks signal that they cannot ignore an energy-driven inflation shock. The rise in the US 2-year yield relative to the 10-year reflects expectations that policy will remain restrictive, or potentially tighten further, even as growth risks rise.

Chart 4: US Yield Curve Flattens from the 02/28 Starting Point

Source: Bloomberg

This type of flattening is inherently unstable. If the shock remains contained, the curve may continue to flatten as inflation expectations dominate. However, if the shock persists and begins to erode activity more meaningfully, the market is likely to transition to a different regime in which front-end yields peak and decline while term premia rise due to fiscal concerns. This scenario could be associated with a shift from flattening toward steepening, depending on how conditions evolve.

The technical signals from fixed income markets reinforce this interpretation. The front end is pricing policy constraint, while intermediate maturities remain vulnerable to repricing. There is also increasing evidence that investors are beginning to differentiate across regions, with Europe and the UK appear more exposed to stagflationary pressures relative to the US based on current conditions.

Communication from various central banks over the past week has been uniformly cautious, with a clear shift away from any easing bias. Last week, the Federal Reserve held rates steady but emphasised that inflation remains elevated and uncertainty has increased. Evidently, central bankers are not prepared to look through the shock. Consequently, the policy reaction function has shifted toward maintaining restrictive conditions even as downside risks to growth increase.

The Bank of England delivered a similarly hawkish hold, explicitly noting that energy prices will push inflation higher in the near term, and highlighting the risk of second-round effects. Market pricing and some institutional forecasts currently reflect the possibility of additional tightening if inflation persists.

The European Central Bank has also adopted a more hawkish tone, with internal discussions increasingly focused on the possibility of renewed rate hikes if energy prices remain elevated. This marks a significant shift from earlier expectations of gradual easing.

In Japan, the situation is more complex. The Bank of Japan has maintained its current stance but signalled growing concerns about inflation risk, particularly given the country’s reliance on imported energy. This raises the possibility of further tightening even as growth weakens, a combination that reinforces downside risks to domestic demand.

The overall message from central banks is consistent. They do not see a growth shock that warrants immediate easing; they see an inflation shock with growth consequences. That distinction is critical for markets.

The impact on global growth is uneven and largely determined by energy exposure. Asia appears most vulnerable due to its reliance on imported energy flows through the Strait of Hormuz, the latest flashpoint in the war. Early signs of adjustments are already visible in the form of reduced industrial activity in energy-intensive sectors and policy measures aimed at managing demand.

Europe also faces significant downside risk due to its exposure to energy prices, particularly in gas markets. The UK is similarly vulnerable given the combination of its energy sensitivity and persistent inflation.

By contrast, the US is relatively insulated in the near term. Its status as a net energy producer, combined with a stronger dollar and more robust domestic demand, provides a buffer against the immediate effects of the shock. However, this insulation is not absolute. Higher fiscal deficits, increased borrowing needs, and rising interest costs introduce a secondary channel through which the shock could affect US growth over time.

Countries with high short-term refinancing needs are particularly exposed to the shock. Those with a greater reliance on short-duration debt or variable-rate structures will see the impact of higher rates transmitted more quickly into fiscal positions. This creates an additional layer of vulnerability, particularly in smaller or more externally dependent economies.

Equity markets are currently in the initial stage of adjustment. This phase is characterised by a clear shift away from energy importers toward energy producers. Markets with little or no significant energy sector or those heavily reliant on imported energy have experienced sharp underperformance. This reflects a straightforward repricing of earnings expectations and terms-of-trade effects.

However, the second stage of the adjustment, if that materialises, is likely to be more complex. If energy prices remain elevated and central banks maintain a restrictive stance, the pressure will shift toward valuation. High multiple growth equities may be more sensitive to changes in discount rates and margins under such conditions.

The relative resilience of technology and other growth sectors to date should not be interpreted as a sign of immunity. Rather, it reflects the sequencing of the adjustment. As the shock broadens from energy to financial conditions and demand, these sectors could experience increased pressure if financial conditions tighten further.

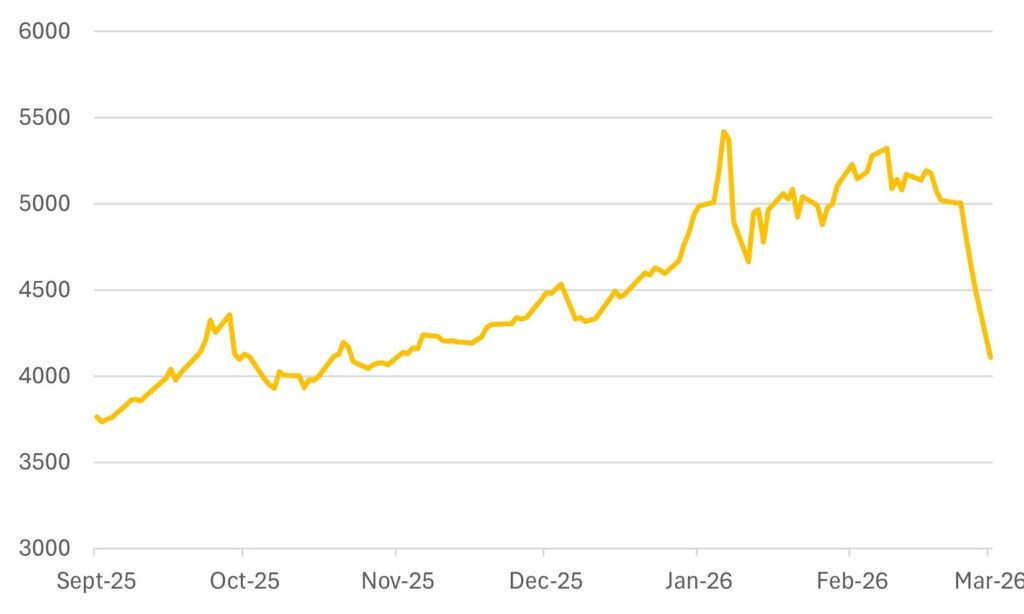

Gold’s decline during this period is notable. Rather than acting as a traditional safe haven, it has been driven lower by rising real yields, a stronger dollar, and positioning effects. This suggests that the market is prioritising monetary dynamics over geopolitical hedging in the short term.

Some analysts outline scenarios in which gold prices could face further downside in the near term. Some technical analysts such as Bill Sarrubi put the potential downside to $3,500, particularly if real rates continue to rise and dollar strength persists. However, some structural factors are cited as potentially supportive over the medium term. Structural factors, including fiscal expansion, geopolitical fragmentation, and ongoing demand for diversification, should continue to support gold over a longer horizon. For those wondering why the gold price has fallen, ETF selling and central banks going quiet on their buying are hitting precious metals. To us, it feels like the early days of the GFC, partly because of investors selling gold as a source of liquidity as they suffered margin calls.

Chart 5: Gold Price did not Initially Protect Investors Before Kicking in With a Vengeance Later

Source: Bloomberg

Despite the near-term uncertainty, the crisis highlights several long-term structural themes. The most prominent is the need to shift toward energy security. This includes increased investment in renewable energy, expansion of domestic energy production and infrastructure, and greater focus on regional supply chains.

Access to critical raw materials is becoming a strategic priority, with implications for investment in mining, processing, and recycling. The broader trend is toward resilience rather than efficiency, with capital increasingly directed toward reducing dependence on external suppliers.

There is also a geopolitical dimension. The perception about the US as an unreliable partner in certain contexts is prompting a reassessment of strategic alignment in multiple regions. This does not imply a wholesale shift, but it does suggest a more diversified approach to economic and security relationships.

Japan illustrates this dynamic. While aligned with the US, it is clearly seeking to limit its direct involvement in the conflict, reflecting both domestic constraints and strategic caution. This is consistent with a broader trend toward more autonomous policy frameworks.

Nevertheless, escalation risks remain central. Threats to energy infrastructure and shipping routes, particularly through the Strait, sustain a high-risk premium in energy markets. The possibility of further disruption ensures that volatility remains elevated and that the balance of risks to growth remains tilted to the downside.

The current environment is best understood as a stagflationary shock in its early stages. Growth remains resilient in the near term, supported by strong initial conditions, but is likely to slow as higher energy prices, tighter financial conditions, and more constrained policy settings feed through. Inflation is rising more quickly than growth is weakening, which is why central banks remain cautious and why markets have so far focused on the first-order effects in energy, rates, and regional equity dispersion.

For investors, the key point is that the shock is significant, but the path forward is still highly uncertain. Limited visibility on duration and escalation may make it difficult to form high-conviction views on major changes to strategic asset allocation. One possible approach discussed in this context is maintaining diversification, some perspectives emphasize the importance of not overinterpreting early market moves, Adjustments, where considered, are often framed in relation to specific exposures and evolving conditions where exposures are clearly inconsistent with a more inflationary and geopolitically fragmented environment. In other words, the current environment is sometimes characterised as favouring resilience and optionality over large-scale repositioning.

Gary Dugan – Investment Committee Member

Bill O’Neill – Non-Executive Director & Investor Committee Chairman

24th March 2026

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell a security or securities noted within nor should it be viewed as a communication intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. The information contained within should not be a person’s sole basis for making an investment decision. Please contact your financial professional at Falco Private Wealth before making an investment decision. Falco Private Wealth are Authorised and Regulated by the Financial Conduct Authority. Registered in England: 11073543 at Millhouse, 32-38 East Street, Rochford, Essex SS4 1DB